Infrastructure – Energy Transfer (ET) has made a final investment decision (FID) to move forward with the $2.7 billion Warrior Pipeline, renamed by the company as the Hugh Brinson Pipeline. The decision adds to momentum for new pipeline takeaway from the Permian Basin.

ET announced the FID last Friday (December 6). The 42-inch pipeline will span 400 miles from the Waha hub to Maypearl, located south of Dallas/Fort Worth, where it will connect to other ET pipelines and storage infrastructure. The Hugh Brinson line will feed growing demand in the state and provide downstream access to the Carthage and Katy hubs.

In Phase 1, ET will also build a 36-inch lateral for 42 miles in Martin and Midland counties to connect the mainline to third-party processing plants in West Texas. Including a Phase 2 compression expansion, the Hugh Brinson Pipeline will be able to transport up to 2.2 Bcf/d.

ET executives had suggested a final decision was close on the company’s 3Q24 earnings call in early November. The company plans to start Phase 1 of the project (1.5 Bcf/d capacity) by the end of 2026.

East Daley Analytics reviewed the former Warrior Pipeline in November, and our outlook remains the same: we expect an overbuilt market after 2026 as new pipeline expansions outpace production growth. In addition to the recently started Matterhorn Express Pipeline, WhiteWater Midstream is building the 2.5 Bcf/d Blackcomb Pipeline. Kinder Morgan (KMI) also has taken FID to add compressors to the Gulf Coast Express Pipeline.

The figure compares East Daley’s latest gas production forecast in the Permian Basin Supply & Demand Report with our outlook for pipeline egress, including ET’s Hugh Brinson project. If Mexico Pacific LNG reaches FID (expected in early 2025), and thus ONEOK (OKE) moves ahead with its Saguaro pipeline, the basin will have plenty of capacity through 2030.

The shift from pipeline constraints to abundance is good news for producers and will support future production growth. However, price spreads to the Waha hub are set to compress as more capacity is added from the basin, cutting a source of profits for some marketers and midstream companies.

Infrastructure – Boardwalk Pipeline Partners has made FID on the Kosci Junction project for 1.16 Bcf/d of capacity, helping support growing demand in the Southeast.

Anchored by a 20-year agreement, the Boardwalk project will extend east from the existing Greenville Lateral on Texas Gas Transmission (TGT). The pipe would travel 80 miles to Clarke County, MS to an interconnect with Southern Natural Gas (Sonat), and an additional 18-mile segment would deliver gas into the Gulf South mainline near Destin Pipeline.

Boardwalk expects to start service on the Kosci Junction in 1H29. Gulf South is also in talks to market the remaining potential capacity, up to a total of 1.58 Bcf/d. According to CEO Scott Hallam, the project will “support the growth of data centers and industrial demand†in the Southeast.

Kosci Junction directly competes with KMI’s Mississippi Crossing project on Tennessee Gas Pipeline. As shown on the map, MSX would travel the same distance as the Greenville Lateral on TGT before turning southeast and following a similar path as the Kosci Junction. ET is also marketing its South Mississippi project across several affiliated pipelines, including Florida Gas Transmission (FGT), Tiger, Gulf Run, Trunkline, Enable MRT, and EGT. The ET project is currently scoped for 1.0 Bcf/d but is potentially expandable to 2.0 Bcf/d. However, Boardwalk may have beaten these competitors to the punch to capture new market.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a 165 Bcf storage withdrawal for the week ending December 6, according to a survey by The Desk. A 165 Bcf withdrawal would be 94 Bcf more than the 5-year average and would cut the surplus to 190 Bcf, the second trip below 200 Bcf since the week ending October 25.

EIA could potentially report a record withdrawal in this Thursday’s survey. The last time a comparable draw occurred for early December was 14 years ago, when capacity holders withdrew 164 Bcf for the week ending December 10, 2010.

For the month of December, East Daley predicts a total withdrawal of 644 Bcf in the Macro Supply & Demand Report. This week’s EIA survey is likely to account for 25% of that total. Should our December forecast pan out, the 5-year storage surplus would total about 205 Bcf. Storage would finish December about 127 Bcf less than a year ago, which is a positive sign for prices.

