Executive Summary: Rigs: The total rig count decreased by 9 for the October 13 week, down to 560 from 569. Liquids-driven basins declined by 9 rigs W-o-W. Flows: The Bakken gas sample continues to rebound, increasing by 3% W-o-W (+76 MMcf/d) to 2.52 Bcf/d as operators have fully recovered from the wildfires in western North Dakota. Infrastructure: Very low ethane cash prices and the steep contango shape of the forward curve in early August ’24 (see graph below) created an incentive for storage operators to buy as much ethane on spot markets as possible and sell the commodity forward. Purity Product Spotlight: EDA believes persistently high ethane stocks, combined with modest growth in ethane supply from 2024 to ’25 (refer to the below chart) – without any meaningful near-term demand – will push prices lower than the forward curve.

Rigs:

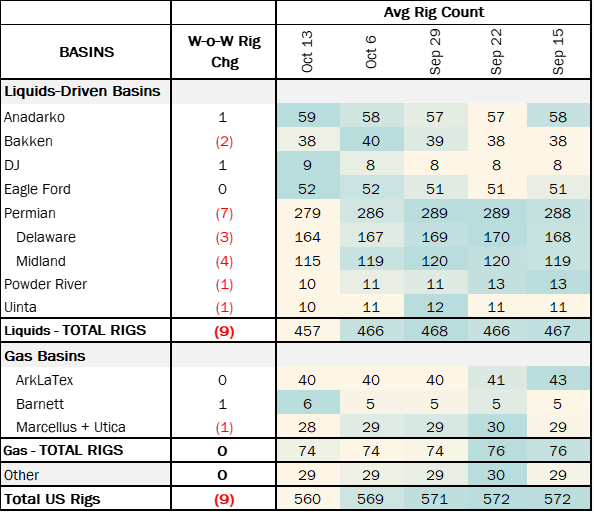

The total rig count decreased by 9 for the October 13 week, down to 560 from 569. Liquids-driven basins declined by 9 rigs W-o-W.

- Permian – Delaware (-3): EOG Resources (-2), APA Corp (-1), Chevron (-1), Diamondback (+1).

- Permian – Midland (-4): Diamondback (-1), Exxon (-1), Cholla Petroleum (-1), Seaboard Operating (-1).

- Bakken (-2): Marathon Oil (-2).

Flows:

The Bakken gas sample continues to rebound, increasing by 3% W-o-W (+76 MMcf/d) to 2.52 Bcf/d as operators have fully recovered from the wildfires in western North Dakota. While there were disruptions to supply in the basin due to well shut-ins, Northern Border Pipeline saw increased inbound flows from Canadian production (Port of Morgan).

The Permian sample increased 3% (+167 MMcf/d) for the October 27 week. Next week, we expect a drop in on pipeline sample as El Paso Natural Gas (EPNG) conducts maintenance. EPNG has detected anomalies on Line 1100 downstream of its Pecos River compressor station, requiring repairs that will limit pressure and reduce operational capacity. Starting October 24, 2024, capacity through the Pecos constraint will be reduced by 133 MMcf/d, and through the Guadulupe constraint by 91 MMcf/d. EPNG will issue maintenance updates and keep the capacity reduction in place until further notice.

Infrastructure:

