Rigs – Producers are returning to core of the SCOOP/STACK play in the Anadarko Basin to capitalize on higher natural gas prices, adding l0 rigs so far in 2025.

Oklahoma’s rig count has climbed from 44 to 54 since the start of the year, according to basin data in East Daley’s Energy Data Studio. The gains are shown in the figure. After hitting a low of 36 rigs in June ‘24, Oklahoma activity plateaued around 45 rigs for the rest of the year.

Meanwhile, interstate pipeline samples for the Anadarko Basin jumped in March to over 4.0 Bcf/d, after holding rangebound from 3.7-3.9 Bcf/d for a long period stretching through 2024 (see figure).

Small private operators are behind the drilling rebound, accounting for 8 of the 10 rig adds in Oklahoma. Major public players Ovintiv (OVV) and Coterra Energy (CTRA) have each brought 1 rig back. Mewbourne and Continental Resources, the two largest private operators, maintain a strong presence and have each steadily operated 7-9 rigs this year.

The increased drilling should boost midstream assets in the Anadarko. The sector has contended with declining G&P volumes in recent years due to depressed gas prices, but a rising market could reverse that trend.

East Daley Analytics allocates rigs by G&P system in Energy Data Studio and in the weekly Rig Activity Tracker. Anadarko-based G&P systems gaining rigs since January include Energy Transfer’s (ET) Enable - Anadarko (+3 rigs), Phillips 66’ (PSX) DCP - Midcon (+2 rigs), ONEOK’s (OKE) COK (+1 rig), and Targa Resources’ (TRGP) South OK (+1 rig)

EDA projects gross gas volumes in Oklahoma will grow by 1% Y-o-Y, reaching 7.7 Bcf/d by YE25. We’ve long been bullish on natural gas in 2025 as LNG projects start, and anticipate a larger role from gas-focused basins like the Anadarko to meet growing demand. The rig gains in the Anadarko show that a supply response has started.

Infrastructure – Permian Basin gas prices have been under severe pressure recently due to pipeline restrictions and weak demand. Waha spot prices went negative in March, and the April Waha futures contract settled at -$0.09/MMBtu.

Pipeline maintenance explains much of the decline. El Paso Natural Gas (EPNG), Gulf Coast Express (GCX) and Permian Highway (PHP) have been performing maintenance since March, cutting egress capacity out of the basin.

Constraints are likely to tighten further in April, when over 1 Bcf/d of Permian egress will be frequently unavailable (see figure). Major maintenance events are scheduled for April 8-11 (GCX to take 820 MMcf/d offline) and April 22-25 (PHP to remove 950 MMcf/d of capacity) EPNG will also perform active maintenance in April and restrict key segments like Line 2000 and the North Mainline. At peak, pipelines plan to take up to 1.8 Bcf/d of pipe capacity offline this month.

Weak demand is also contributing to price pressure. Gas consumption in Texas and the Southwest typically falls to seasonal lows in the spring, when warming temperatures idle furnaces but are still too low to create cooling demand. Reflecting these soft conditions, Transwestern Pipeline issued several critical notices in late March for underperformance in the Phoenix market, citing shippers for taking less gas than they nominated.

Infrastructure – On March 21, the Maritime Administration (MARAD) issued a license to Delfin LNG authorizing the project to construct, operate and export LNG from the US. The permit is a big step for Delfinct, which is still short customers but making headway toward a final investment decision (FID).

Delfin LNG utilizes brownfield deepwater port infrastructure to support three floating LNG export terminals. The project would produce roughly 13.2 mtpa, or ~2 Bcf/d of feedgas equivalent.

Shortly after the MARAD approval, Delfin signed a non-binding Heads of Agreement to supply Berlin-based SEFE (Securing Energy for Europe) with 1.5 mtpa for a 15-year term. The facility still needs roughly 6 mtpa of offtake agreements to meet the 80% contracted threshold at which LNG facilities have historically made FID.

President Trump’s promise to expedite LNG permitting has not been an empty one. Since he took office in January, both Commonwealth LNG and CP2 LNG have received approvals from the Department of Energy for exports to non-FTA countries. With the latest Delfin authorization, the Trump administration has granted approvals to over 6 Bcf/d of LNG projects, all slated to come online before 2030. While these facilities still need to make FID, the approvals are a welcome sign for prospective offtakers.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a 25 Bcf net storage injection for the week ending March 28, reflecting above-normal temperatures across most of the Lower 48. A 25 Bcf injection would be 38 Bcf greater than the 5-year average for the same week and would narrow the deficit to just 84 Bcf, the first sojourn below 100 Bcf since the week ending February 7. The storage deficit versus last year would drop by 62 Bcf to 495 Bcf.