Henry Hub cash prices are reflecting the recent cold weather, holding above $3.00/MMBtu this week. We forecast January Henry Hub prices to run up to an average of $3.25 in the Macro Supply & Demand Report.

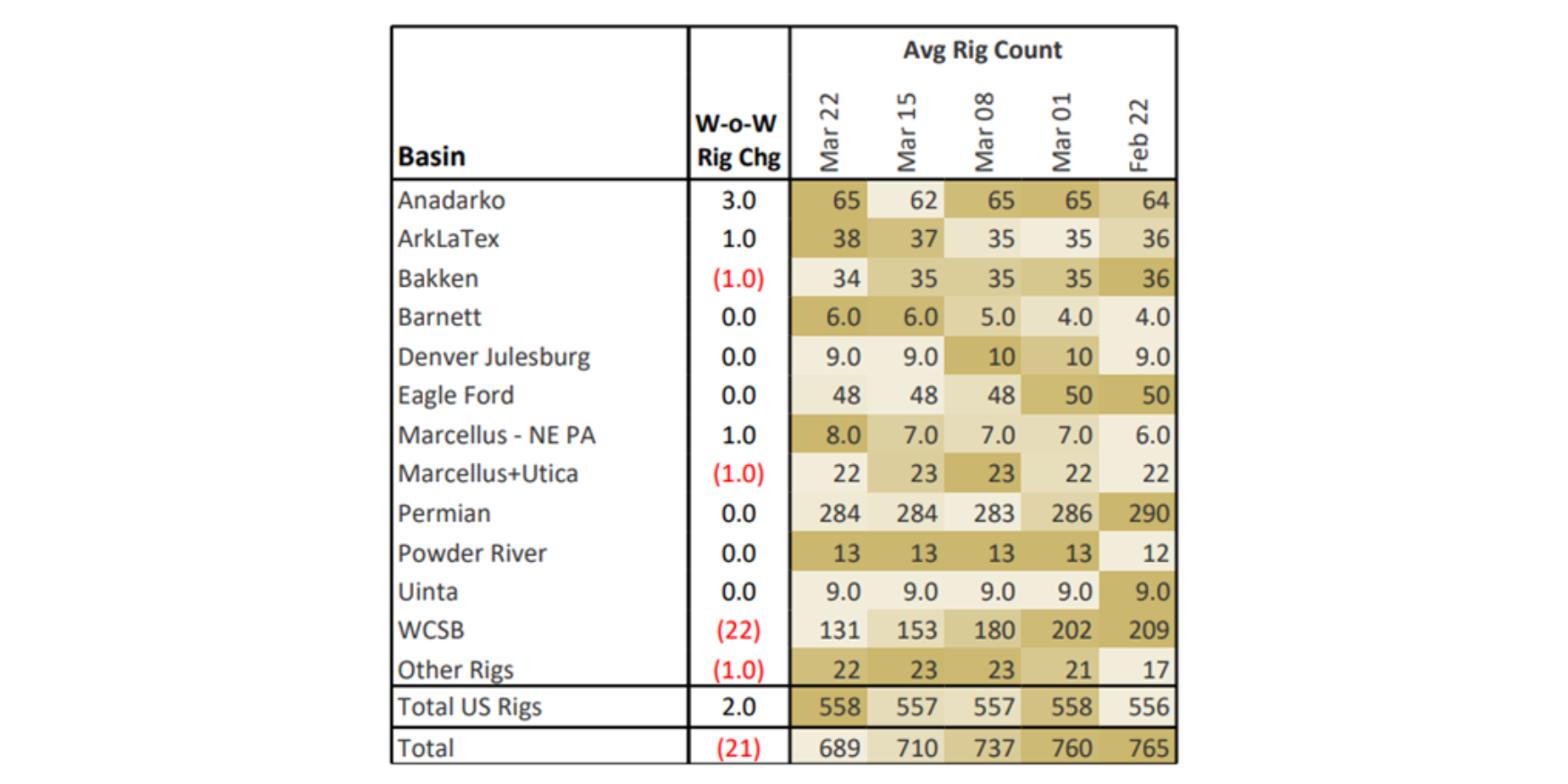

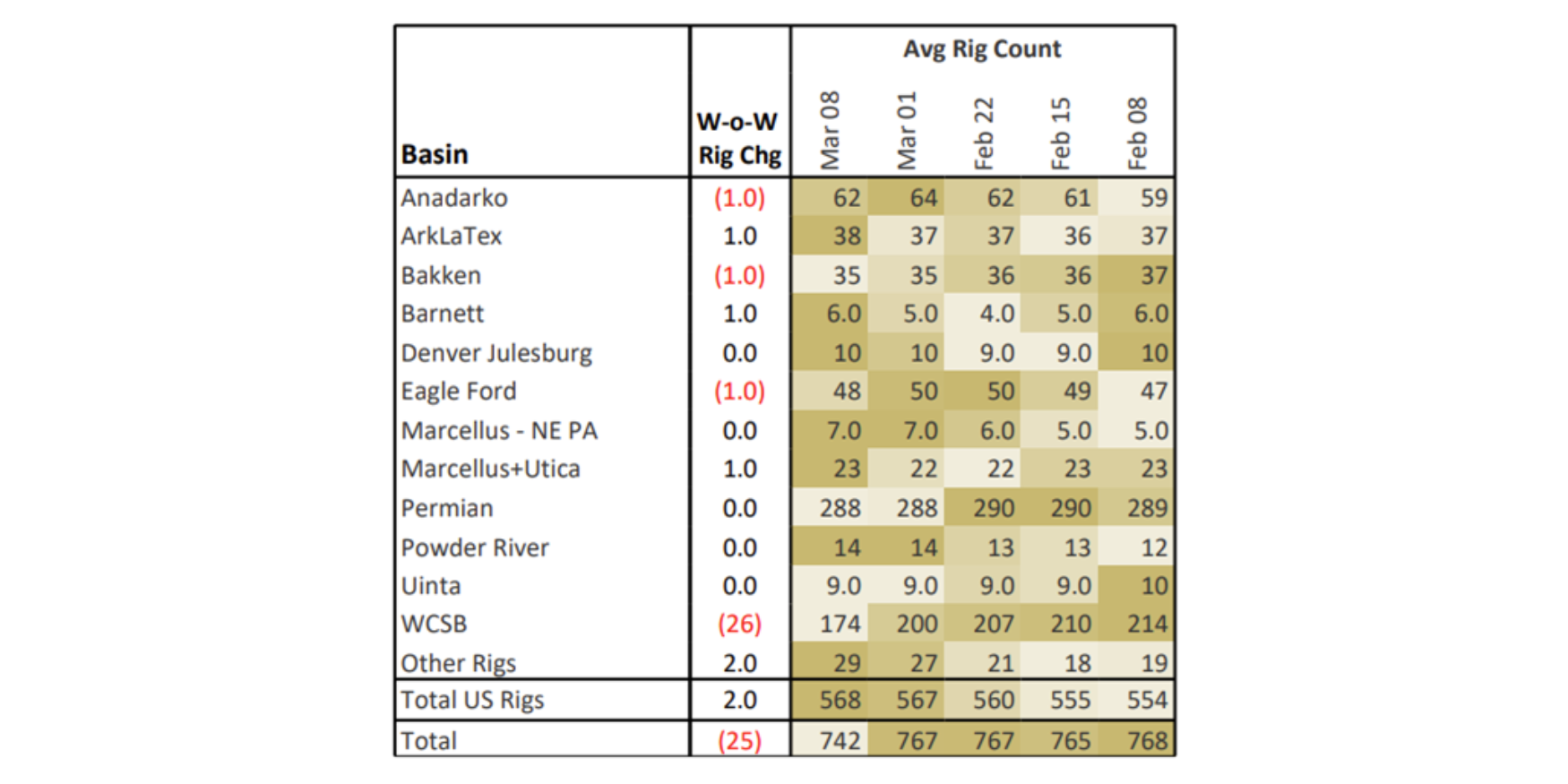

Rigs – The US rig count increased by 5 for the November 30 week, standing at 569. The Anadarko (+2), ArkLaTex (+1), Denver Julesburg (+1), and Marcellus + Utica (+1) gained rigs on the week. The Permian lost 2 rigs on the week.

On the midstream side, Targa Resources (TRGP) is down 3 rigs net with losses on its West Texas, Delaware and Versado systems. Phillips 66 (PSX) gained 4 rigs on its Eagle Ford and Permian systems

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.