Any day now, a giant gas pipeline led by WhiteWater Midstream is due to start from the Permian Basin. Following Matterhorn Express, the market has line of sight on a second WhiteWater project, Blackcomb Pipeline. The new pipes will help resolve takeaway issues from the Permian but are likely to create a different set of problems moving natural gas downstream, according to East Daley Analytics’ latest regional models covering the Permian and Texas Gulf Coast.

On July 31, WhiteWater announced Blackcomb and a final investment decision (FID) between the Whistler Pipeline JV (WhiteWater, MPLX and Enbridge (ENB)) and Targa Resources (TRGP). East Daley includes Blackcomb in our updated supply and demand forecasts for the Permian Basin and Houston Ship Channel, released last week. We model linefill on Blackcomb starting in July 2026 and ramping to a full 2.5 Bcf/d by December ’26 to the Agua Dulce hub.

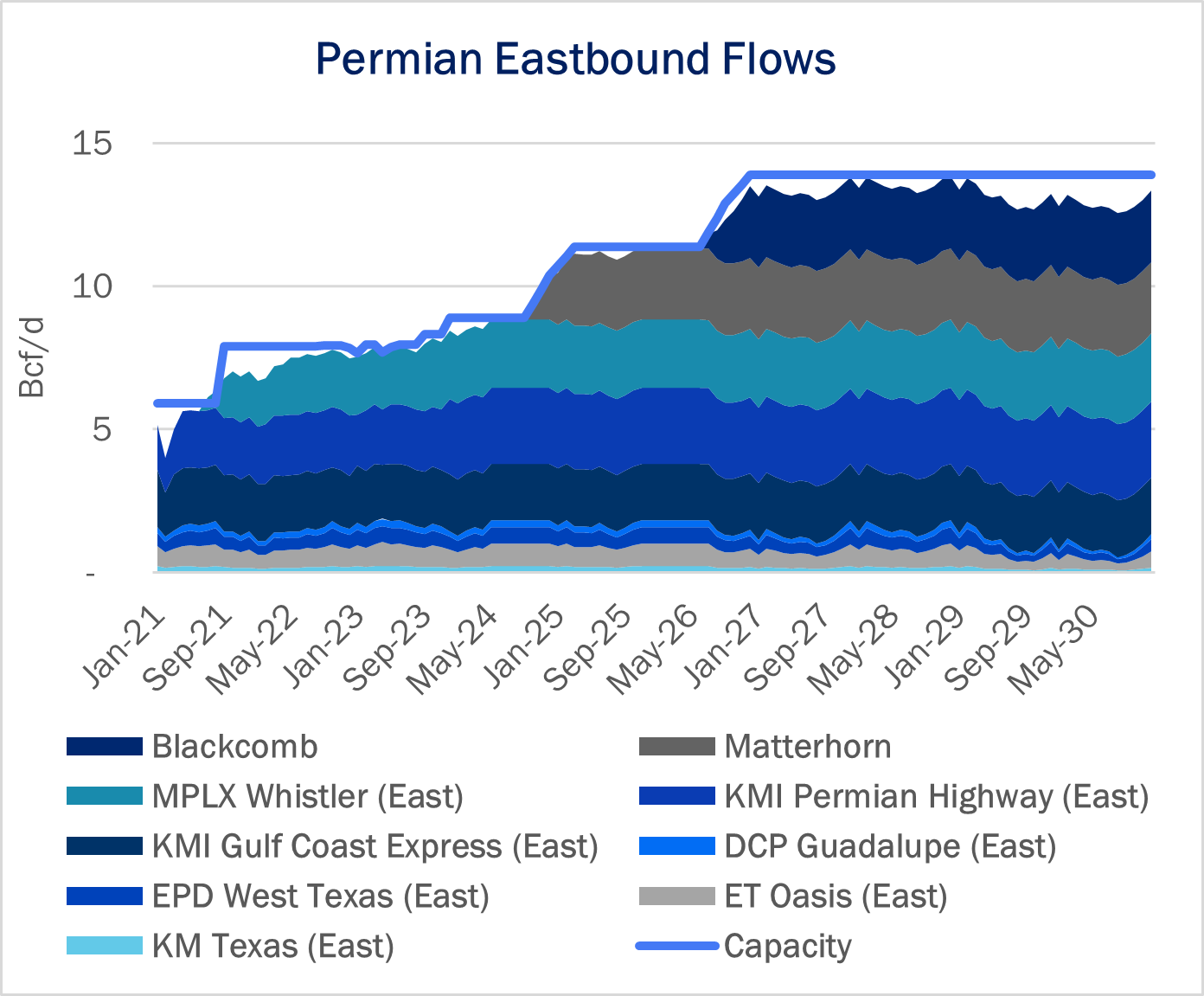

The Permian Basin is a reliable source of supply for South Texas, a role bolstered by recent compression expansions (Permian Highway Pipeline, Whistler) and the new 42-inch Matterhorn and Blackcomb projects. In the Permian Basin Supply & Demand Forecast, EDA expects pipeline utilization on these eastbound routes to remain high as Permian supply continues to grow (see figure).

Rapid Permian growth has saturated the South Texas market in recent years, leading to wide basis differentials between Houston Ship Channel and the Carthage market in East Texas. Pipeline capacity from the Permian to South Texas increases to 11.4 Bcf/d in 2025 after start-up of Matterhorn Pipeline, and to 14 Bcf/d in 2027 once Blackcomb comes online, up from just 3.4 Bcf/d in early 2019.

We expect limited demand growth in 2024, so additional inbound flows from the Permian will need to displace inbound supply from the Carthage market in East Texas. In the Houston Ship Channel Supply & Demand Forecast, we reduce flows from Carthage to Houston by 1-2 Bcf/d from 2024-28 to balance the South Texas market, indicating Houston will trade at a discount to Henry Hub. Carthage will provide swing supply in 2029-30 as LNG demand in South Texas comes online and additional pipeline capacity from Texas to Louisiana is available to support LNG projects on the TX/LA border.

Check out our new Permian Basin and Houston Ship Channel regional models for more information. – Oren Pilant Tickers: ENB, TRGP.

NEW Webinar – Fast and Furious: Production, Constraints and Opportunity

East Daley will host our latest MCAP webinar on September 25th at 10 am MT. In “Fast and Furious: Production, Constraints and Opportunity,” we will look at opportunities across the energy complex:

- Crude: Double H Conversion’s impact on crude fundamentals, and who can capture that upside.

- Gas: What the Blackcomb pipeline means for TRGP’s G&P growth in the Permian.

- NGLs: The fight for barrels in the Permian, and the implications of OKE’s acquisition of ENLC.

Register here to join us.

Sign Up for the NGL Insider

East Daley NGL Insider provides weekly updates on the US NGLs market including supply and demand fundamentals, basin-level views, and analysis of market constraints and infrastructure proposals. We explore sub-basin dynamics and provide market insights on NGL flows, infrastructure, and purity products. Sign up now for the NGL Insider.

The Daley Note

Subscribe to The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices and EDA research likely to affect markets in the short term.