With winter in the rearview mirror, we set our sights on the storage refill season ahead. East Daley has plotted three scenarios in the Macro Supply & Demand Report: our base case, a cold summer case and a warm summer case. In the graph, we highlight how each scenario would play out through the end of October ‘25.

Our base case assumes 10-year normal weather for the summer and projects storage ending October with a 34 Bcf surplus to the 5-year average, not far from where we stand today. The summer of 2014 was the coldest summer of the past 10 years and would result in a storage surplus of nearly 670 Bcf, assuming no changes to production in the face of rapidly declining prices. Last summer (June-August) was the warmest of the past 10 years (and all time). That same injection pace would leave the Lower 48 at a deficit of nearly 375 Bcf, leading to higher prices heading into 4Q25. This is the likelier scenario of the two, given the warm summers we’ve seen in recent history.

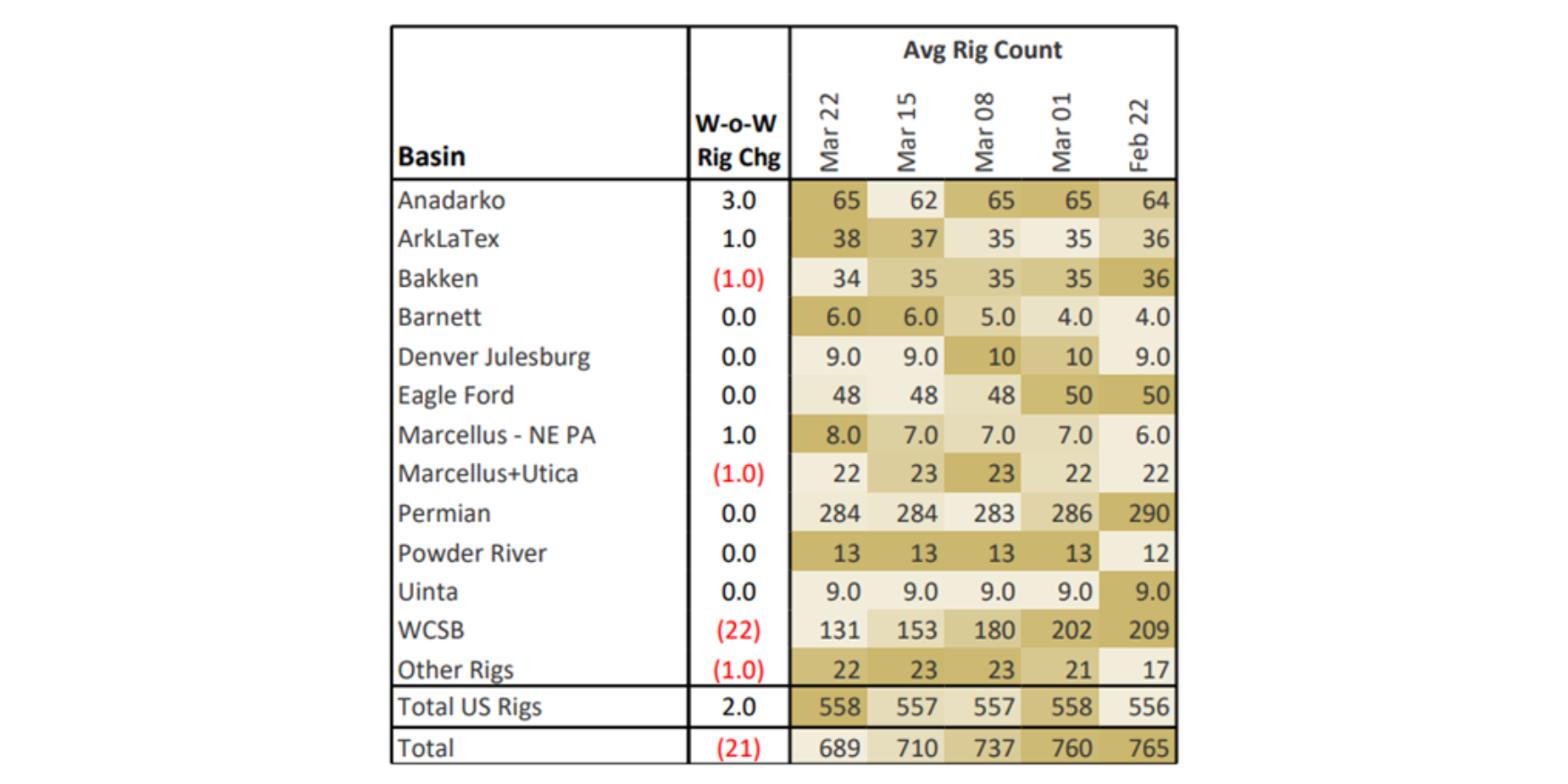

Rigs – The US rig count increased by 2 for the March 22 week, standing at 558. Basins adding rigs include the Anadarko (+3), ArkLaTex (+1) and Marcellus NE-PA (+1). The Bakken and Marcellus+Utica each lost 1 rig on the week.

