Crude Oil Edge: November 1, 2023

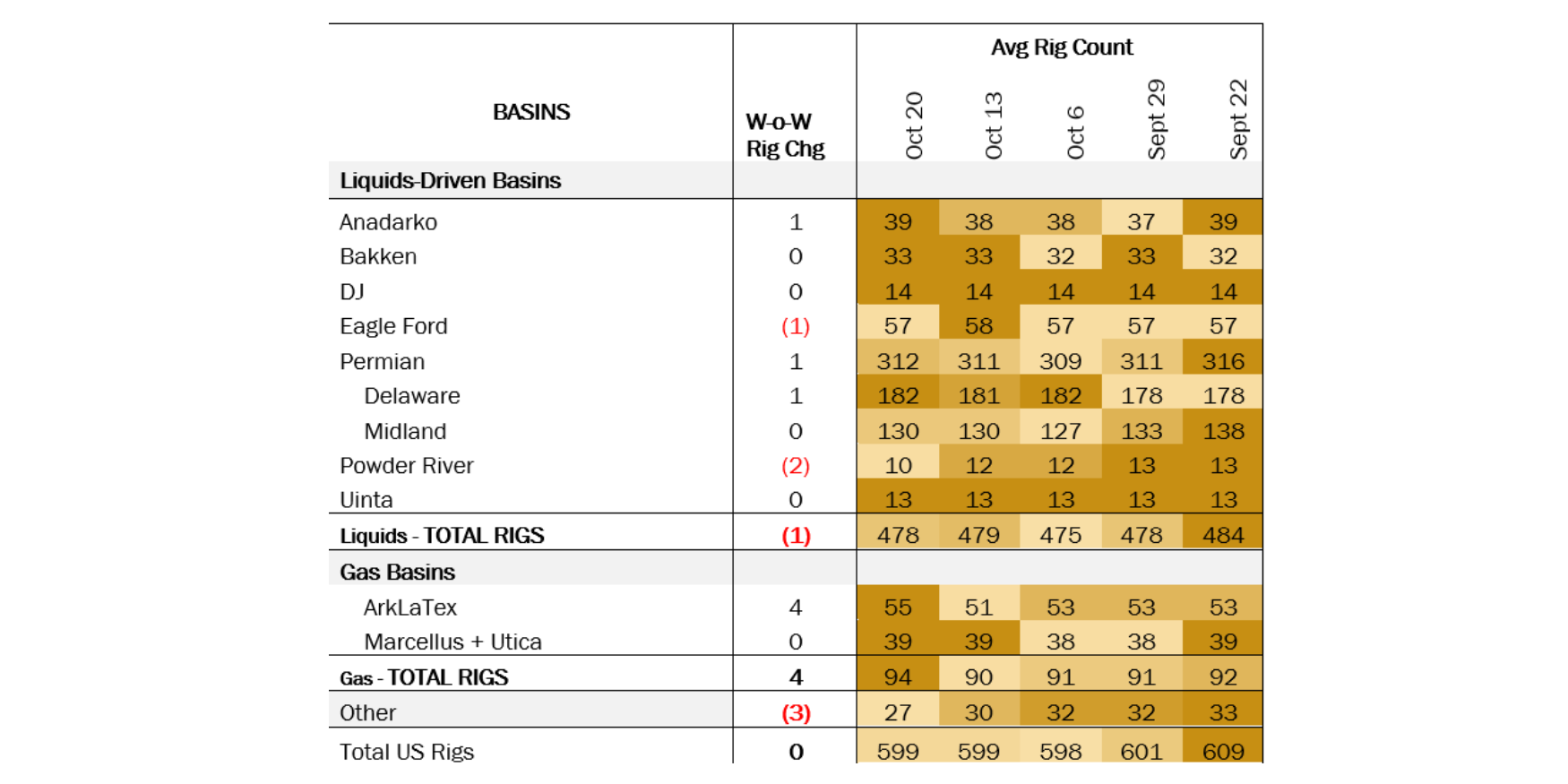

Rigs:

The US rig count is flat with total rigs remaining at 599. Liquids basins lost 1 rig. The Anadarko and Permian basins each gained 1 rig and the Powder River Basin lost 2 rigs. Within the Permian, the Delaware gained 1 rig and the Midland remained flat.

