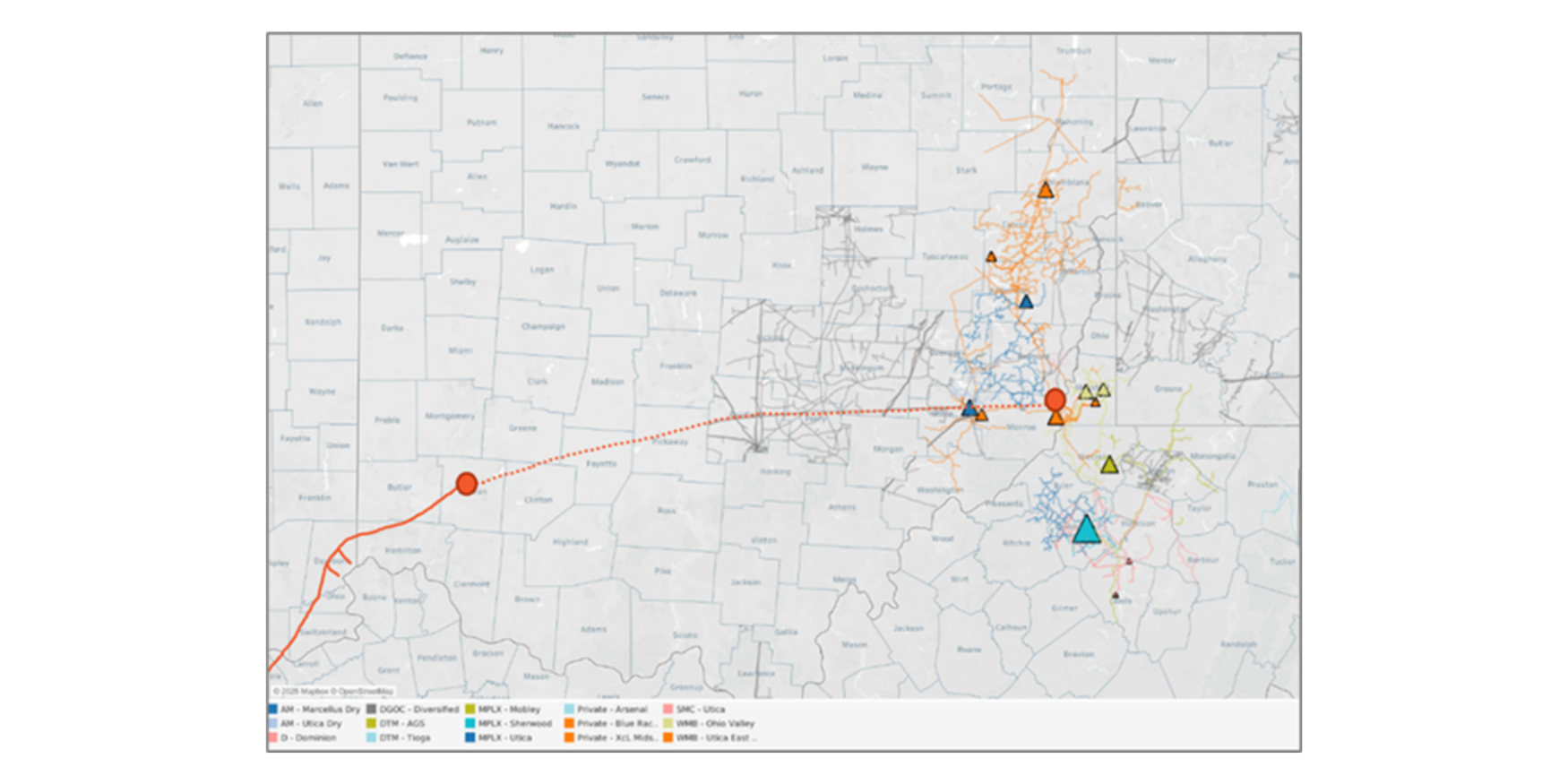

Infrastructure – Gulf Coast Midstream Partners (GCMP) is holding an open season to gauge interest in a salt cavern storage hub near Freeport, TX. The storage project would take advantage of new gas infrastructure in the region, including the Matterhorn Express Pipeline.

Houston-based GCMP is seeking bids for the Freeport Energy Storage Hub (FRESH) in Fort Bend County, TX. The project envisions building a 30-inch header pipe, the Wharton Lateral, over 32 miles to connect up to 17 intra- and interstate pipelines to a new salt dome. The non-binding open season will run from October 1 to October 24, 2024.

