Natural Gas Weekly: June 23, 2023

Flows: Houston Ship Channel (HSC) prices have strengthened considerably this year on a tighter regional balance, boosted by higher demand. As markets and infrastructure expand, East Daley’s Macro Supply and Demand Forecast points to more volatility ahead for the Gulf Coast industrial hub.

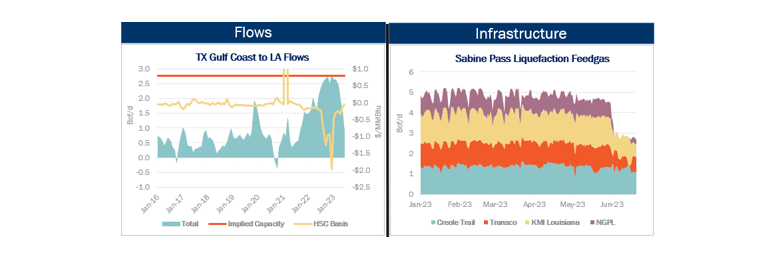

HSC basis recently traded $0.05/MMBtu behind the Henry Hub, up from a steep ~$2 discount seen in December 2022. The price dislocation occurred as flows surged on pipelines from the Texas Gulf Coast into Louisiana. The loss of demand from Freeport LNG, coupled with rising Haynesville production in East Texas, created a looser regional balance. The return of Freeport LNG in 1Q23 has helped restore balance, while an early summer heat wave is keeping more gas in Texas to generate power, significantly reducing flows from Houston-area pipes into Louisiana.

However, the brief dislocation in December may be an omen for more volatility to come. Developers are building ~3.5 Bcf/d of Permian pipeline projects to come online through 2024. All that incremental gas will be moved to the Texas Gulf Coast, dramatically increasing supply in the region. East Daley anticipates this will lead to another event where South Texas pipelines run completely full to Louisiana, forcing HSC to trade at a material discount to Henry Hub once again.

The forward strip is not pricing in this risk, calling for HSC to average a ~$0.20/MMBtu discount to Henry Hub through 2024. However, as we saw in December when eastbound capacity was pushed, the discount can grow much wider. The first pipe expansion for 375 MMcf/d is expected to come online in September, and EDA will be keeping a close eye on Gulf Coast spreads.

Infrastructure: Cheniere Energy (LNG) is conducting scheduled maintenance on two of the six trains at Sabine Pass Liquefaction, lowering industrial demand on the Gulf Coast.

The Sabine Pass feedgas sample has declined by 1.7 Bcf/d M-o-M, from 4.6 Bcf/d in May to just 2.9 Bcf/d through the first two weeks of June. Most of the drop is attributable to reduced flows on the Natural Gas Pipeline Company of America (NGPL) and Transcontinental Gas Pipe Line (Transco) systems. Cheniere has not indicated how long the maintenance work is expected to last at the terminal in Cameron Parish, LA. Sabine Pass, the largest US LNG export facility, can receive over 5 Bcf/d of gas at peak operations.

NGPL has used this opportunity to conduct in-line inspections on the pipeline segment between Montgomery, TX and Cameron, LA, temporarily reducing capacity eastbound through Compressor Station 302 in Montgomery, TX.

Rigs: Permian Basin rig counts have been falling in recent weeks. In East Daley’s latest Midstream Activity Tracker, the Permian rig count sits at 342 rigs for the June 16 week, down 19 rigs over six weeks. The basin hit a rig peak this year of 361 at the end of April. While large public company rig count has remained constant, smaller independent operators have been dropping rigs, contributing to the falling basin-wide count.

Storage: EIA reported a 95 Bcf storage injection for the June 16 week, beating market expectations for a 91 Bcf injection. Working gas inventory currently totals 2,729 Bcf, 362 Bcf above the 5-year average. In our updated Macro Supply and Demand Forecast, we estimate working gas ends June at 2,939 Bcf.

Natural Gas Weekly

East Daley Analytics’ Natural Gas Weekly provides a weekly update to our monthly Macro Supply and Demand Forecast. The update covers rigs, flows, production, prices and capacity constraints that materially change our view on supply and demand. This update highlights what investors and traders need to monitor in natural gas to ensure they are on the right side of the market. Subscribe to the Natural Gas Weekly.