The US rig count has remained flat for the last three weeks at just under 600 rigs, while US crude oil production has held at an all-time high of 13.2 MMb/d, according to weekly EIA data. US crude oil production is already 80 Mb/d above EIA’s 2024 crude oil production forecast in the Short-Term Energy Outlook (STEO). The growth in production while rig counts have slowly decreased is due to productivity gains in drilling and completions, as well as efficiencies realized through M&A activity.

Infrastructure:

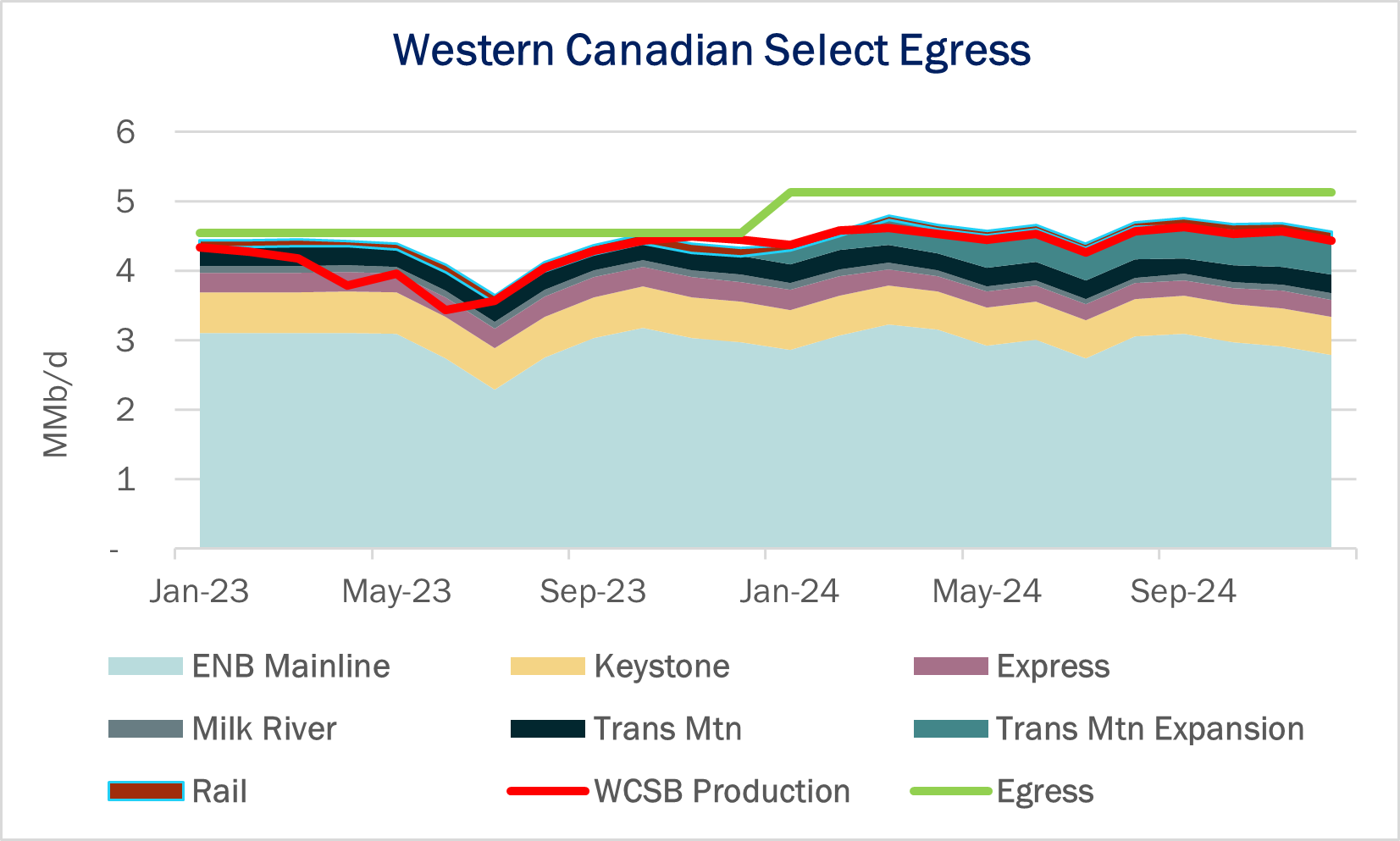

Is there one final hurdle before start-up of the Trans Mountain Pipeline expansion (TMX)? Trans Mountain notified the Canada Energy Regulator (CER) on October 19 it may need to use a contingency plan and adjust the pipeline diameter from 36 inches to 30 inches through the Fraser Valley, located ~125 miles east of Vancouver, BC due to hard rock encountered during horizontal and directional drilling (HDD).

