Executive Summary: Rigs: The total rig count decreased by 4 for the November 3 week, down to 563 from 567. Flows: The Permian sample is up to 6.1 Bcf/d. Infrastructure: Appalachian Basin energy players are planning for wet gas growth.

Rigs:

The total rig count decreased by 4 for the November 3 week, down to 563 from 567. Liquids-driven basins declined by 5 rigs W-o-W.

- Permian (-2):

- Delaware (-1): EOG Resources

- Midland (--1): Exxon

- Anadarko (-1): American Warrior

- Bakken (-1): Chord Energy

- Eagle Ford (+1): EXCO Resources

- Powder River (-1): Anschutz Corporation

- Uinta (-1): WEM Operating, LLC

Flows:

- The Permian sample is up to 6.1 Bcf/d. On November 14. Permian Highway Pipeline (PHP) brought 711 MMcf/d of capacity back online. There was a reduction of 489 MMcf/d (out of the total 2.65 Bcf/d) until November 20, but that limitation should be in the past. Matterhorn volumes continue to level up at around 1.4 Bcf/d.

- The ArkLaTex sample continues to decline, settling at 10.0 Bcf/d. The weekly trend lines up with our latest ArkLaTex production forecast, where we expect a slower production ramp.

- The Gulf of Mexico seems to have fully recovered from the impacts of shut-ins ahead of Tropical Storm Rafael. The regional sample increased 3% W-o-W to 7.32 Bcf/d.

Infrastructure:

Appalachian Basin energy players are planning for wet gas growth. Range Resources (RRC) is on pace to grow production just shy of 2% from 2023 to ’24. Much of that growth is focused on the liquids-rich window in the southwest Marcellus. Range said on its 3Q24 earnings call that it expects “to see our production stream continue to have a little bit more of an NGL contribution.”

Actions mimic words, as RRC has 2 active rigs drilling behind MPLX’s 2.4 Bcf/d Majorsville-Houston-Harmon Creek G&P systems. RRC is the biggest contributor to the MPLX complex and is the driving force feeding a 300 MMcf/d expansion at the Harmon Creek processing plant. The project has an expected in-service date in 2H26 (refer to the Energy Data Studio visual below).

