Infrastructure – In December, Kinder Morgan released a preliminary maintenance schedule for January for its El Paso Natural Gas (EPNG) pipeline. Among the listed impacts was a significant reduction in flows through EPNG’s North ML segment point that would reduce operational capacity from over 2.29 Bcf/d to about 1.74 Bcf/d for most of January, a drop of nearly 25%.

January is typically a period of high demand for both the pipeline’s north and south mainlines, which carry gas westward from the Permian. These volumes account for much of the gas supply across New Mexico, Arizona, and California when cooler winter temperatures drive up demand in the west, so a significant reduction in capacity along EPNG could force price dislocations at western hubs, especially if the region sees colder-than-average temperatures.

January 2024 saw flows at EPNG’s North ML point average 1.71 Bcf/d. While this is slightly below the four-year average for January of 1.77 Bcf/d, last January also saw volumes reach 2.07 Bcf/d, well above the 1.74 Bcf/d capacity expected to be available this year. If demand were to reach similar levels again this January, western prices may need to increase above usual levels to incentivize additional volumes from other routes due to EPNG’s maintenance.

Infrastructure – After achieving first liquefaction only 12 days earlier, Venture Global’s Plaquemines LNG announced on Dec 26 that the first commissioning cargo had set sail from the Louisiana facility to deliver LNG to ENBW in Germany.

Since beginning liquefaction on Dec 12, the Gator Express Pipeline (GXP) has supplied Plaquemines with over 7.42 Bcf of gas sourced from Tennessee Gas Pipeline (TGP). While GXP also has an interconnect with Tetco, that interconnect hasn’t posted any volumes since Dec 6.

Over in Texas, Cheniere’s Corpus Christi LNG announced on Dec 30 that it had achieved the first liquefaction at Train 1 of the facility’s Stage 3 expansion project. Cheniere expects to achieve substantial completion of the train by the end of 1Q25.

Flows to US LNG facilities have broached new territory as a result of these two projects beginning liquefaction, with combined volumes topping 15.2 Bcf/d on Dec 31. This number can be expected to grow further in the coming months as commissioning at Plaquemines and Corpus Christi Stage 3 continues.

Flows – Permian sample is up W-o-W by 2% to 6.5 Bcf/d. Flows starting next week could be impacted by El Paso Pipeline maintenance which has scheduled a reduction in capacity of 669 MMcf/d on Caprock and North Mainline stations, which are key points on the basin gas egress dynamics.

Bakken flow sample has remained flat during the last two weeks of December averaging 2.4 Bcf/d, partly due to warm-to-average temperatures in North Dakota and ~36 active rigs in the basin.

The ArkLaTex sample recovered to 10.2 Bcf/d, which lines up with our latest ArkLaTex production forecast and reflects a slower production ramp in 2025.

Another source of variability for the flow sample is the expected arctic blast, which will bring record-setting cold in the second week of January 2025. Temperatures will dip east of the Rocky Mountains and the Northeast will see a higher likelihood of snowfall.

Storage – Following a 93 Bcf withdrawal in last week’s report, traders and analysts expect the Energy Information Administration (EIA) to report a 140 Bcf draw for the week ending December 27. A 140 Bcf withdrawal would be 36 Bcf more than the 5-year average and narrow the surplus to 130 Bcf.

Cold weather appears to be on the horizon with the latest forecasts expecting an unusually cold January. This forecast would be a boon to gas prices aiding in shrinking the storage surplus even further. This follows a slow start to winter with the sixth-warmest November on record, the 2024-25 winter so far has closely resembled the last heating season.

In the latest Macro Supply & Demand Report, East Daley calls for the Lower 48 to exit March at 1,924 Bcf (March 31) with normalized weather.

