Infrastructure – New natural gas demand is coming into focus to feed AI and data centers, and the Permian Basin looks to play a leading role. East Daley Analytics sees a potential connection between the Stargate Project, the OpenAI infrastructure project recently rolled out with much fanfare, a new Chevron power initiative, and Energy Transfer’s (ET) latest pipeline project.

EDA tracks data center projects in Texas and across the US in the new Data Center Demand Monitor. Many are on our radar. For example, Chevron (CVX) on Jan. 28 announced a partnership with Engine No. 1, and GE Vernova to build up to 4 GW of scalable gas-fired generation to power AI. The group plans to build co-located power plants at data centers and target customers in the Southeast, Midwest and West regions.

This follows President Trump’s announcement of the $500B Stargate Project to build AI infrastructure across the US, starting with a massive 5 GW project near Abilene, TX. The partnership with tech companies OpenAI, SoftBank and Oracle plans to invest $100B immediately, including its ‘flagship’ project in Abilene to feed new data centers, an OpenAI executive told Reuters.

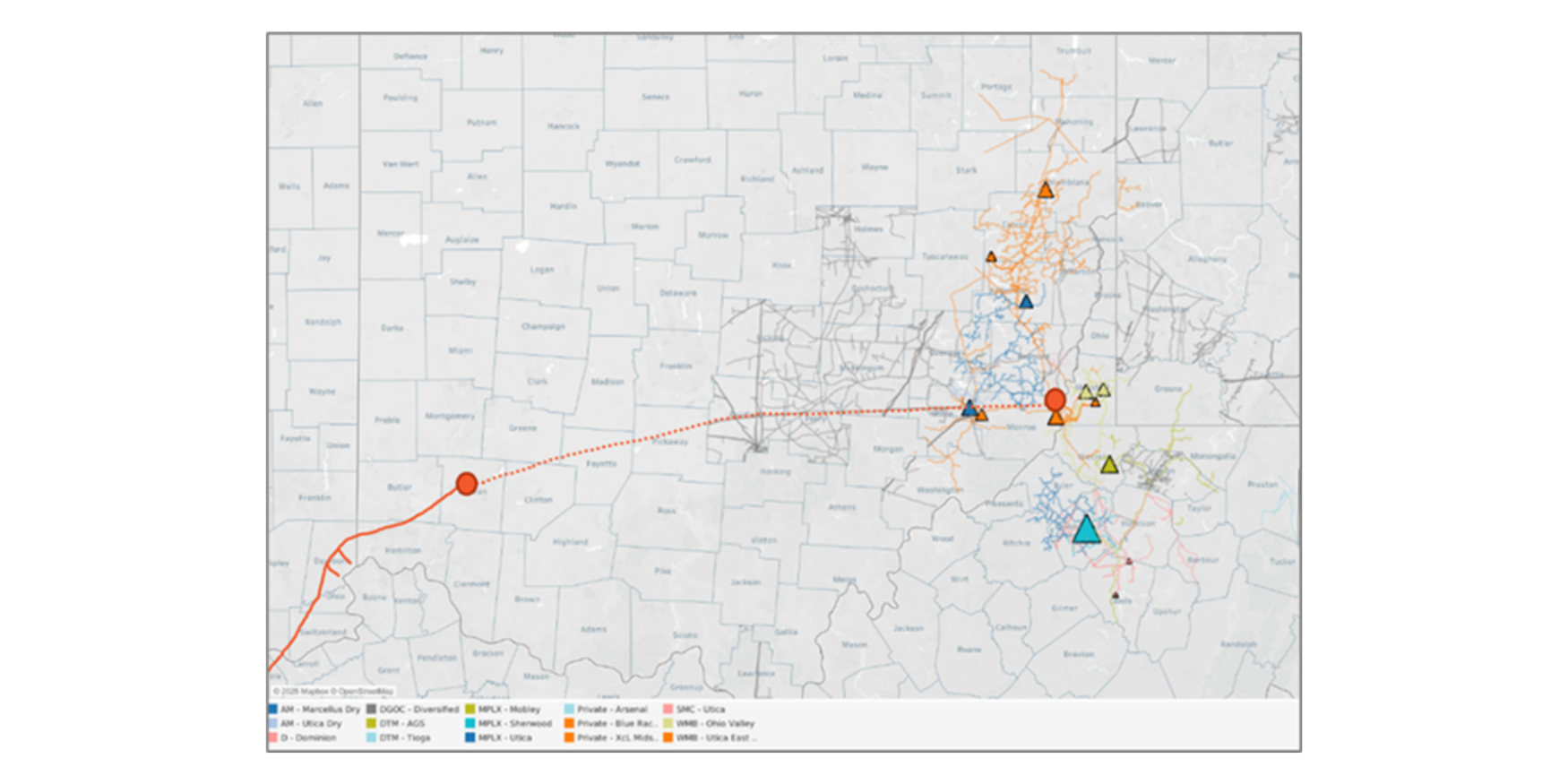

East Daley’s new Data Center Demand Monitor reveals a new infrastructure corridor emerging from West Texas to feed AI-driven energy demand (see figure). Energy Transfer’s (ET) Hugh Brinson Pipeline (formerly the Warrior Pipeline) will travel near Abilene, and we speculate that the new 1.5 Bcf/d project will help meet this emerging demand center. ET announced a final decision on the Hugh Brinson project in December ‘24.

Chevron’s power plants, expected to be operational by 2027, will use GE Vernova 7HA natural gas turbines, the same turbine model confirmed for Stargate’s first onsite power plant. Site selections have not been announced, but the shared technology and regional alignment point to a connection between the CVX venture and Stargate.

Stargate’s Abilene data center project is expected to scale from 1.2 GW to 5 GW, making it one of the largest power-intensive AI clusters in the world. Developers have already submitted permits for a 360 MW natural gas power plant, reinforcing the trend of co-locating dedicated energy infrastructure with AI demand. At full scale, Stargate’s 5 GW demand could consume ~0.66 Bcf/d of natural gas (assuming 100% gas-fired power).

