Natural Gas Weekly: November 30, 2023

Flows – Permian Basin gas samples are trending at an all-time high in November 2023 as new infrastructure and strong West Coast demand lift output.

Interstate pipeline receipts from the Permian Basin have averaged 6.37 Bcf/d through November 28, a 5.5% increase vs October and the highest in historical pipeline flows dating to 2018.

Strong demand in California and the Southwest region are driving gains in the Permian sample. Westbound flows on Kinder Morgan’s (KMI) El Paso Natural Gas system are also at a record high in November. Permian flows on El Paso have averaged 2.47 Bcf/d so far in November, up 10% vs the previous 4-month average. These increased flows are helping keep Southern California border prices in check as the heating season begins. A year ago, westbound flows on the El Paso system were nearly 30% lower due to the Line 2000 outage from the Permian. SoCal border prices jumped to over $40 last winter when the supply restrictions combined with below-normal temperatures on the West Coast (see figure).

In the Permian Basin Supply and Demand Forecast, East Daley forecasts Permian residue gas production to exit 2023 at 17.4 Bcf/d, a Y-o-Y increase of 2.3 Bcf/d. New natural gas processing and pipeline expansions have supported higher supply. Whistler Pipeline completed a compression expansion in September, adding 0.5 Bcf/d of takeaway to the Gulf Coast. Also on the horizon is a 0.5 Bcf/d expansion of KMI’s Permian Highway Pipeline. That project is expected to begin operations in the first week of December.

