Infrastructure – The new Trump administration has lifted a moratorium on new LNG export licenses set by former President Biden as part of a broader order seeking to expand U.S. energy production.

President Trump issued the executive order on Monday (January 20) directing the Department of Energy (DOE) to resume processing export permit applications for new LNG projects. The order requests that the Secretary of Energy restart the reviews “as expeditiously as possible,†and that the DOE consider the economic, employment and security impacts to allies when evaluating the applications.

East Daley recently raised our LNG export forecast in the Macro Supply and Demand Report to reflect the more supportive regulatory environment under the Trump administration. In our updated Base case, we forecast total demand for LNG exports reaches 29.2 Bcf/d by late 2030 (see the purple line in the graph). In a Conservative case, LNG feedgas demand reaches 25.7 Bcf/d (see dark blue line).

A long project list awaits DOE review including Venture Global’s CP2 project, Kimmeridge-backed Commonwealth LNG, New Fortress Energy’s (NFE) Louisiana FLNG, Energy Transfer’s (ET) Lake Charles LNG, and Cheniere’s Sabine Pass Expansion, among others. Most of these are still short of the long-term contracts required to reach a final investment decision (FID), but the new order could help jumpstart commercial talks.

Flows – Total pipeline deliveries to US LNG facility reached a new all-time high of 15.49 Bcf/d on January 11 as commissioning work continues at the Plaquemines LNG and Corpus Christi Stage 3 expansions.

Total deliveries to LNG plants have consistently topped 14 Bcf/d since mid-December, when Venture Global began making LNG at the Plaquemines project in southeastern Louisiana. Cheniere also announced first LNG production from the Stage 3 expansion in early January.

Satellite imagery shows construction at both of the Plaquemines and Corpus Christi sites is moving along. Heat signatures are visible at both facilities, indicating that commissioning activity is underway.

Flows to Plaquemines LNG have been particularly impressive, jumping to 1.2 Bcf/d last Wednesday (Jan 15). The facility has been steadily ramping up receipts since early December as it moves through the commissioning process.

Flows –US flow samples averaged 67.9 Bcf/d for the January 19 week, up 1% W-o-W but still well below production levels in December.

The latest Arctic front pushed south over the weekend and has reduced pipeline samples by ~15 Bcf over the latest four days (January 18-22) compared to Dec ’24 monthly averages. Grossing up our interstate samples, East Daley estimates nearly 20 Bcf of lost dry gas production.

The powerful front brought snowstorms as far south as Louisiana and the Florida panhandle. While the worst of the weather is behind us, we expect lingering curtailments through the end of January as the snow melts, temperatures warm and operations resume.

The basins most affected in our latest samples include the Anadarko, Appalachia, Permian and Rockies. The Haynesville and Barnett have seemingly been able to avoid freeze-offs, with pipeline sample for each region increasing by ~5%.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a 242 Bcf withdrawal from storage for the week ending January 17. A 242 Bcf withdrawal would exceed the 5-year average by 75 Bcf and cut the surplus to a mere 2 Bcf. Storage inventory vs last year would remain in deficit territory at 76 Bcf.

In the latest Macro Supply & Demand Report, EDA forecasts at total of 845 Bcf will be withdrawn from storage in January ’25, leaving inventories at 2,545 Bcf. This is a 37 Bcf surplus vs the 5-year average, but we expect the weekly balance to toggle in neutral surplus/deficit territory for the next several weeks.

Storage will move into more permanent deficit territory starting in February and could fall up to 200 Bcf behind the 5-year average by the end of March. Wellhead freeze-offs and strong demand will impact the next two weekly EIA surveys, and could potentially disclose larger withdrawals than anticipated by the market.

On Tuesday (January 21), ERCOT power demand rose to over 70 GW as a cold front pushed south, which suggests serious gas demand in Texas and across the Southeast. Henry Hub prices jumped to over $10/MMBtu ahead of the holiday weekend but have since settled down below $4. While this storm had Uri-like traits, it appears that utility providers and producers alike were well prepared to keep the lights on and gas flowing.