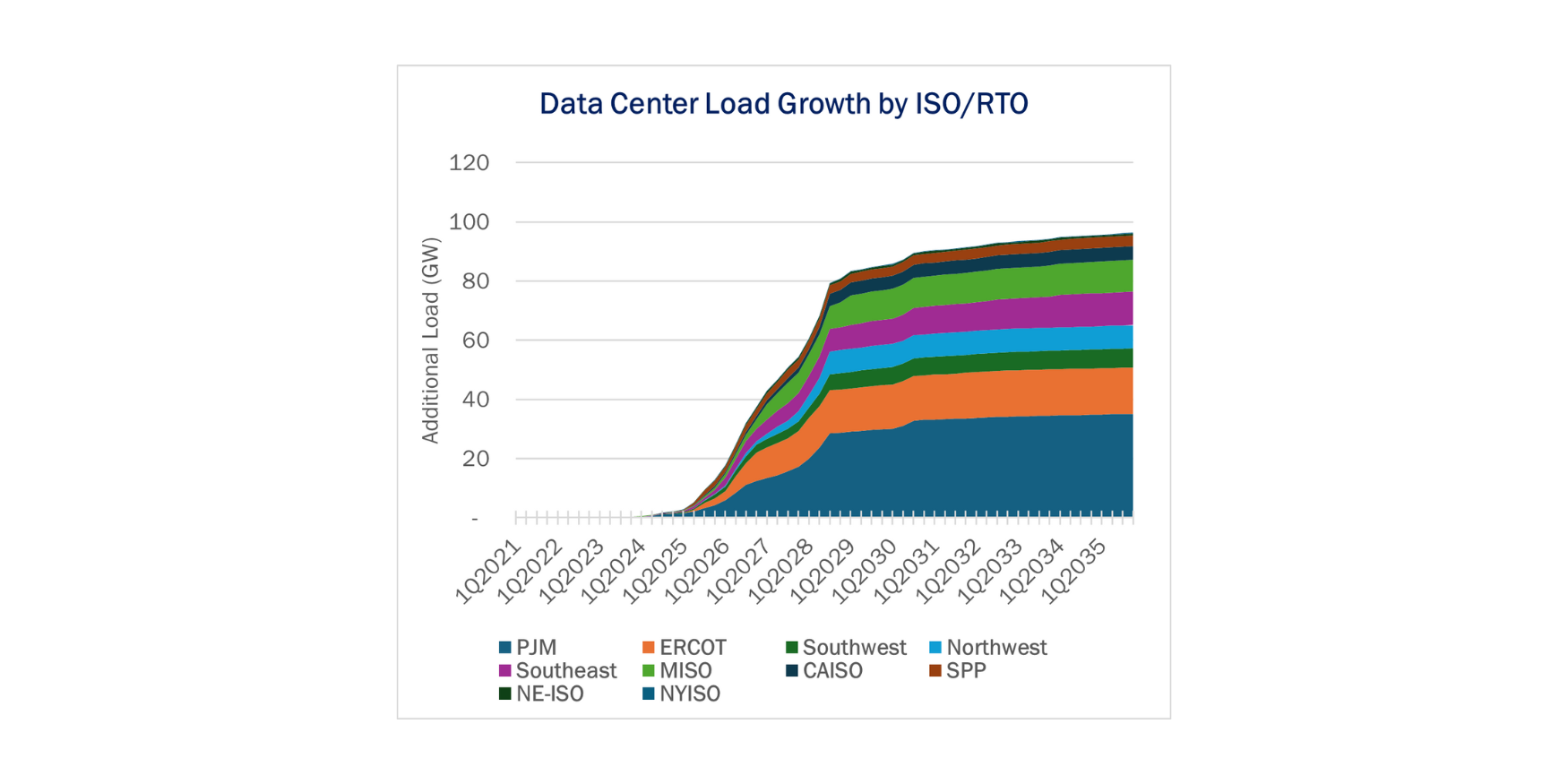

Available in Energy Data Studio, the Data Center Demand Monitor gives a bottoms-up approach to quantifying natural gas demand for data centers. East Daley tracks and maps nearly 300 projects by county across the US to visualize where demand could materialize. The new data center tool is available now as part of the Macro Supply & Demand package - reach out to learn more.

Rigs – Earlier this week, BP announced it was “contemplating increasing rigs†into a “very, very solid†natural gas forward strip in late 2025 and 2026.

According to Bloomberg pricing data, Henry Hub averaged $4.12/MMBtu during a cold January and the December ’25 contract currently sits at $4.49, averaging $3.94 in 2026. The curve is well above East Daley’s estimate of a ~$2.40 breakeven for core Haynesville acreage, and would even support development of emerging acreage to turn a profit at an estimated $3.75 breakeven.

Accordingly, East Daley is bullish on Haynesville growth. We expect rigs to grow from 36 to 72, and model residue gas production topping 17 Bcf/d by the end of 2025. This growth will be needed to balance a market with an incremental ~3 Bcf/d of LNG demand growth by YE25 from Plaquemines LNG Phase 1 and Corpus Christi Stage 3, and another 2.7 Bcf/d from Golden Pass LNG by YE26. Plaquemines has been flowing 1.2 Bcf/d through the first two months of 2025, signaling that after an extended lull, the LNG infrastructure wave is finally here. The additional demand along with a cold winter has put US natural gas storage into a deficit (to the 5-year average) for the first time in two years, and East Daley expects this deficit to persist into mid-2026.

