Infrastructure – Energy Transfer (ET) could reach a final investment decision (FID) on the Warrior Pipeline project within weeks, management said on the company’s 3Q24 earnings call. While we appreciate the value of Warrior for its interconnectivity to gas markets beyond Carthage, the additional capacity would overbuild egress from the Permian Basin in 2027 and crush Waha spreads.

ET likely would prefer to own a fee-generating asset than protect its own marketing earnings, but we would be surprised if Permian producers are willing to do the same. If Mexico Pacific LNG reaches FID (expected in early 2025), and thus ONEOK (OKE) moves ahead with its Saguaro pipeline, the basin will have plenty of capacity through 2030.

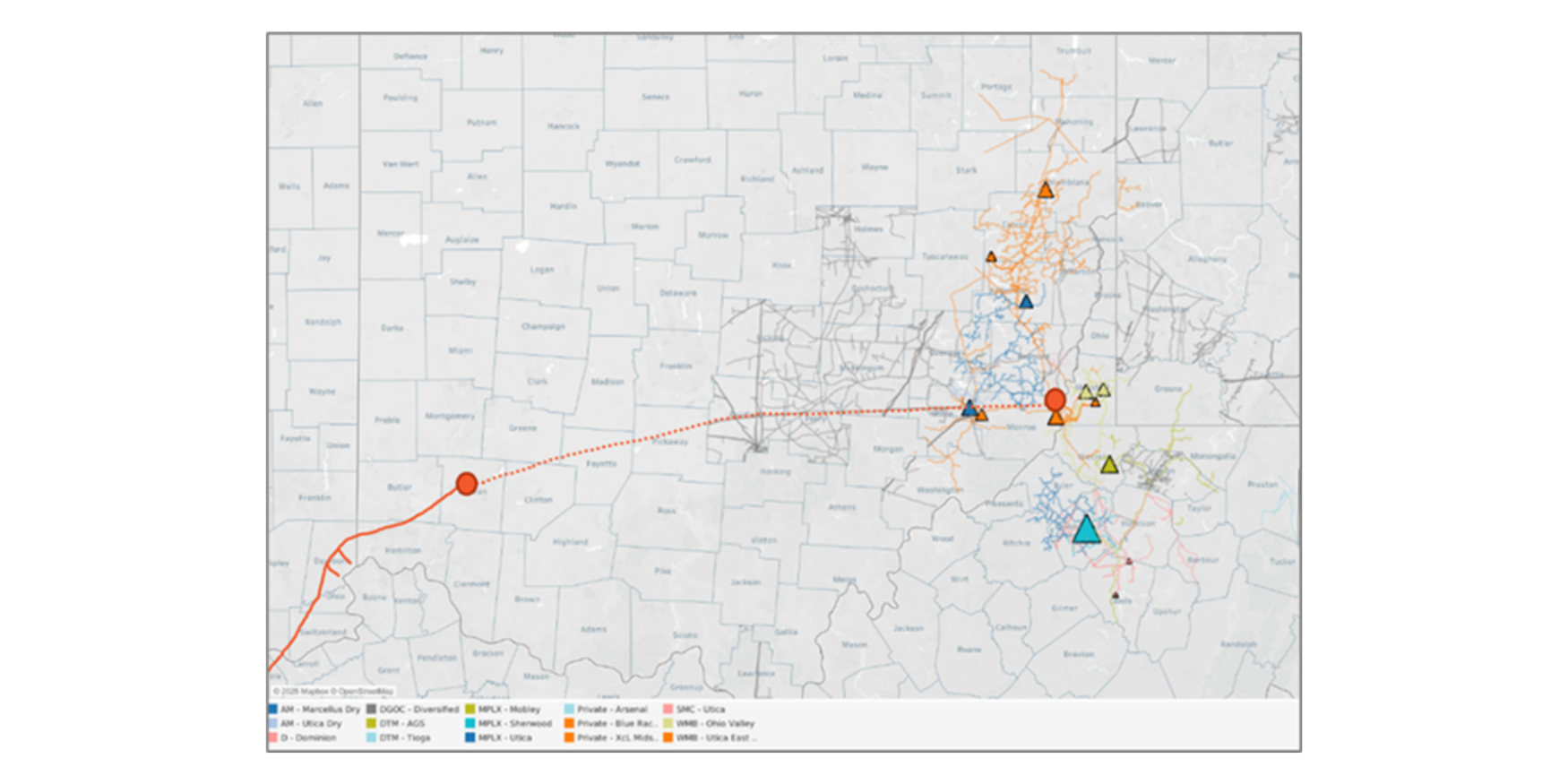

East Daley Analytics tracks the Warrior and Saguaro projects in the Permian Basin Supply & Demand Report. The figure shows the outlook for gas production and pipeline takeaway from the monthly Permian forecast, including the 1.5 Bcf/d-2.0 Bcf/d Warrior project. The Matterhorn Express Pipeline began delivering gas in October, and a group led by WhiteWater Midstream has taken FID on a new project, the 2.5 Bcf/d Blackcomb Pipeline.