In a project update, Trans Mountain said it has developed a contingency plan that could shorten the TMX completion time by 55-60 days. The plan arises from challenging conditions at the Mountain 3 horizontal crossing, where TMX has been drilling since June 2022. The project is on a ‘critical’ path due to HDD delays, Trans Mountain said in the CER filing.

Under the contingency plan, Trans Mountain would reduce the pipeline diameter to 30 inches from 36 inches in the section. The pipeline walls would be thicker at 15.9 mm, allowing TMX to continue operating at the approved maximum operating pressure, the pipeline said. Trans Mountain is currently boring a 42-inch hole it expects to complete in early November. It will then consider whether to ream out the permitted 48-inch section, or adopt the contingency plan.

CER responded last week, notifying Trans Mountain that a deviation from permits at the Mountain 3 horizontal crossing, including the permitted route and pipeline thickness, would require a variance and approval by the Canadian regulator.

All other indications point to TMX being mechanically completed by YE23 and placed in service by 1Q24. Trans Mountain last week began submitting numerous pipeline testing results to CER.

The original Trans Mountain Pipeline was built in 1953 and transports crude from Edmonton, AB to three delivery sites in British Columbia. In Vancouver, the pipeline supplies the Burnaby refinery and the Westridge Marine Terminal. Trans Mountain also connects to Sumas Pipeline and delivers volumes to refineries in Washington. TMX, a twin line, will add 590 Mb/d of capacity and deliver solely to the Westridge terminal to export Western Canadian Select production.

Storage:

