Flows – Flows out of the Haynesville indicate that production is starting grow again, but we still have a ways to go to balance the market. In the Macro Supply & Demand Forecast, East Daley is calling for ~1.2 Bcf/d of additional supply out of the Haynesville this year to support rapidly growing demand from Plaquemines LNG and Golden Pass LNG in 2026.

Pipeline flow samples in the Haynesville show an increase of ~550 MMcf/d between January and March ’25. We have observed most of the gains on DT Midstream’s (DTM) Blue Union system and Energy Transfer’s (ET) Enable-Louisiana system, both of which gather most of their volumes from Expand Energy (EXE). Our assumption is that EXE has started working through its deferred inventory in response to stronger prices and increasing LNG demand.

Last month, Expand released early 2025 guidance affirming its plan to grow. The operator produced 6.4 Bcf/d in 4Q24 across the Northeast and Haynesville. EXE expects production to average ~7.1 Bcf/d in FY25 and to exit the year at 7.2 Bcf/d after working through all the deferred capacity built up in 2024. Of that 7.1 Bcf/d, roughly 2.9 Bcf/d is in the Hayneville.

EXE intends to build another 300 MMcf/d of production capacity by running up to 15 rigs in 2H25, taking potential production up to 7.5 Bcf/d in 2026. That 7.5 Bcf/d is essentially what EXE views as the equilibrium production level given a $3.50-$4/MMBtu gas price.

Aethon, the largest private producer in the Haynesville, is guiding to maintenance production and calling for higher prices before it ramps up drilling. At CeraWeek 2025, Aethon President Gordon Huddleston said that $5/MMBtu prices need “to carry on beyond ’26 into ’27 and ’28.†Currently, 2026 Henry Hub futures are averaging just under $4.50, but are sitting at $3.75 in ’27-’28. Aethon is currently operating just 4 rigs in the Haynesville, down from 7 in 2024.

Comstock Resources (CRK), the other large public, is focused on developing its Western Haynesville play. CRK is operating 4 rigs on that acreage, but plans to run 2-3 rigs on legacy Haynesville acreage to grow production in 4Q25. BP on the other hand sees the current forward strip as an opportunity to grow production. However, BP’s Haynesville presence is relatively limited, running just 2-3 rigs in the play.

East Daley does not believe that maintenance production levels will be enough to support demand growth in 2025 and 2026. Our analysis in the Macro Supply & Demand Forecast points to significant price increases at Henry Hub should production fail to materialize. In our unbalanced view of production, where rig activity is correlated to the forward strip, we see a scenario in which prices could skyrocket to as high as $8/MMBtu (see figure). That would certainly incentivize production growth, but we think the more likely scenario is somewhere between our balanced and unbalanced forecasts. A supply shortage would bump prices in the near term until producers are confident that more demand (from Golden Pass LNG in particular) will arrive.

Infrastructure - Cheniere Energy (LNG) has achieved substantial completion of Midscale Train 1 at the Corpus Christi LNG site. The train is the first of seven for the Stage 3 expansion, which is expected to drive an additional 1.3 Bcf/d of demand (~10.5 mtpa of LNG production) once fully online in 2H26.

Cheniere announced the milestone Monday (March 17). Flows on Corpus Christi Pipeline haven’t shown a sizeable increase since Train 1 achieved first liquefaction back in December ’24, despite ~500 MMcf/d of available capacity (see figure).

Additional volumes for the Stage 3 project are likely coming from the 1.7 Bcf/d Agua Dulce Corpus Christi (ADCC) intrastate pipeline that entered service this past summer. ADCC was specifically designed by WhiteWater Midstream and Cheniere to support the Stage 3 expansion, and it appears so far that Cheniere intends to source gas for the project exclusively from that pipe.

East Daley follows the Stage 3 expansion in the Houston Ship Channel Supply & Demand Report. Recent satellite imagery from Sunday (March 16), showed no indication that Train 2 had begun producing LNG yet. However, Cheniere said in its 4Q24 earnings presentation that “~20% of Train 2 systems [were] turned over to commissioning and start-up teams who are beginning to place those systems into service.†Trains 2 and 3 are expected to ramp in 2025, so Train 2 should begin production in the coming months.

Additionally, Cheniere’s second expansion project at Corpus Christi, Midscale 8 and 9, was authorized by FERC last week. The project would add two more midscale trains to the seven currently under construction, as well as increase the authorized loading rate at the facility’s existing marine berths. The new trains would be able to liquefy about 470 MMcf/d of additional gas. In last month’s earnings call, Cheniere stated it was expecting to achieve a final investment decision (FID) on the project sometime later this year.

Infrastructure – Permian gas prices have been under heavy pressure due to seasonal pipeline maintenance that is curtailing volumes out of the basin.