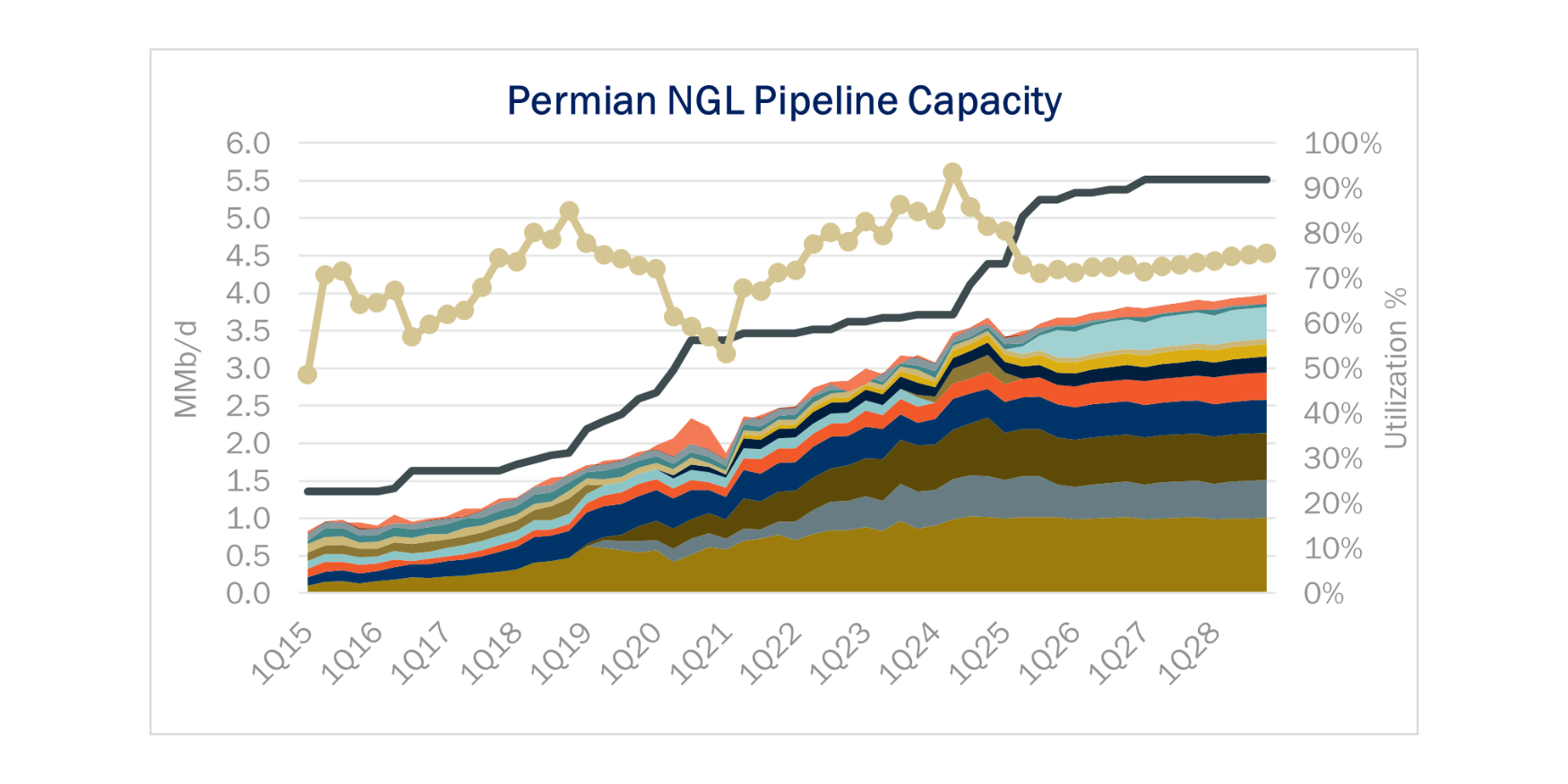

Very low ethane cash prices and the steep contango shape of the forward curve in early August ’24 (see graph below) created an incentive for storage operators to buy as much ethane on spot markets as possible and sell the commodity forward. ONEOK (OKE) just reported earnings, and acknowledged a $45MM decrease in 3Q24 earnings on sales of purity NGLs held in inventory (likely ethane). OKE “expects an earnings benefit on the forward sales of inventory over the next two quarters”.

The steep contango in ethane bodes well for others that secured storage space, including asset operators like Enterprise Products (EPD), Energy Transfer (ET) and Targa Resources (TRGP). These companies likely traded around their valuable storage facilities in 3Q24.