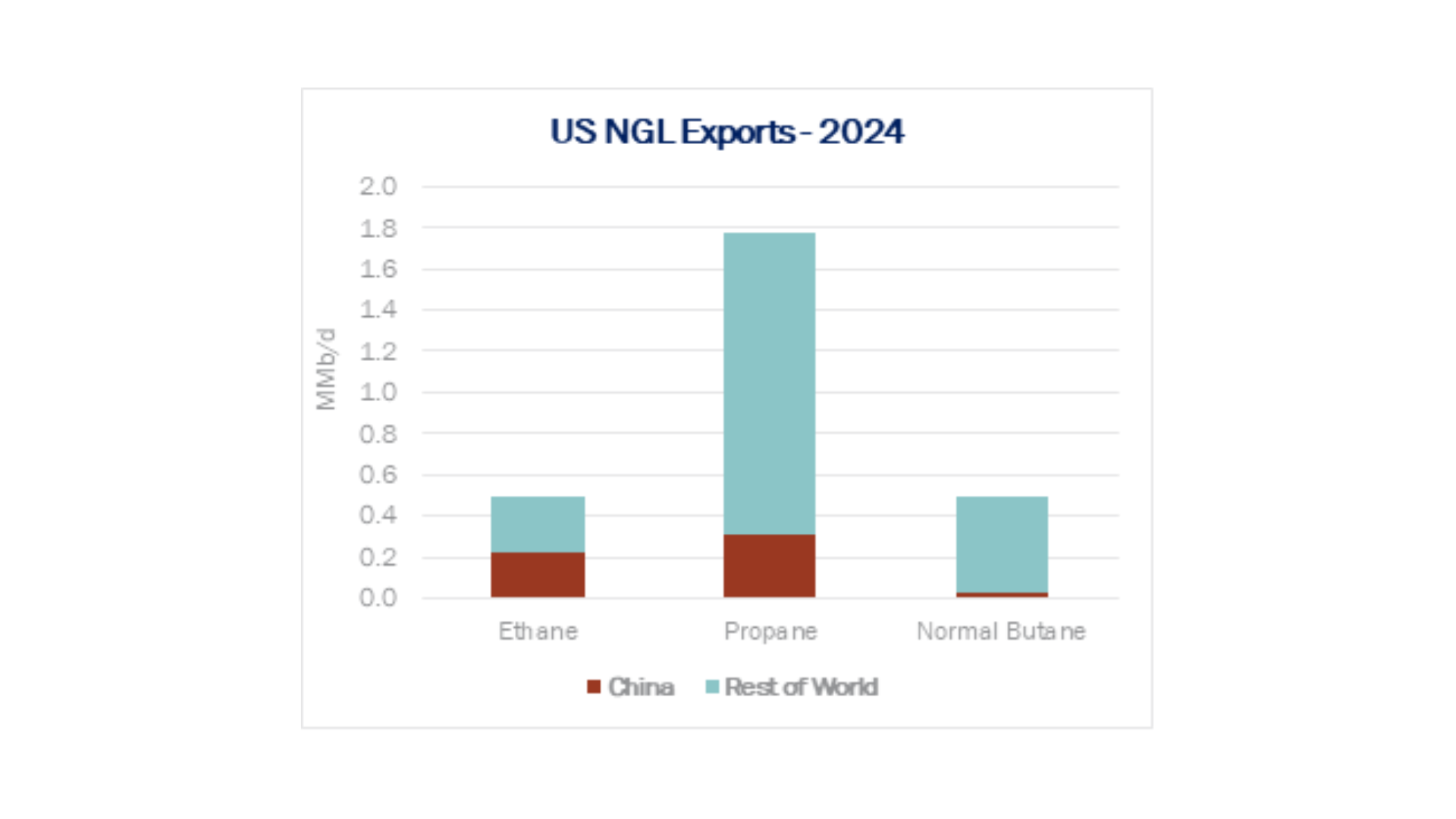

Connecting the dots further downstream, the Harmon Creek facility is also expanding de-ethanization capacity by 40 Mb/d, which will also be operational in 2H26. The de-ethanizer facility will alleviate any potential growth constraints caused by out-of-spec natural gas. RRC ships ethane on Mariner West (to NOVA Chem in Windsor, Canada) and on ATEX Pipeline (to Mont Belvieu export markets), but management recently noted 80% of NGL production is exported at the Marcus Hook terminal near Philadelphia. Management often touts the Northeast pricing premium over Mont Belvieu and uses Energy Transfer’s (ET) Mariner East and Marcus Hook infrastructure to access European demand.

will also be operational in 2H26. The de-ethanizer facility will alleviate any potential growth constraints caused by out-of-spec natural gas. RRC ships ethane on Mariner West (to NOVA Chem in Windsor, Canada) and on ATEX Pipeline (to Mont Belvieu export markets), but management recently noted 80% of NGL production is exported at the Marcus Hook terminal near Philadelphia. Management often touts the Northeast pricing premium over Mont Belvieu and uses Energy Transfer’s (ET) Mariner East and Marcus Hook infrastructure to access European demand.

