Natural Gas Weekly: February 17, 2023

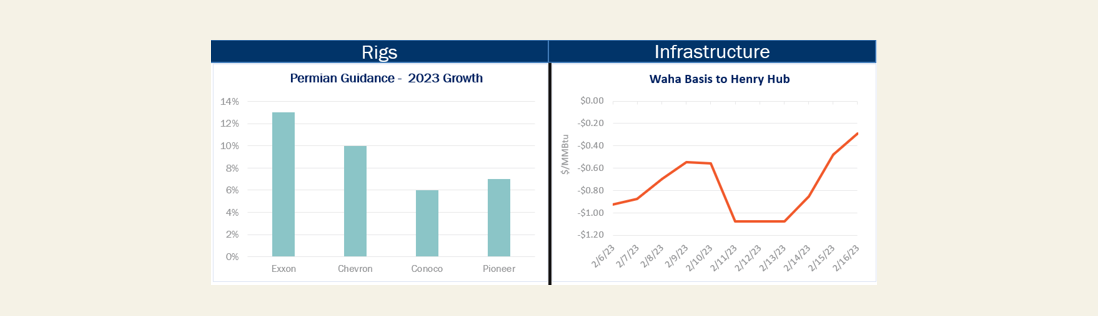

Rigs – Several of the largest producers in the Permian Basin expect to increase production in 2023, albeit at a slower pace than the double-digit growth seen in 2022. Many also are guiding to flat to slightly increasing rig counts in the basin.

Leading the pack so far from quarterly updates are the majors ExxonMobil (XOM) and Chevron (CVX). In the company’s earnings call, XOM executives guided to a 13% increase in Permian natural gas and liquids production this year. In its 4Q22 update, CVX predicted its Permian output would grow 10% in 2023. Management at ConocoPhillips (COP) guided to mid-single-digit growth this year. Pioneer Natural Resources (PXD) estimated its Permian liquids would grow 5% in 2023, with natural gas to grow at a slightly faster rate.

Several management teams highlighted a need to add more drilled but uncompleted wells (DUCs) after drawing down DUC inventory in 2022, a factor that could temper growth. Overall, upstream guidance so far indicates Permian growth of around 10% in 2023, consistent with our outlook. In the latest Permian Basin Supply and Demand Forecast, East Daley forecasts Permian residue gas production to grow 1.5 Bcf/d in 2023 (exit to exit). We expect Permian oil production to grow 525 Mb/d this year.

Infrastructure – Shippers wasted no time filling the newly repaired Line 2000 of the El Paso Natural Gas (EPNG) system. The gas pipeline connecting the Permian Basin to consumers in the Southwest resumed operations on Wednesday (Feb. 15), ending an 18-month outage. The pipe was running nearly full at daily nominations of 606 MMcf on Wednesday and Thursday (Feb. 16), or 99% utilization.

Line 2000 had been offline since an explosion near Coolidge, AZ in August 2021. The outage has contributed to downward pressure on Permian gas prices (as basin production fills takeaway capacity) while pushing West Coast prices higher this winter. Waha basis tightened during the first two days of resumed flows this week, trading $0.29/MMBtu behind the Henry Hub on Thursday (Feb. 16) vs a discount of $0.80 earlier in the week, according to Bloomberg price data.

The return of Line 2000 should also help tame price volatility in Southern California and rebuild depleted storage stocks. Working gas inventories are 38% below the five-year average in the Pacific region, according to the latest storage data from the Energy Information Administration (EIA). In contrast to other Lower 48 markets, the West Coast has seen below-normal temperatures this winter. We anticipate demand to refill storage will keep Line 2000 and other pipelines to the West Coast running at higher utilizations this spring.

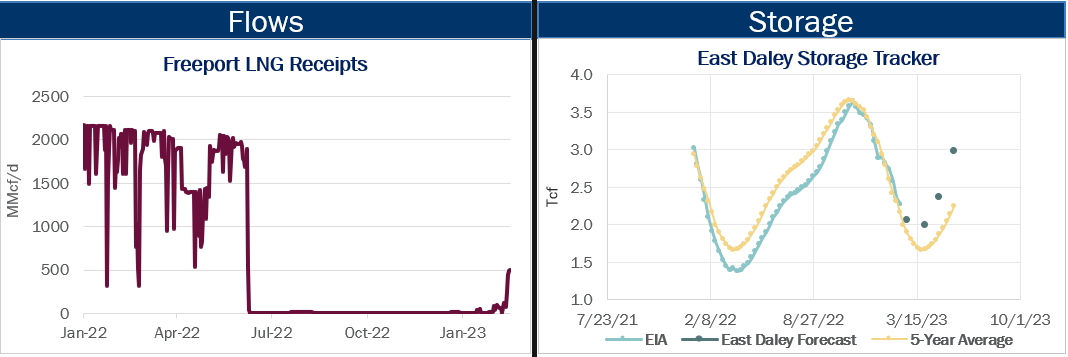

Flows – Freeport LNG continues to make progress restoring operations. On Feb. 12, Freeport LNG shipped its first cargo since an explosion in June 2022. The cargo consisted of LNG already stored in tanks at the Texas terminal. Freeport also has been ramping its gas pipeline receipts since Feb. 12. Volumes rose to ~0.5 Bcf/d this week, or about 25% of the maximum throughput to the LNG facility.

Freeport has been receiving small gas volumes since late January after regulators approved its request for a limited restart. The approvals allow Freeport to begin preliminary operations, including commissioning work and cooldown of the LNG piping system and Train 3. East Daley has been monitoring an uptick in feedgas to the Freeport plant. Deliveries began on Jan. 26 and reached a high of 507 MMcf/d on Feb. 15. East Daley models Freeport ramping to the full 2.1 Bcf/d of export capacity by the end of April. ![]()

Storage – EIA reported a 100 Bcf storage withdrawal for the Feb. 3 week, putting working gas inventories at 2,266 Bcf. In our Macro model, we estimate storage inventories end February at 2,058 Bcf. Storage is 183 Bcf above the 5-year average after the latest EIA report.

Methodology Note: As of Jan. 30, 2023, East Daley Analytics is switching to WellDatabase for wellhead production data and rig information. East Daley uses a data aggregator, BlackBird BI, to collect and organize raw data published by WellDatabase. As part of the change in data providers, East Daley’s active rig estimates will now reconcile with the weekly Baker Hughes rig publication. The biggest change in rig counts is a reduction in vertical rigs in areas like the Anadarko, ArkLaTex and Barnett, which is not expected to impact the production outlook. Please direct any methodology questions to Ryan Smith ([email protected]). Additionally, we are happy to introduce you to our new data vendors if there is any interest.

Natural Gas Weekly

East Daley Analytics’ Natural Gas Weekly provides a weekly update to our monthly Macro Supply and Demand Forecast. The update covers rigs, flows, production, prices and capacity constraints that materially change our view on supply and demand. This update highlights what investors and traders need to monitor in natural gas to ensure they are on the right side of the market. Subscribe to the Natural Gas Weekly.