On the midstream side, Enterprise Products (EPD) is down 6 rigs total with losses on its Permian, Eagle Ford, San Juan and Piceance systems. Phillips 66 (PSX) is up 3 rigs total with additions on its DJ, Midland and Delaware systems.

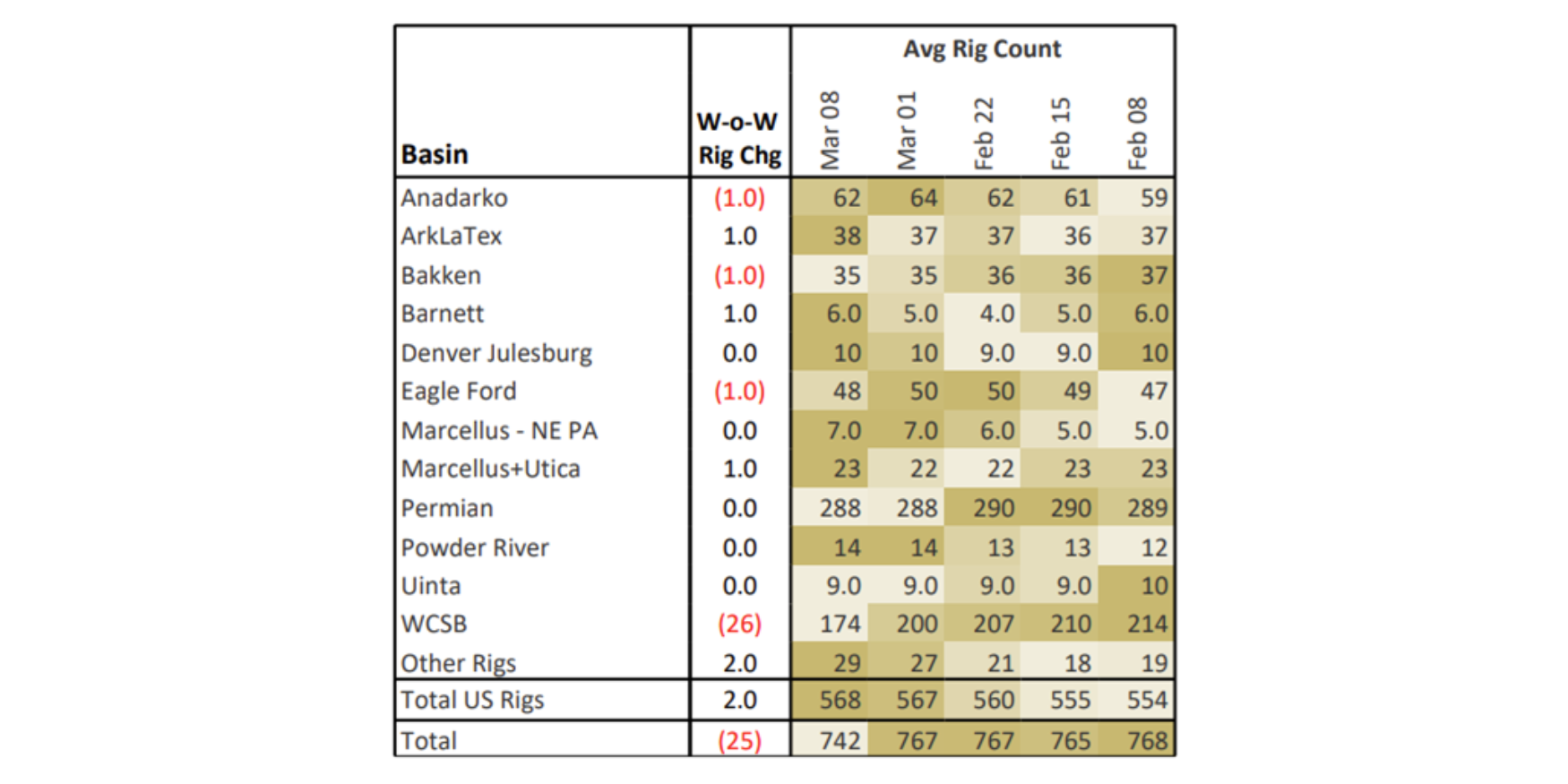

East Daley’s weekly Rig Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Rig Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.