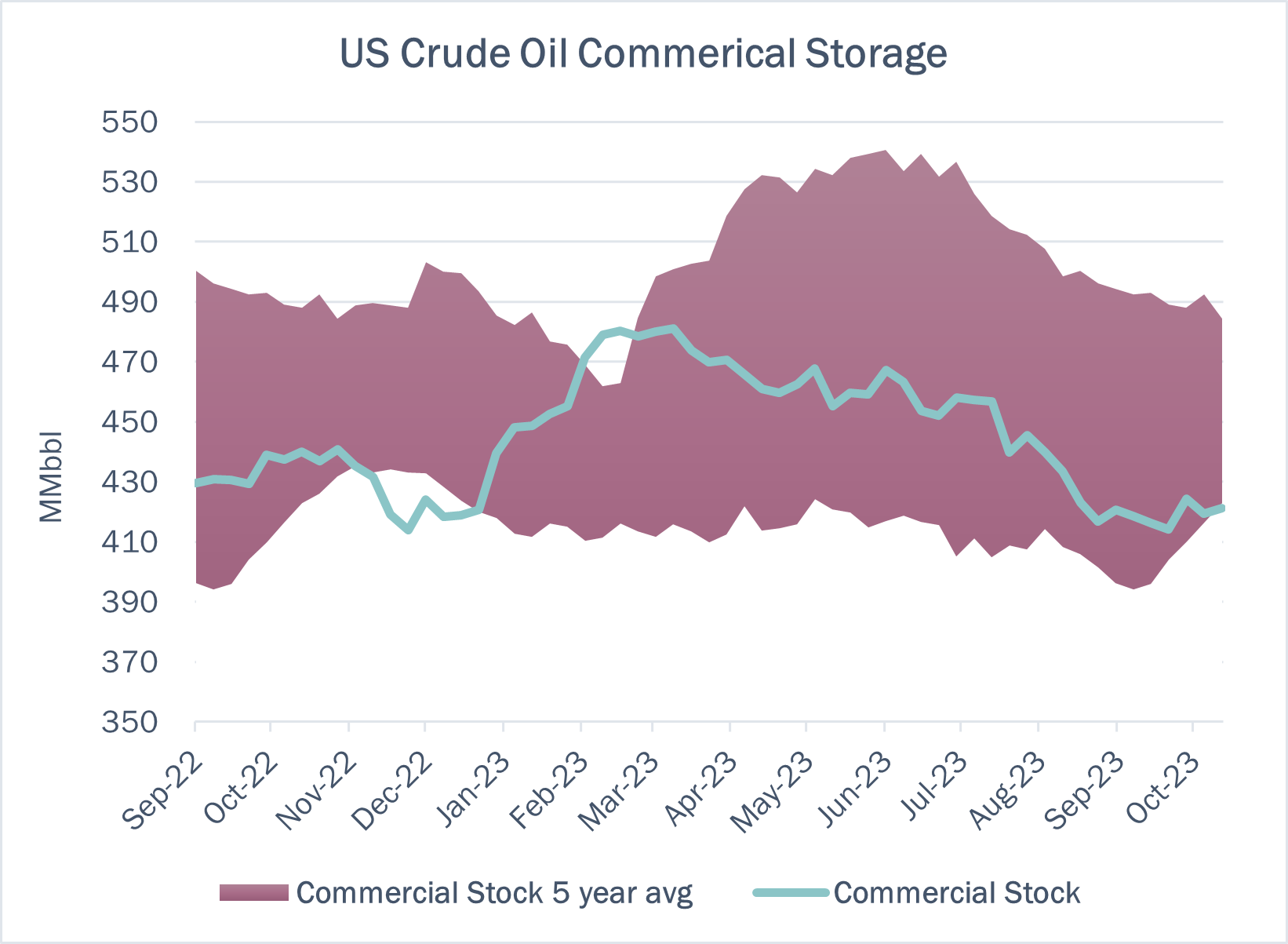

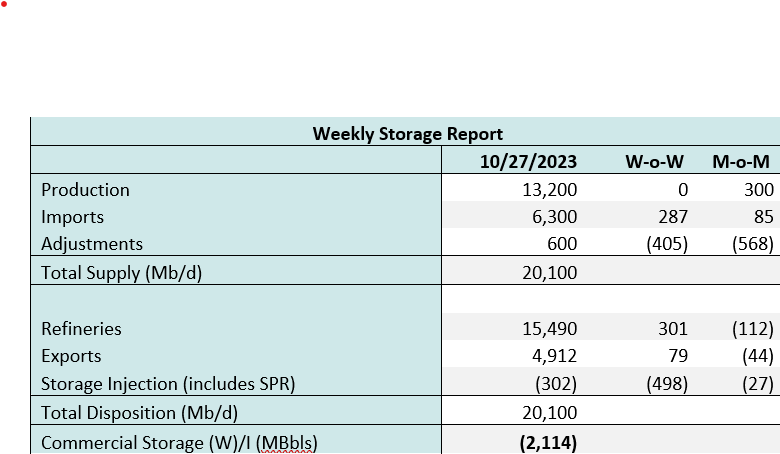

Crude oil commercial stocks saw an injection of 1.642 MMbbl for the week ending October 20 to 421.1 MMbbl. Strategic Petroleum Reserves (SPR) stocks are flat at 351.3 MMbbl. Total stock of commercial and SPR is 772.4 MMbbl.

East Daley expects a draw of 2.1 MMbbl in commercial inventories for the week ending October 27. We expect total US stocks, including the SPR, will close at 770.3 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, increased by 2% in liquids-focused basins. The Eagle Ford saw the largest change, gaining 29% W-o-W, but the pipeline sample coverage is poor in South Texas since most gas moves via intrastate pipelines, meaning the W-o-W increase is hard to trust. We expect US crude production to remain flat at 13.2 MMb/d.

According to US bill of lading data, US crude imports increased by ~287 Mb/d W-o-W to 6.3 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Argentina and Brazil.

As of October 30, there was ~1.7 MMb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by 1.6% W-o-W, coming in at ~15.49 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 27 vessels loaded for the October 27 week vs 30 vessels the prior week. EDA expects US exports to be 4.9 MMb/d.

Regulatory and Tariffs

Presented by ARBO

Tariffs:

TransCanada’s (TRP) Keystone and Marketlink pipelines both extended the terms of their temporary volume incentives through November 30, 2023. On Keystone, the temporary discount only applies to uncommitted shipments originating at the international boundary and delivering to Cushing, OK. Depending on the quality of the barrel, the rate ranges from $7.60/bbl to $8.12/bbl. To get the rest of the way to the US Gulf Coast, Seaway has a current rate of $1.15/bbl. Only volumes above 50 Mb/d qualify. (IS23- 698, filed September 25, 2023) (IS23-704, filed September 28, 2023)

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com/