Waha spot prices traded at -$0.82/MMBtu last Friday (March 14) ahead of maintenance on the El Paso Natural Gas (EPNG) system. EPNG is curtailing 735 MMcf/d of capacity for repairs on the North Mainline from March 18-21. Waha prices remained negative at -$0.10 in trading Monday.

Waha prices have been trending lower since late February, during a period when Henry Hub has generally been rising and frequently traded over $4/MMBtu. As a result, Waha basis has been steadily weakening to under -$4 in March (see figure).

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a light 2 Bcf storage withdrawal for the week ending March 14, reflecting mild temperatures in many regions. A 2 Bcf draw would shave 29 Bcf off the 5-year storage deficit and move it down to 201 Bcf. The storage deficit vs last year would grow by 7 Bcf to 635 Bcf.

Early projections for the next two weeks could net a 14 Bcf injection into storage to end March, an earlier start to injection season than previously anticipated. This would put end-March inventory at around 1,710 Bcf, slightly higher than East Daley’s outlook in the Macro Supply & Demand Report.

Henry Hub spot prices have traded down this week, about $0.15 lower W-o-W. The prompt month has chopped sideways since last Friday (March 14) and sits just above $4.05/MMBtu. East Daley projects prices will rise this summer based on higher power and LNG feedgas demand. In the Macro Report, we forecast prices to average $4.38 in the summer and to peak in August at $4.59.

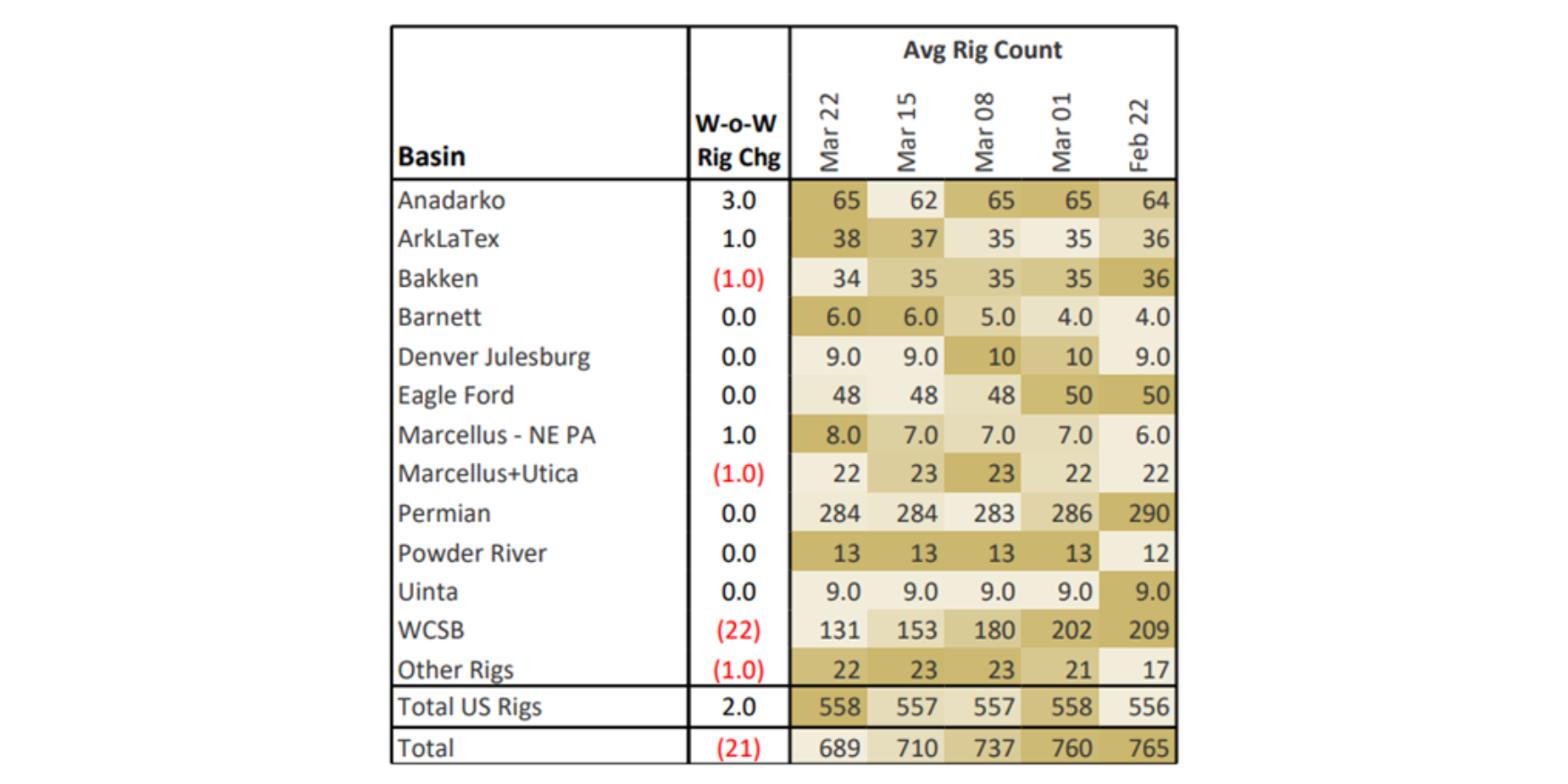

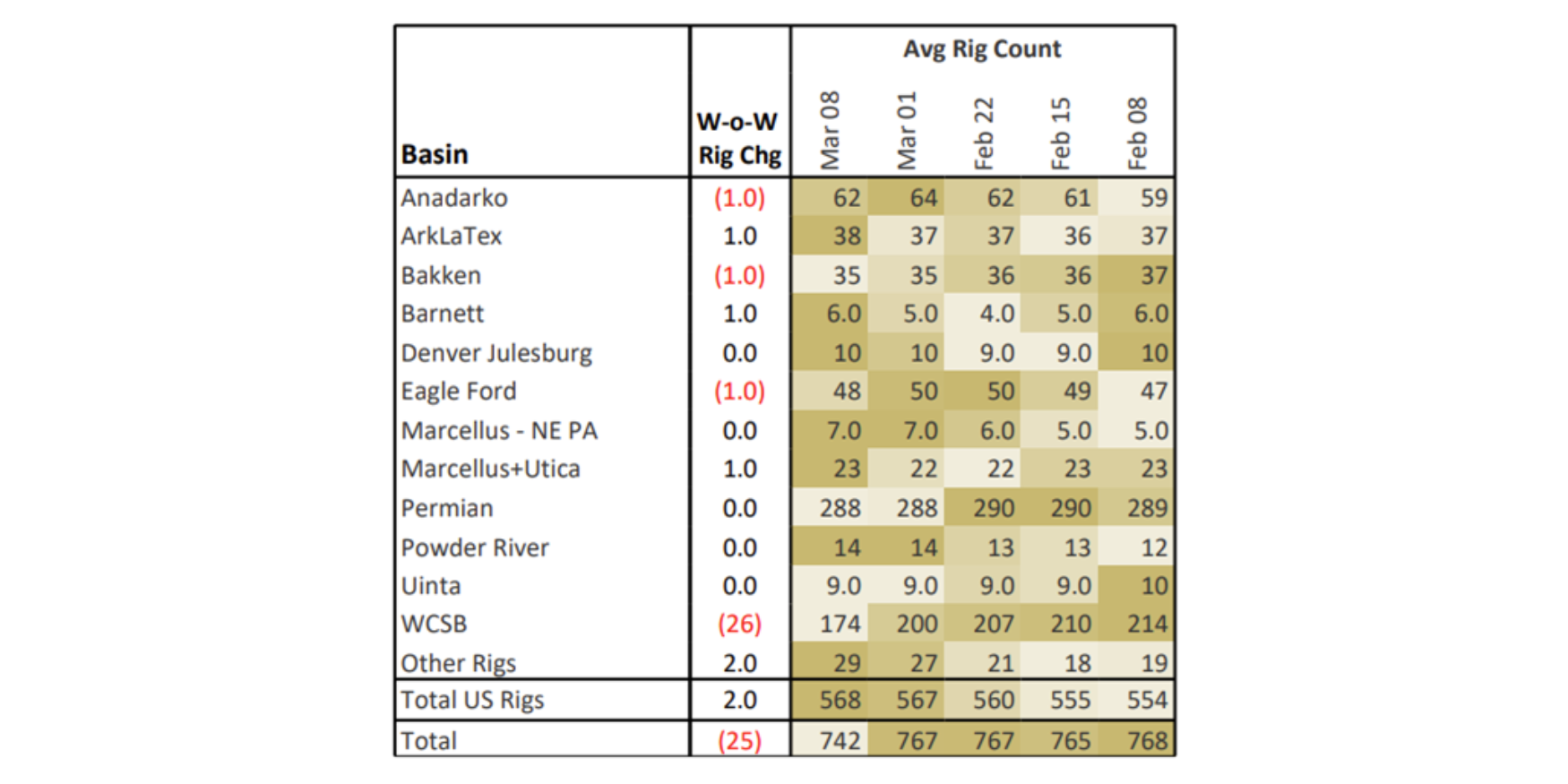

Rigs – The US rig count increased by 2 for the March 8 week, standing at 568. Basins losing rigs include the Anadarko (-1), Bakken (-1) and Eagle Ford (-1). The ArkLaTex, Barnett and Marcellus + Utica each added 1 rig on the week. The Permian count held flat at 288, recovering from the large drop the prior week due to rig moves.

On the midstream side, Targa Resources (TRGP) is up 3 rigs net with additions on its Permian and Bakken systems. Phillips 66 (PSX) is down 3 rigs on its Anadarko, DJ and Eagle Ford systems.

East Daley’s weekly Rig Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Rig Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.