The question remains: Who will bite first at $4 prices? BP has already signaled that the current price environment is favorable. But some of the larger Haynesville producers aren’t so eager. Aethon, the largest private producer in the Haynesville, said earlier this month that it will need prices to top $5/MMBtu to justify new development. Expand Energy (EXE) also said prices need to climb “materially higher†than a $3.50 breakeven before it would consider bringing online new production. Aethon and EXE are currently running 7 rigs each in the basin, by our count. Comstock Resources (CRK), the other “Haynesville major,†is furiously drilling its western Haynesville exploratory play, running 4 of its 6 rigs on that acreage.

At the moment, Haynesville producers appear to be playing a game of chicken. Prices are strong enough to turn a profit. But if they commit to an aggressive drilling program and demand doesn’t materialize fast enough, they could end up struggling to pay for it and be punished by investors. On the other hand, more nimble producers could find profit in the forward curve, adding needed incremental supply and delaying the $5-handle the big fish are waiting for.

Infrastructure – Waha gas prices are likely to face pressure in the last week of February as Kinder Morgan’s (KMI) El Paso Natural Gas Pipeline (EPNG) will take 756 MMcf/d of capacity offline for maintenance. The work on EPNG will take place at the North Mainline compressor station from February 24-27.

Major pipeline maintenance events historically have contributed to brief but sharp price declines at the Waha hub, driven by limited egress capacity from the Permian Basin. However, Matterhorn Express is now in service and has expanded Permian takeaway, so maintenance events like these should have less impact on prices going forward.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report an 89 Bcf storage withdrawal for the week ending February 7. An 89 Bcf draw would be 29 Bcf greater than the 5-year average and would increase the deficit to 140 Bcf. The storage deficit to last year would expand to 163 Bcf based on the consensus estimate.

Weather models for February point to colder temperatures that would result in gas-weighted heating degree days (GWHDDs) equal to or higher than the 30-year and 10-year norms. The figure presents end-of-season storage scenarios for cold and warm weather, along with East Daley’s base case in the Macro Supply & Demand Report. The latest forecasts for February suggest the cold case could be winning out. Prices have responded with Henry Hub cash rising over $0.50/MMBtu since last Friday (+17%). The prompt-month March contract on NYMEX also jumped about $0.40 over the same time period (+13%).

While this may not be the coldest winter on record, it is certainly rivaling the winters of ’20-21 and ’21-22. Our storage deficit forecast shows the delta between our base case (using normal weather) and the ultra-cold Winter ’13-14 case. The trajectory appears to be somewhere in between should a cold February be realized. This points to stable or increasing prices for producers and a warning to natural gas consumers of what is yet to come.

Flows – Matterhorn Express Pipeline delivered back-to-back record volumes to interstate pipelines earlier this month, flowing 1.53 Bcf/d on Feb. 2 and topping 1.535 Bcf/d on Feb. 3. February has been a strong month for Matterhorn, with the first 10 days of the month all posting flows in the top 20, including eight days of the top 10.

Matterhorn had previously delivered 1.525 Bcf/d to interstates back in early November before Tennessee Gas Pipeline’s interconnect had even come online. At the time, both El Paso Natural Gas and Permian Highway Pipeline were undergoing maintenance that limited Permian egress and made more gas available for Matterhorn to flow from the basin.

East Daley expects Matterhorn volumes to stay in the 1.5 Bcf/d range through April, with a steady ramp to full capacity beginning in May ’25 as increasing Permian production provides more associated gas for shippers to send to the Gulf Coast. Check out our Permian and Houston Ship Channel S&D products for updates on Matterhorn.

Rigs – The US rig count decreased by 1 for the February 1 week, standing at 529. The Anadarko (+2), Eagle Ford (+1) and Bakken (+1) added rigs while the Permian (-3) and ArkLaTex (-1) lost rigs on the week.

On the midstream side, Western Midstream (WES) is down 2 rigs net with losses on all its Permian and DJ systems. Phillips 66 (PSX) added 2 rigs total on its Midcon and Eagle Ford systems.

East Daley’s weekly Rig Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Rig Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.