Purity Product Spotlight:

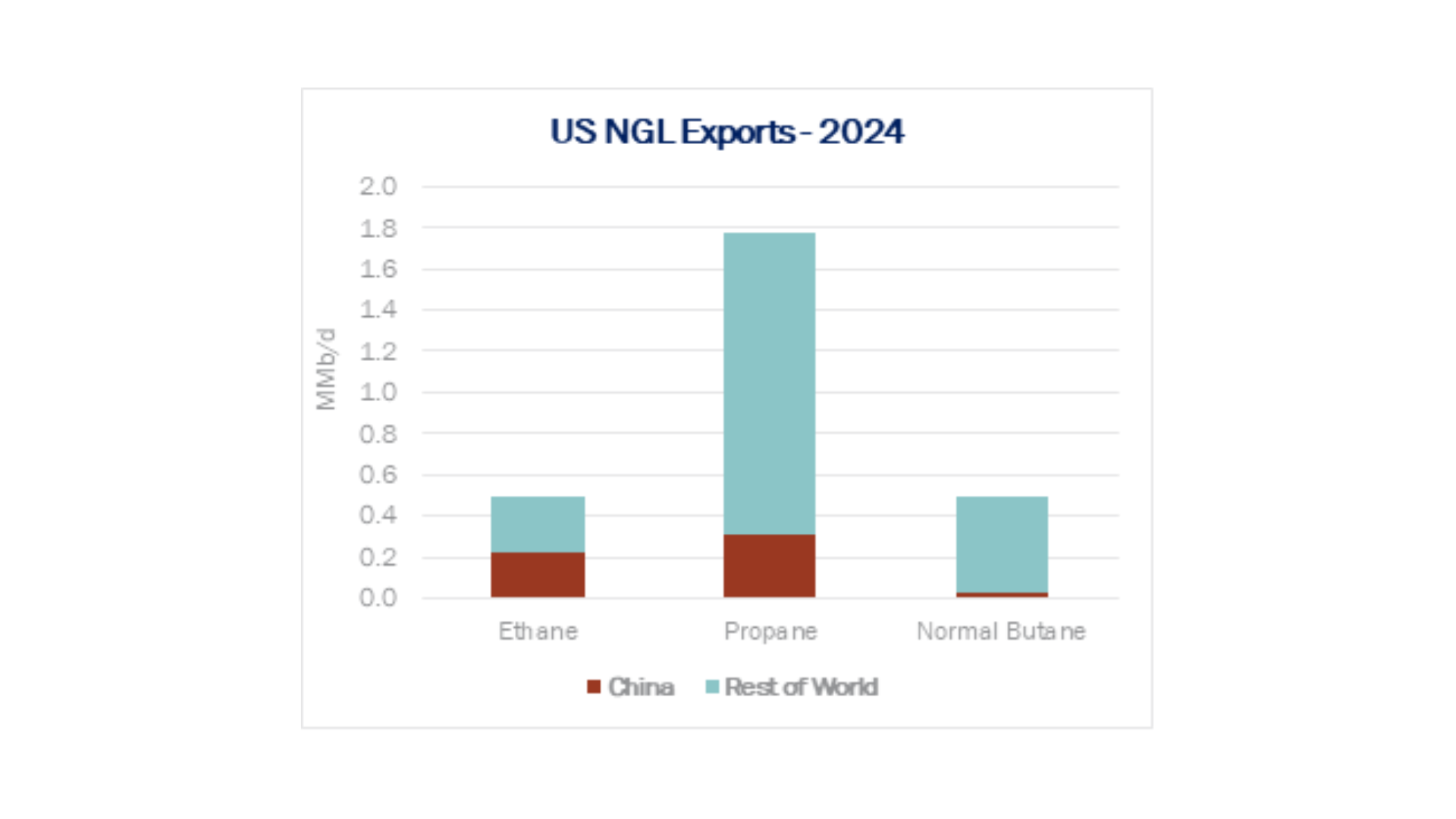

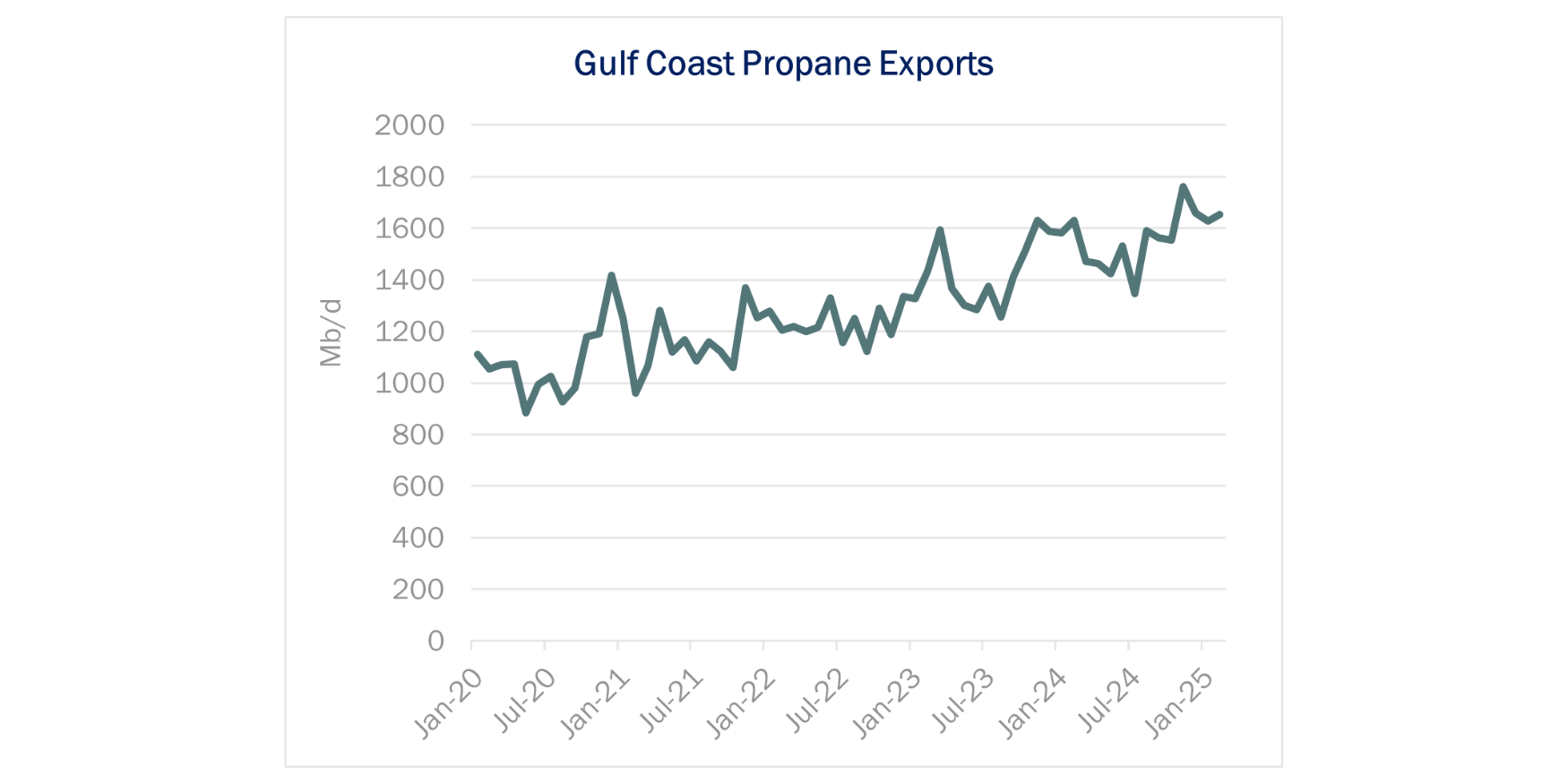

EDA believes persistently high ethane stocks, combined with modest growth in ethane supply from 2024 to ’25 (refer to the below chart) – without any meaningful near-term demand – will push prices lower than the forward curve. This will lead to more ethane rejection at the end of 2024 and into 2025, especially in the Anadarko Basin. The next meaningful capacity expansions on the demand side do not occur until the end of 2025 (Neches River).

The CP Chem / Qatar Golden Triangle Polymers plant in Orange County, TX has an assumed ISD of Jan ’27, with ethane demand capacity of 130 Mb/d.

Our understanding of the Energy Transfer (ET) Marcus Hook expansion is that the project has been shelved until there are enough committed volumes to support it (we previously estimated 25 Mb/d of capacity available in mid-’25).

Data Points & Product Release Calendar: