The Daley Note: September 19, 2022

In an industry milestone, an independent producer has lined up an equity stake in a U.S. LNG export project. We see Devon Energy’s (DVN) agreement for the Delfin LNG project as a possible template for producers to bridge the capital gap and juice midstream investments in the high-flying LNG sector.

Under the Heads of Agreement (HOA), DVN will take up to 2 million tons per annum (mtpa) of liquefaction capacity in Delfin LNG, a floating LNG (FLNG) project planned in shallow Gulf of Mexico waters near the Texas-Louisiana border. DVN also will take

an equity stake in Delfin Midstream. The HOA creates a framework for DVN to reach a long-term tolling agreement for 1 mpta and the option for another 1 mpta of LNG supply. DVN also has opportunities for future equity investments in Delfin.

The DVN deal bolsters recent commercial momentum for the Delfin project. Delfin signed an HOA with Centrica in August and finalized a Sales and Purchase Agreement (SPA) with Dutch company Vitol in July. The Delfin project is fully permitted and targeting start-up in 2026.

Williams (WMB) and potentially Genesis Energy (GEL) would most benefit from the project’s success. Delfin has a long-term lease for a segment of GEL’s High Island

Offshore System (HIOS) that connects to the Delfin Offshore Pipeline, where Delfin would dock its FLNG vessels. Gas would move from an interconnect with WMB’s Transco pipeline in Cameron Parish, LA to the FLNG vessels to make and store LNG.

To our knowledge, the DVN – Delfin deal is the first investment by an independent in a Lower 48 LNG project. Producers Apache (APA) and EOG Resources (EOG) have signed supply deals with Cheniere Energy’s (LNG) Corpus Christi terminal providing netback exposure to Asian LNG prices, but these contracts don’t include an equity component.

Since the dawn of the shale boom, producers have flirted with the idea of selling gas overseas. But where the will was strong, weak wallets have kept E&Ps at arm’s length. LNG is expensive, requiring billions in capital for projects, and E&Ps have been debt-strapped for over a decade. Instead, international marketers and utilities have been the primary customers for U.S. LNG projects.

Will the next LNG wave be different? Two factors could create a new “supply-push” model. Producers are repairing balance sheets and showing discipline for the first time. Many now have plenty of free cash on hand with higher oil and gas prices. At the same time, LNG projects have downscaled toward smaller modular designs requiring less upfront capital. Delfin claims it only requires 2.0-2.5 mpta of commitments to take a final decision on its first Delfin floating vessel.

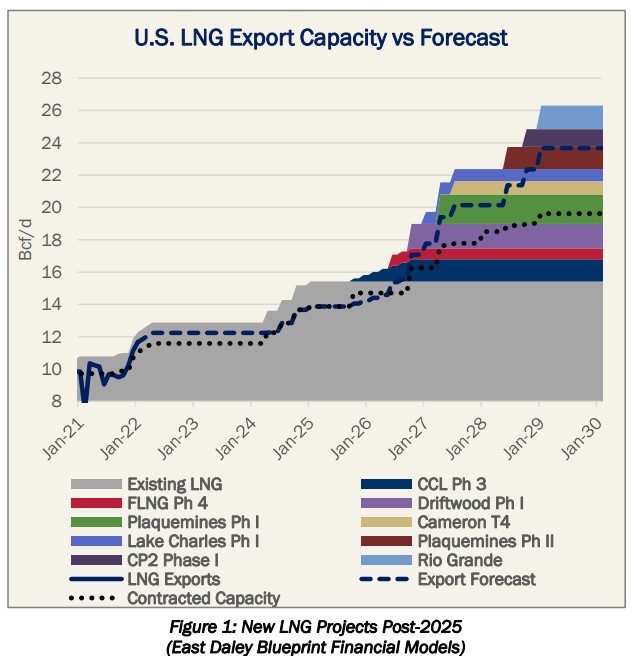

The Devon HOA is modest (up to ~260 MMcf/d of demand), but we see outsized midstream impacts if it leads to similar arrangements boosting LNG project commercialization. Top Northeast gas producer EQT (EQT) also is trying to tie up with an LNG project in Louisiana. East Daley is tracking the second wave of LNG projects that we forecast to add over 12 Bcf/d of LNG demand post-2025. If producers can move further downstream into LNG sales, our outlook will prove conservative. – Andrew Ware Tickers: APA, DVN, EOG, EQT, GEL, LNG, WMB.

Upcoming Event

HART Energy – America’s Natural Gas Conference 9 a.m. – Tuesday, Sept. 27 in Houston, TX

Click here to set up a meeting with Zack on Weds., Sept. 28 in Houston the day following EDA’s presentation.

The Daley Note

Subscribe to The Daley Note (TDN), “midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.

North American Energy Indicators and Equity Prices

Key Private Debt Metrics

North American Natural Gas Prices

North American Crude Oil Prices

North American Natural Gas Liquids Prices

Subscribe to The Daley Note (TDN), “midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.