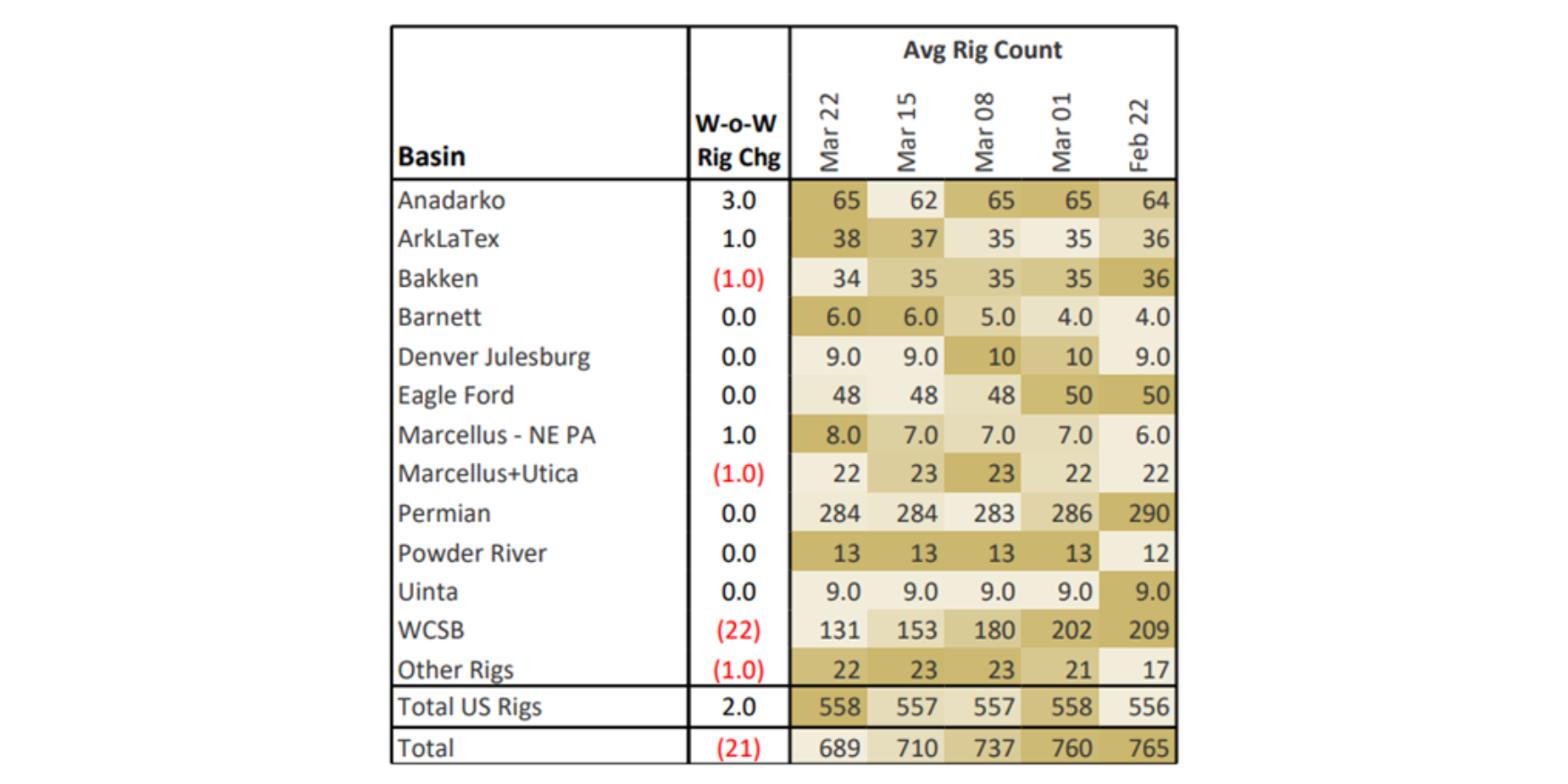

Rigs – The US rig count decreased by 10 for the January 11 week, standing at 516. The Permian (-4), Anadarko (-2), Eagle Ford (-2), Bakken (-2) and Marcellus + Utica (-1) lost rigs while the ArkLaTex (+1) and DJ (+1) added rigs on the week. The large drop in the Permian is most likely due to rig moves and should recover next week.

On the midstream side, Targa Resources (TRGP) is up 7 rigs net with additions on all its Permian systems as well as TRGP’s Eagle Ford system. Enterprise Products (EPD) lost 4 rigs total on its Permian, Eagle Ford and ArkLaTex systems.

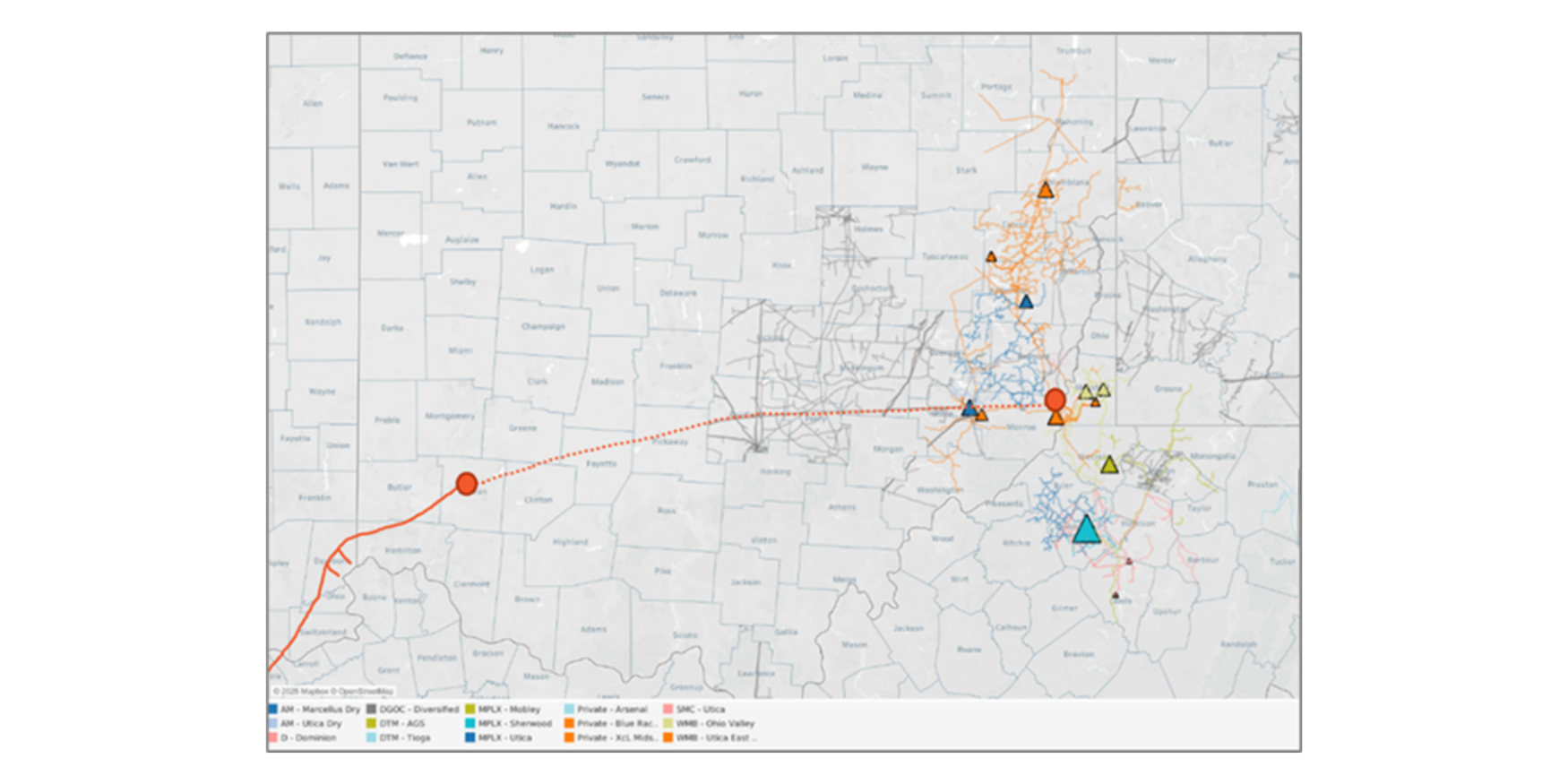

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.