Natural Gas Weekly: August 31, 2023

Flows – Western US natural gas prices are trading at a significant premium to the broader market as hot temperatures and seasonally low regional storage push prices higher. The market dynamic is supportive of new infrastructure to open westbound gas flows.

Spot gas at the Southern California border traded for $4.38/MMBtu on Tuesday (August 29) amid above-normal temperatures vs a Henry Hub price of $2.59/MMBtu, a $1.79 premium. The Opal hub in Wyoming traded for $3.47, $0.88 higher than the Henry Hub, while the Malin, OR point was $0.82 above the market benchmark. Hot weather across the Southwest pushed up demand for power generation. Daytime temperatures in Los Angeles peaked over 100 degrees Fahrenheit on Monday and remain in the mid-90s this week. The El Paso pipeline also reported underperformance at some pooling points in the Permian Basin, supporting higher prices.

Western prices eased on Wednesday (August 30) but remain much higher than other regions. The SoCal border traded for $3.78 on Wednesday (+$1.28 vs HH) and Opal traded for $3.10 (+$0.60 vs HH).

Western prices eased on Wednesday (August 30) but remain much higher than other regions. The SoCal border traded for $3.78 on Wednesday (+$1.28 vs HH) and Opal traded for $3.10 (+$0.60 vs HH).

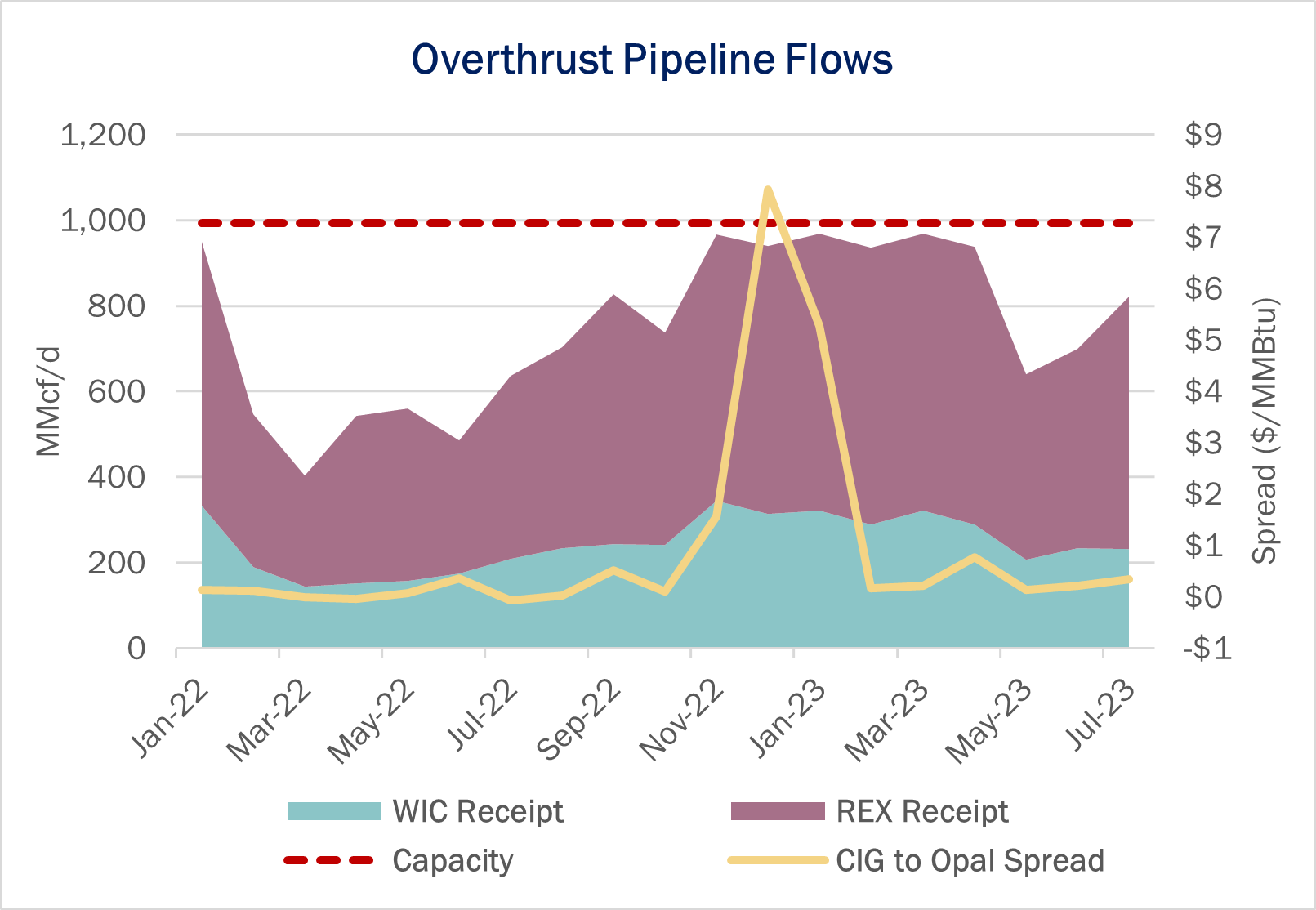

East Daley has highlighted the regional divide in natural gas markets resulting from the wild 2022-23 winter. While most of the Lower 48 experienced a mild season, the West Coast and Rockies saw below-normal temperatures that drained regional storage fields and sent prices spiking to over $40/MMBtu. The spread between the Colorado Interstate Gas (CIG) mainline and Opal blew out during the winter as westbound deliveries maxed out on the Rockies Express Pipeline (see figure). Higher demand to refill storage in the West continues to support higher prices in 2023. Entering September, underground storage in the Pacific region remains 7.3% below the 5-year average, according to weekly EIA .

The regional premium supports a project planned by Williams (WMB) to move more gas to western markets. In its 2Q23 earnings, WMB announced a binding precedent agreement to expand the MountainWest Overthrust Pipeline (MWOP). The project would add compression at several stations in Wyoming, increasing westbound capacity by 325 MMcf/d between Wamsutter and Opal.

The MWOP expansion would relieve some of the constraints between Opal and CIG to move gas from the Rockies to the West Coast. Western US markets rely on ~4.5 Bcf/d of gas sourced from the Rockies, and the path between the CIG mainline and Opal offers the shortest distance to new sources of supply. WMB anticipates a project in-service date of December 2026.

Infrastructure – Hurricane Idalia made landfall late Tuesday (August 29) on the Gulf Coast of Florida as a Category 3 hurricane. The storm is expected to take a course through Georgia and the Carolinas as a weakened tropical storm. We expect lower gas demand for power generation as thousands of utility customers lose power, with little to no impact on production.

East Daley expects storage to exit October at 3,908 Bcf, or about 339 Bcf higher than inventories at the end of last year’s injection season, according to our latest US Macro Supply and Demand Forecast. With inventories at such a high level, we on balance see downside risk to gas prices if an active hurricane season forces demand offline from power plants and industrials along the Gulf Coast, particularly at LNG export facilities.

Storage – Traders expect EIA to report a 31 Bcf storage injection for the August 31 week, according to a survey by The Desk. EIA reported an 18 Bcf storage injection for the August 24 week, leaving working gas inventories at 3,083 Bcf, or 268 Bcf above the 5-year average.

Storage – Traders expect EIA to report a 31 Bcf storage injection for the August 31 week, according to a survey by The Desk. EIA reported an 18 Bcf storage injection for the August 24 week, leaving working gas inventories at 3,083 Bcf, or 268 Bcf above the 5-year average.

Looking ahead, we expect high storage to keep pressure on prices in the autumn shoulder months. In East Daley’s August US Macro Supply and Demand Forecast, we predict inventories build to 3,908 Bcf by the end of October, a level that could send cash prices lower as spare storage capacity becomes scarce. We forecast Henry Hub prices to average $3.15/MMBtu through March 2024.

Rigs – East Daley is reviewing the latest week of rig data for integrity issues. We are posting the previous week’s data. US rigs decreased by 11 W-o-W to bring the total count to 623 for the August 18 week. The Anadarko, ArkLaTex and Marcellus+Utica are each down 3 rigs, the Bakken is down 2 rigs, and the Powder River Basin is down 1 rig.

Rigs – East Daley is reviewing the latest week of rig data for integrity issues. We are posting the previous week’s data. US rigs decreased by 11 W-o-W to bring the total count to 623 for the August 18 week. The Anadarko, ArkLaTex and Marcellus+Utica are each down 3 rigs, the Bakken is down 2 rigs, and the Powder River Basin is down 1 rig. Natural Gas Weekly

East Daley Analytics’ Natural Gas Weekly provides a weekly update to our monthly Macro Supply and Demand Forecast. The update covers rigs, flows, production, prices and capacity constraints that materially change our view on supply and demand. This update highlights what investors and traders need to monitor in natural gas to ensure they are on the right side of the market. Subscribe to the Natural Gas Weekly.