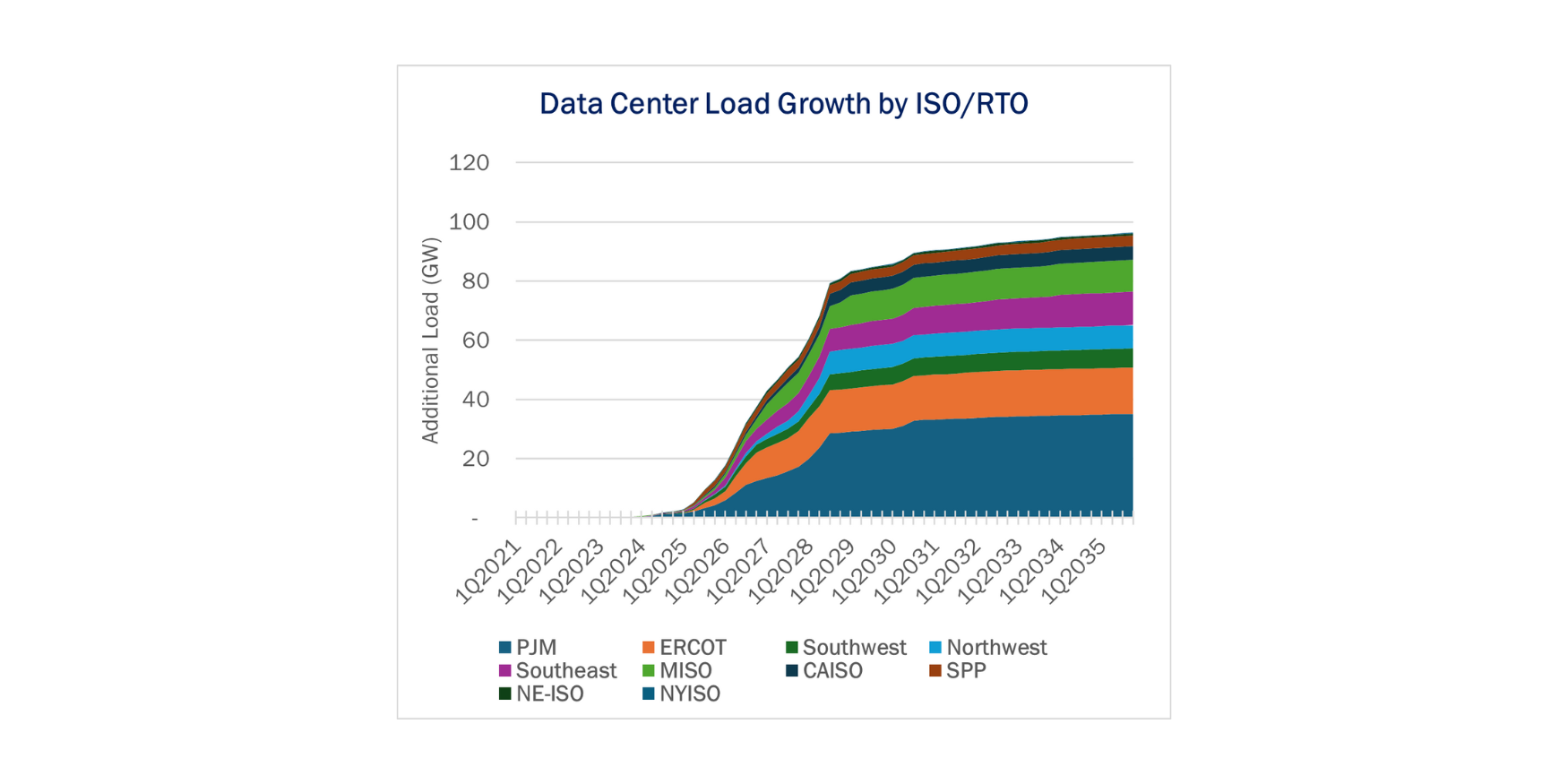

So, why would ET still build Warrior? One answer is data centers and increasing power demand in the Dallas-Fort Worth area, where Warrior terminates. ET’s management hinted as much, saying contracting is “weighted a little bit heavier towards market pool than it is on producer push.â€