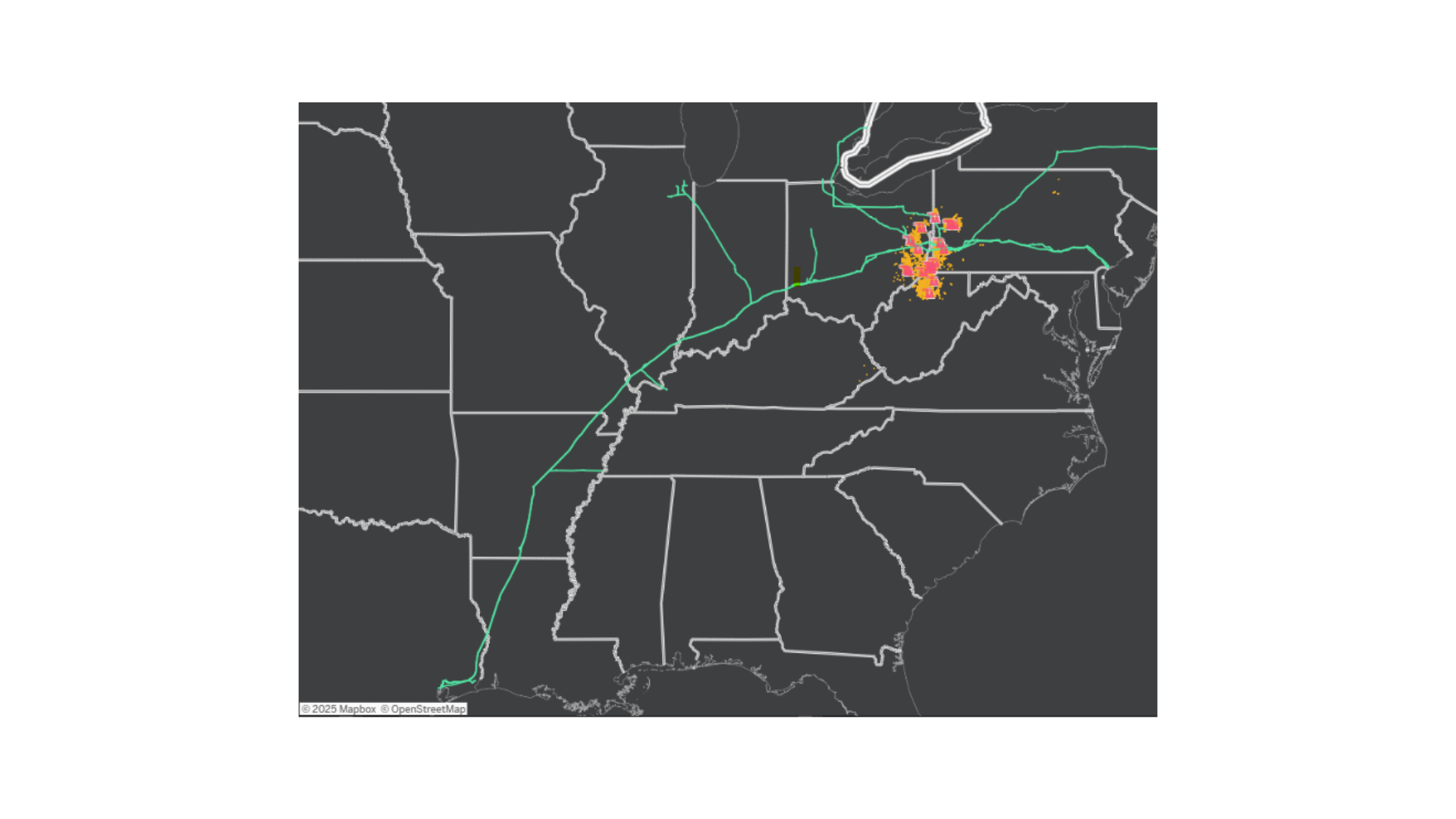

ET has gone back and forth on the Marcus Hook expansion, which would be achieved with additional refrigeration and storage capacity. Two data points suggest momentum in the last leg of the trip to the vessel bound for Europe. The first is a FERC filing by ET disclosing its intent to strip NGLs from the Rover interstate gas pipeline via its Revolution plant at the “Rover-Bulgar Interconnect”. These Revolution-produced NGLs would very likely be shipped on Mariner East to Marcus Hook (see map below). An environmental assessment filed in July ‘24 noted a construction timeline of three months beginning in 4Q24, and ET’s latest investor deck this month confirmed construction is underway.

The second data point is MPLX’s investment in de-ethanization behind Harmon Creek. Much of RRC’s ethane is already shipped to Europe and the expanded facility would likely send more ethane across the pond. These two data points just might be enough to get a Marcus Hook expansion to a final investment decision soon.

Data Points & Product Release Calendar: