Infrastructure – XPLR Infrastructure (XIFR; formerly NextEra Energy Partners) continues to seek buyers for its investment in Meade Pipeline Co., the owner of a piece of one of the most valuable US gas pipelines. XPLR expects to close the sale by 4Q25, management said in its latest earnings materials.

Meade Pipeline controls a 58.8% interest in the Central Penn Line North and a 29.4% interest in Central Penn Line South on Williams’ (WMB) Transcontinental Gas Pipe Line (Transco). XPLR acquired Meade in 2019 for a total of ~$1.37B. The company in 2023 announced plans to focus on renewables and divest its portfolio of gas pipelines, including the Meade assets.

Transco operates the pipeline as part of the Atlantic Sunrise project, leasing all of Meade’s capacity for a monthly $7.96MM fee over 20 years. The ownership and lease agreement was signed in February 2014, extending the 20-year term to 2034.

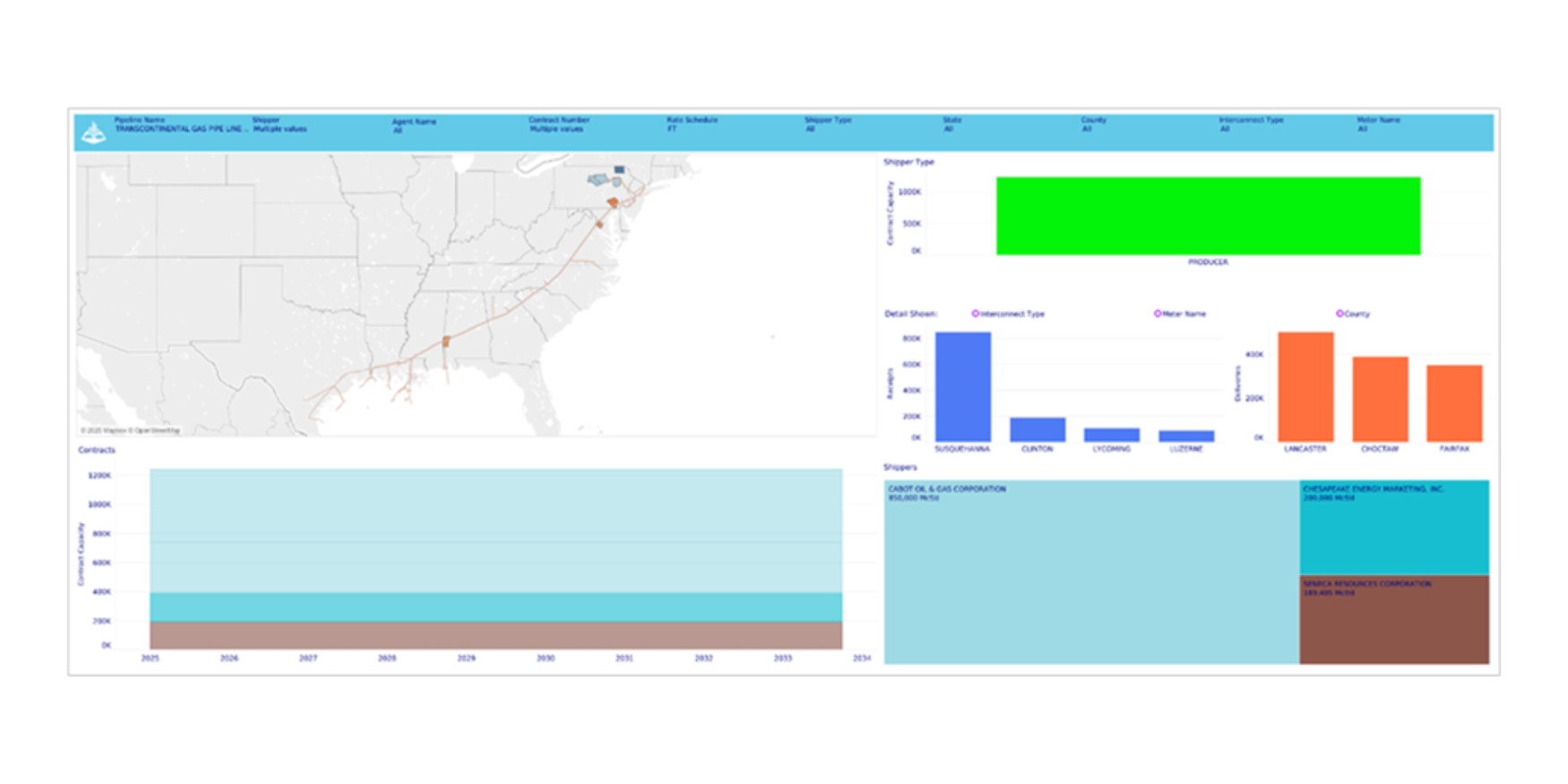

East Daley clients can review contract and financial data for Meade Pipeline in the Gas Pipeline Customer Contracts dashboard in Energy Data Studio, shown in the figure. Our Consulting Services can also create custom asset profiles using our leading energy data.

The Atlantic Sunrise facilities generated ~$430MM in revenue and ~$303MM in EBITDA in 2023, according to Form 2 disclosures filed with the Federal Energy Regulatory Commission (FERC). Based on the spending disclosed to FERC, the project was completed at a ~6.6x build multiple.

The largest counterparties backing the project include Cabot Oil & Gas (now Coterra Energy (CTRA)), Chief Oil & Gas (now Expand Energy (EXE)), and Seneca Resources. The shippers all signed 20-year contracts that will expire in October 2033. These producers should prove stable recontacting parties as they look to maintain dry gas production in northeast Pennsylvania. Current flows through the Central Penn Line indicate that the pipeline is highly utilized.

Due to its unique access to Atlantic Coast markets, EDA appraises the whole of Transco at a 13-15x multiple. It is one of the most profitable gas pipelines in the US, generating net income of over $1B in 2023. Although the Central Penn Line is just one segment of the asset, its location in the premium Northeast market and its connectivity to the broader system enhances the value.

Reach out to EDA’s Consulting Services for a deeper look at Meade Pipeline. Private equity players are likely to pursue a unique opportunity for an equity interest, or it could be an opportunity for Williams to expand ownership of a line already part of its flagship asset.

Infrastructure – On Monday (April 28), Woodside Energy made a final investment decision (FID) to develop the 16.5 mtpa (~2.5 Bcf/d feedgas equivalent) Louisiana LNG facility in Calcasieu Parish. The $17.5B commitment is unusual as, unlike past LNG project FIDs, Louisiana LNG only has ~8% of its capacity contracted under binding supply and purchase agreements (SPA). However, Stonepeak recently invested $5.7B in the project, covering 75% of 2026 and 2027 capital expenditures.

The three-train facility is expected to produce first LNG in 2029 and has capacity to add two more trains, which would bring total potential demand to over 4 Bcf/d. Woodside is in discussions with potential partners to reduce the company’s current $11.8B share of capital exposure, including selling an interest in the $1.1B Line 200 header.

The 3+ Bcf/d Line 200 pipeline would extend 37 miles from Lake Charles to the Gillis hub, interconnecting with up to 11 pipelines. Woodside also acquired the proposed Driftwood Mainline (4 Bcf/d) and Line 300 from Tellurian, projects that would provide ample optionality in a crowded Gillis market.

With this latest FID, East Daley estimates 12.7 Bcf/d of incremental LNG feedgas demand by YE30. There are also several more projects aiming to make FID later this year. CP2 (3+ Bcf/d) and Commonwealth LNG (~1.26 Bcf/d) both received their DOE non-FTA export licenses earlier this year under the friendlier-to-LNG Trump regime. Energy Transfer (ET) also expects to make FID on Lake Charles LNG (~2.5 Bcf/d) during 4Q25, management said on the company’s 4Q24 earnings call.

ET has made good headway recently advancing its LNG project. Lake Charles LNG signed an SPA with Chevron (CVX) late last year, and CVX is working to recruit other customers. ET also signed a Heads of Agreement with MidOcean Energy, a subsidiary of EIG Global Energy Partners, to jointly develop the Lake Charles facility. Under the terms of the non-binding framework, MidOcean would commit to 30% of construction costs in return for 30% of the LNG production. Lake Charles is still waiting on its DOE non-FTA approval after the original expired, but East Daley does not expect this to be an inhibiting factor.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a 108 Bcf injection of for the week ending April 25. A 108 Bcf injection would be 50 Bcf greater than the 5-year average, flipping the delta to a 6 Bcf surplus. The storage deficit versus last year would fall by 44 Bcf to 434 Bcf.

The May futures contract settled at $3.17/MMBtu earlier this week, about $0.17 higher than the end of last week as short non-commercial positions cashed out ahead of expiry. The new June prompt-month contract also gained some ground and is trading above $3.35, about $0.40 over where cash traded earlier this week.

In this month’s edition of the Macro Supply & Demand Report, East Daley forecasts May cash will average $3.45/MMBtu as storage remains in a marginal surplus to the 5-year average.

Rigs – The US rig count decreased by 7 for the April 19 week, standing at 570. The Permian (-4), Anadarko (-2), Marcellus NE PA (-2), DJ (-1) and Marcellus + Utica (-1) lost rigs while the Bakken added a rig on the week.

On the midstream side, Energy Transfer (ET) is down 4 rigs net with losses on its Permian, Anadarko and Eagle Ford systems. Phillips 66 (PSX) is up 2 rigs total with additions on its Anadarko and Permian systems.

East Daley’s weekly Rig Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Rig Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.