GCMP is permitting FRESH as a Texas intrastate natural gas storage facility offering service to interstate shippers. FRESH filed its storage application with the Texas Railroad Commission in January 2024 and expects to receive a storage permit by YE24. The developer plans to make a final Investment Decision (FID) by 3Q25 and is targeting in-service as early as mid-2028.

Infrastructure – Federal regulators have sided with Williams (WMB) in a dispute with Energy Transfer (ET) over authority for the Louisiana Energy Gateway (LEG) project, breaking a logjam that had stalled a key pipeline to meet new LNG export demand.

On September 27, the Federal Energy Regulatory Commission (FERC) determined that LEG is an intrastate system and not subject to federal jurisdiction under the Natural Gas Act, denying a show cause petition filed by Energy Transfer. The company had argued the Haynesville egress pipe should be regulated by FERC as an interstate transmission line, rather than as a gathering extension as claimed by WMB.

The FERC decision is another win for Williams in its dispute with ET over the LEG project. In June, Louisiana district courts ruled for WMB over LEG rights-of-way that cross ET’s pipelines in the state.

With these major regulatory fights out of the way, the risk significantly declines of capacity constraints out of the Haynesville in 2025. In the Southeast Gulf Supply & Demand Forecast, East Daley Analytics currently sees about 6.1 Bcf/d on average (~86% utilization) flowing from the Haynesville to the Louisiana Gulf Coast through June ’25, when egress capacity tightens briefly as Haynesville supply ramps to meet incremental LNG demand from Plaquemines LNG. We have delayed the in-service for Golden Pass LNG Train 1 until January ’26 following the recent bankruptcy of contractor Zachary Holdings, so any potential Haynesville egress constraint will be independent of Golden Pass LNG demand.

Along with LEG, Momentum Midstream’s New Generation Gas Gathering (NG3) project was challenged by ET over pipeline crossings, but ET and Momentum settled that dispute in June ’24. Assuming LEG and NG3 come online in July ’25, the region should have sufficient latent capacity to meet incremental LNG demand until late 2027.

But to meet demand after 2027, developers will need to reach a final investment decision (FID) on other projects. NG3, DT Midstream’s (DTM) LEAP, and ET’s Gulf Run Pipeline have announced potential expansions that could ease constraints on this route, in excess of 5 Bcf/d across all three pipes.

If either LEG or NG3 are delayed past 2H25, expect to see NGPL-TXOK prices weaken significantly until new capacity opens up. See our Southeast Gulf Supply & Demand Report for basis forecasts and more information.

Flows –Pipeline samples mostly held flat W-o-W at ~68.3 Bcf/d for the October 6 week. Anadarko gas samples fell 1% W-o-W, likely linked to operating constraints at Segment 15 on Natural Gas Pipeline of America (NGPL). Maintenance work on the LA#1 Line (Segment 25) is scheduled through October 31, which may disrupt ArkLaTex supply in the coming weeks.

The Bakken gas sample has been declining since mid-September, primarily due to displacement of inbound Canadian flows via the Alliance and Northern Border pipelines. Enhanced processing and pipeline capacity, including the Bear Creek gas processing plant and the Elk Creek NGL pipeline, have allowed for an increase in basin gas flows, further pushing out Canadian supply.

Gas flows in the Permian Basin have been relatively stable since mid-September. However, the region may face disruptions when Northern Natural Gas (NNG) holds scheduled maintenance in October, reducing capacity at points such as El Paso/NNG Waha, Permian Highway Waha, and GCX/NNG Waha. Similar limitations will affect Oasis/NNG Waha and ONEOK Westex, leading to decreased throughput and less flexibility until normal operations are restored later in the month.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a 73 Bcf storage injection for the week ending October 4. A 73 Bcf injection would decrease the surplus to the 5-year average by 23 Bcf to 167 Bcf. The surplus to last year would fall by 12 Bcf to just 115 Bcf.

Injections have trailed the 5-year average for most of the spring and summer, yet storage facilities are still chockablock full in many regions. The Mountain region is near peak operating capacity, and the East and Midwest are both 86% full as of the latest weekly EIA survey.

The South Central region has more flexibility to handle swings. While inventories in non-salt storage are at 84% capacity, South-Central salt caverns are just 62% full. The Pacific region also has some flexibility at just 73% of capacity.

In the latest Macro Supply & Demand Forecast, East Daley expects total US working gas inventory to peak at 3,897 Bcf, or 185 Bcf above the five-year average. Our forecast would mark the highest storage inventory since October 2020, when the Henry Hub spot price averaged $2.39/MMBtu.

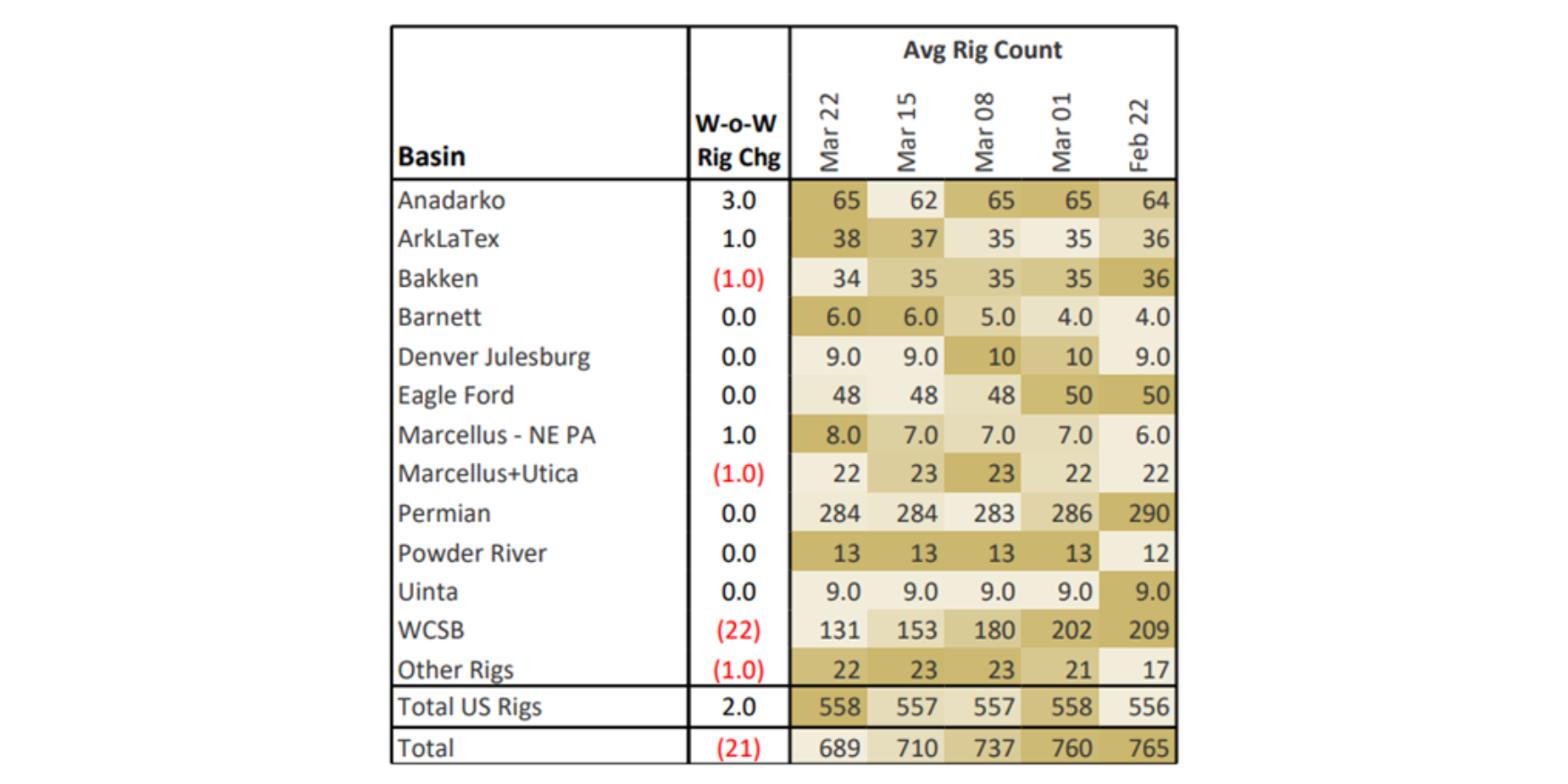

Rigs – The US rig count decreased by 1 for the September 28 week, standing at 566. Basins losing rigs include the ArkLaTex (-2), Anadarko (-1) and Powder River (-1). The Marcellus+Utica added 2 rigs on the week.

On the midstream side, Targa Resources (TRGP) is down 3 rigs on its Delaware and Midland systems. Kinetik (KNTK) gained 2 rigs on its Durango system in the Delaware Basin.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.