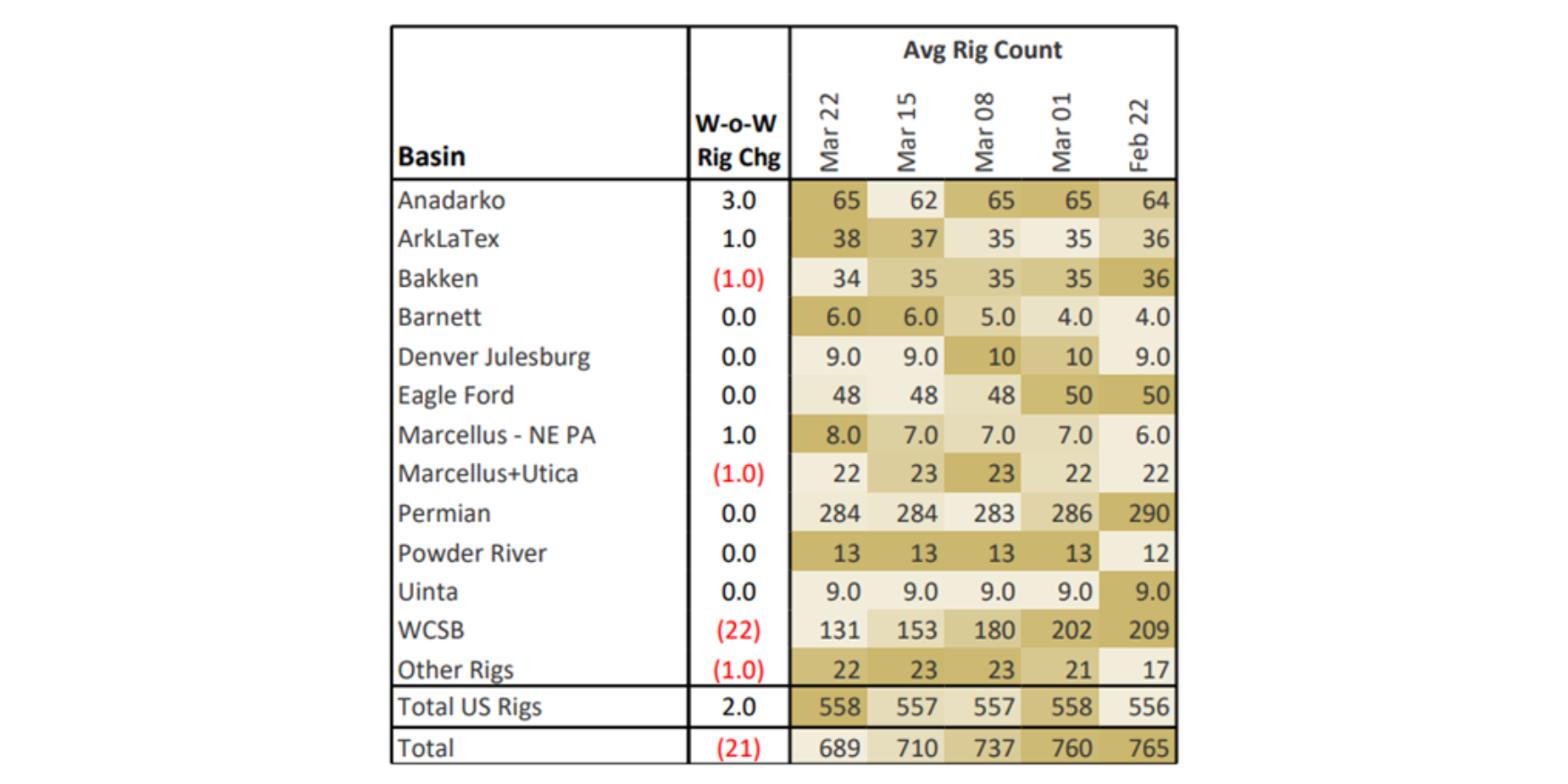

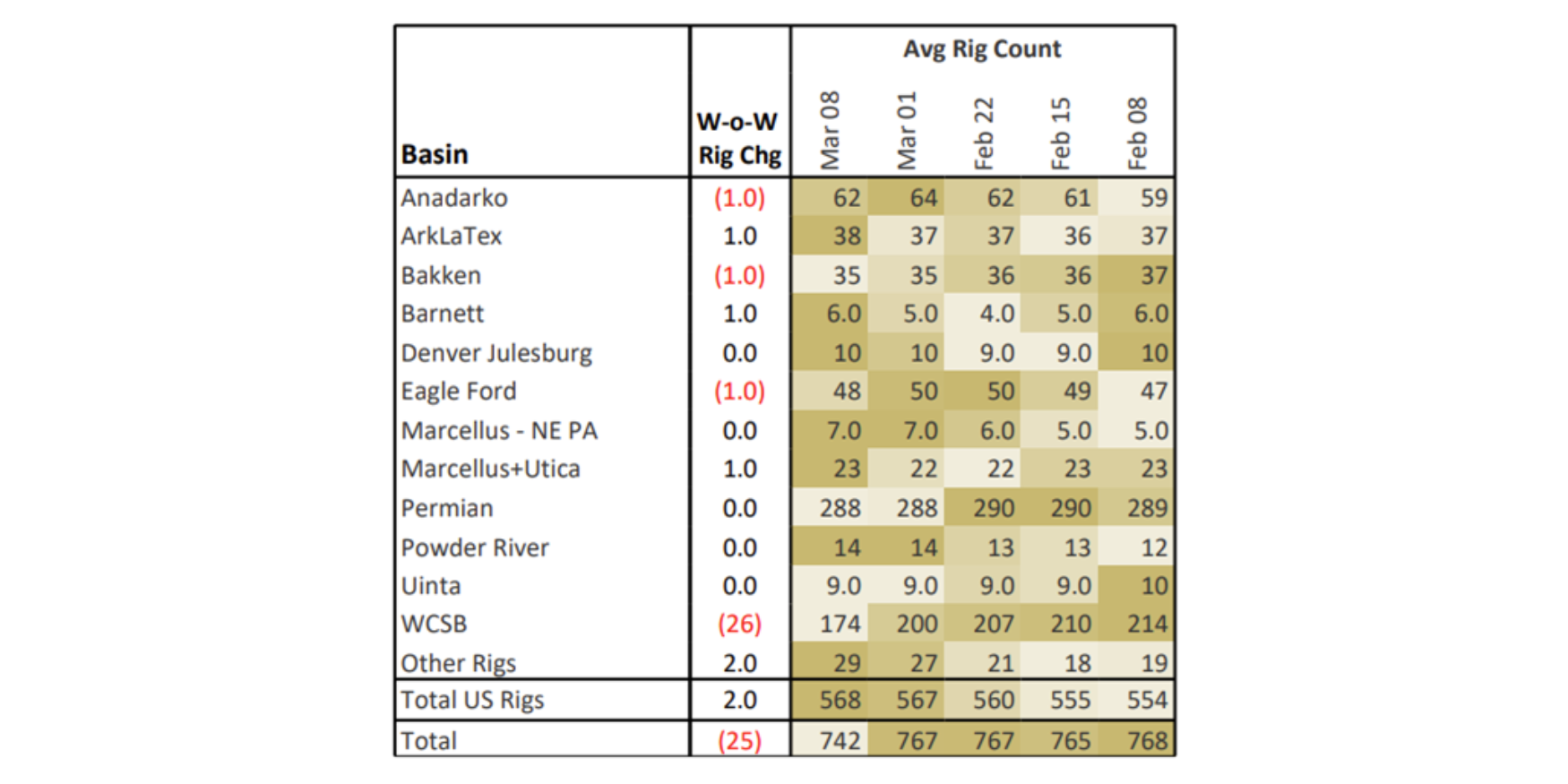

Rigs – The US rig count decreased by 7 for the December 21 week, standing at 531. The Permian (-4), ArkLaTex (-2), Anadarko (-1), and Marcellus NE PA (-1) lost rigs on the week.

On the midstream side, Targa Resources (TRGP) is down 5 rigs net with losses on its Permian, Eagle Ford, and North Texas systems. Enterprise Product Partners (EPD) gained 3 rigs total on its Eagle Ford and Permian systems.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.