Unlike producers, demand-pull customers like electric utilities do not care about overbuilding the basin as much as securing supply. With ever-increasing demand estimates from data centers and general population growth, Texas will need a lot generation capacity, and natural gas plants will be a part of the solution.

The Electric Reliability Council of Texas (ERCOT) predicts that monthly peak generation capacity will need to grow 72% by 2030 to meet demand, from 86 GW in 2024 to 148 GW. Those estimates are much higher than other forecasts by independent system operators (ISOs), and we would not be surprised if a more conservative figure materializes. Nonetheless, we expect a large increase in power (and thus natural gas) demand ahead.

The theme of higher power demand is starting to crystalize into real investments, and ET could be an early winner with Warrior.

Flows – Gas prices are creeping up in anticipation of the winter’s first cold front (see Storage below), yet producers remain wary of market imbalances ahead. Major Haynesville producers have guided to flat production in 2025, reflecting some caution after oversupply and poor prices in 2024.

However, East Daley has a sunnier view in the Macro Supply & Demand Forecast. We forecast some growth out of the Haynesville to meet new demand from Plaquemines LNG in early 2025.

Comstock Resources (CRK) has dropped 2 rigs since 1Q24 and is currently operating 5 rigs in the ArkLaTex Basin, 3 of which are drilling on CRK’s exploratory Western Haynesville play in East Texas. On CRK’s 3Q24 earnings call, management said it expects to see production decline heading into 2025, based on rig activity trends.

Expand Energy (EXE; formerly Chesapeake and Southwestern) reported ~1 Bcf/d of spare productive capacity will be available at YE24 from its drilled but uncompleted wells (DUCs) and deferred turned-in-line wells (TILs). Management guided to a maintenance drilling program of ~12 rigs to hold production flat at 7 Bcf/d, excluding flexible production from DUCs and TILs. On EXE’s inaugural earnings call, CEO Nick Del’Osso said that, based on the current macro picture, the producer expects “supply is going to be flat to down†and “probably remain that way until you see a rig count change.â€

In 2025, East Daley forecasts ~1.5 Bcf/d of new demand coming online by March at Plaquemines LNG in Louisiana. This facility can most easily be supplied by Haynesville gas, so we anticipate a moderate ramp in production in early 2025 to meet this new demand.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a net 8 Bcf storage injection for the week ending November 8, according to a survey by The Desk. An 8 Bcf injection would increase the surplus to the 5-year average by 24 Bcf to 252 Bcf, and would mark the fourth consecutive week that the surplus has grown. The surplus to last year would increase by 4 Bcf to 154 Bcf.

Storage facilities are likely to report the first net storage withdrawal for the week ending November 22, with early estimates predicting a -8 to -15 Bcf draw in that EIA survey. This would still be a smaller withdrawal than the 5-year average and put the market on course for a fifth consecutive week of a building surplus.

The end of November looks to be cooler than previously forecast, and December prompt futures have responded to the upside. On Monday and Tuesday (November 19-20) the December ’24 Henry Hub contract increased by over $0.22/MMBtu as weather forecasts turned bullish for Nov. 28 – Dec. 5. Updated models show temperatures falling below the 30-year normal as a cold front descends across most of the Lower 48. The December, January ‘25 and February ’25 contracts are all now well above the $3/MMBtu mark, a good sign for a production rebound and in line with East Daley’s Macro Supply & Demand Forecast.

Rigs – The US rig count decreased by 10 for the November 9 week, holding at 550. Basins losing rigs W-o-W include the Anadarko (-4), Bakken (-2), Permian (-2), ArkLaTex (-1) and Marcellus+Utica (-1). The large W-o-W drop in the Anadarko Basin is most likely due to rig moves and should recover next week.

On the midstream side, Targa Resources (TRGP) is down 6 rigs on its Midland, Delaware and Eagle Ford systems. Enterprise Products (EPD) lost 3 rigs total on its Permian, Eagle Ford and ArkLaTex systems.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.