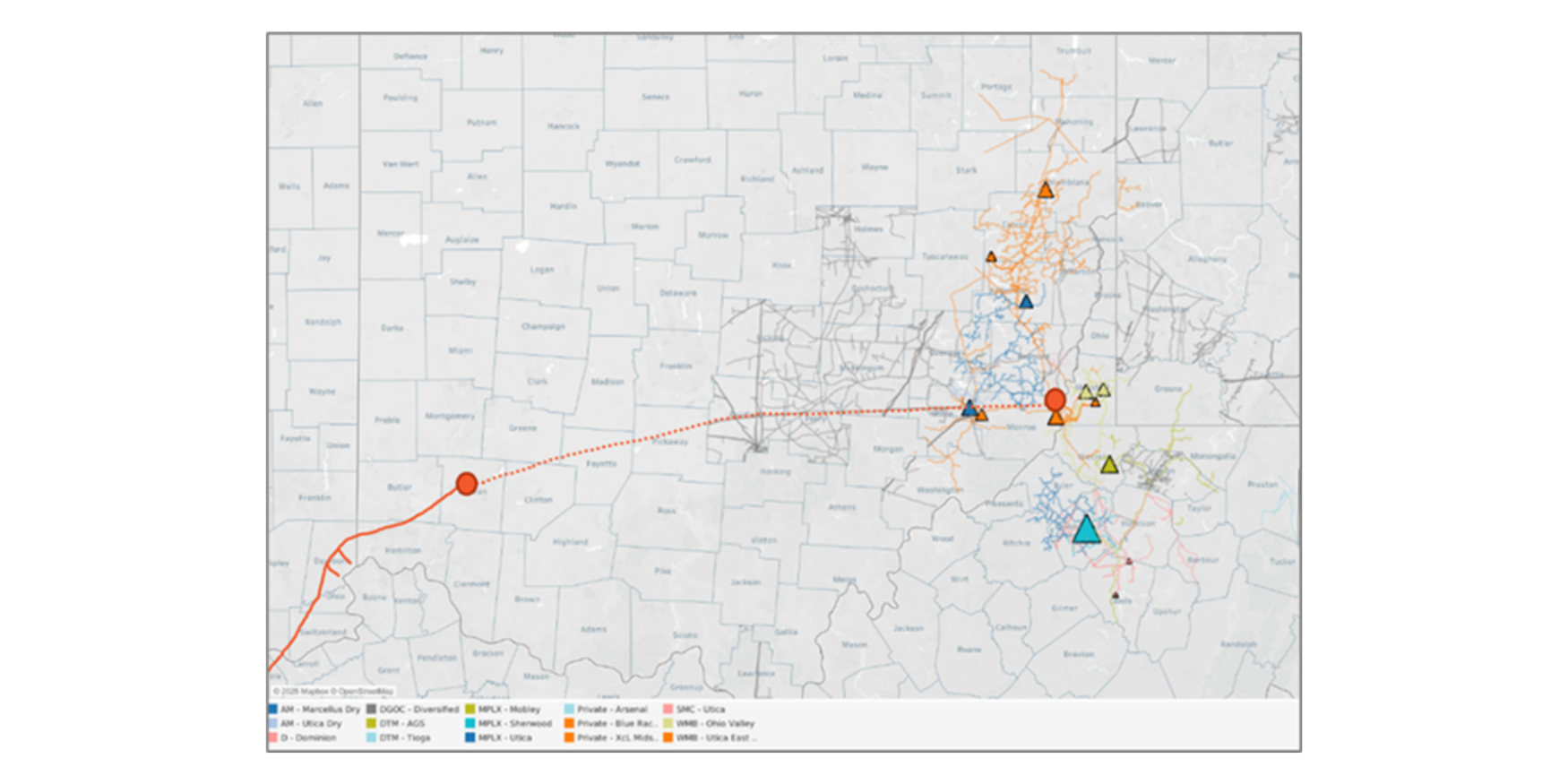

Flows – East Daley breaks out the ArkLaTex Basin covering Haynesville shale development into two geographic regions: the Louisiana Haynesville, and East Texas.

In the ArkLaTex Supply and Demand Forecast, EDA has been calling for basin production to decline since July, based on falling drilling activity. Rig counts on the Louisiana side of the Haynesville have fallen by over 50% in 2023, from 50 rigs last December to just 24 in November ‘23. East Texas rigs have been more resilient, increasing to 39 in May before falling to a low of 29 in October.

Pipeline samples in the ArkLaTex Basin averaged 13.15 Bcf/d in November ‘23, up ~211 MMcf/d over October and the highest volumes we’ve seen since the sample peaked in May ‘23 at 13.7 Bcf/d. However, if we dig deeper, we see that all of this M-o-M growth is coming out of East Texas (see figure).

Our latest ArkLaTex Supply and Demand Forecast expects wellhead production to fall to 17.4 Bcf/d by March ‘24 from a recent peak of 18.2 Bcf/d in May ‘23. Rig counts in the ArkLaTex averaged 54 in November, down from 75 rigs at the start of the year. We model production to continue declining through March ‘24, with significant rig adds starting in January ‘24 in anticipation of stronger gas prices next year.

Based on the rig trends shown above, we are forecasting a larger decline in the Louisiana Haynesville, with production bottoming out as late as June ’24. However, these declines are partially offset by growth in East Texas.

Leading Haynesville producers are guiding to a similar outlook. On the company’s 3Q23 earnings call, Southwestern Energy (SWN) executives said they expect overall Haynesville production to decline “at least into early next year,†and that “strip prices are not yet high enough to incentivize production growth.â€

Chesapeake Energy (CHK) guided to a steady drilling program of 5 rigs in the Haynesville, with the option to add a rig in the back half of 2024 if prices improve from new LNG demand. Management also noted that Haynesville production will be lower in 2024 compared to 2022 and the beginning of 2023, when production was running into midstream constraints. Those constraints have mostly been alleviated through additional interconnects between gathering systems and treating capacity expansion.

Comstock Resources (CRK), the only major public producer to operate in both Louisiana and East Texas, has also guided to a flat rig program. CRK is focused on developing its Western Haynesville acreage in East Texas, where 2 rigs are currently drilling. CRK plans to add a rig to that acreage in 2024 and another in 2025, keeping the producer’s overall basin rig count at 7. CRK expects to grow the Western Haynesville to 0.5 Bcf/d by 2025, and up to 2 Bcf/d by 2028. Regarding legacy acreage production, management says it will be hard to hold production flat with just 4 rigs. [i.e. Haynesville production should decline, even if Comstock is able to balance it with East Texas production]– Oren Pilant Tickers: CHK, CRK, SWN.

Storage – Traders expect the Energy Information Administration (EIA) to post a -6 Bcf storage withdrawal for the November 25 week, according to a survey by The Desk. Market estimates are wide for the Thursday storage report, ranging from a -35 Bcf withdrawal to a +11 Bcf injection. The wide range reflects uncertainty as a cold front moved into the Lower 48 over the Thanksgiving holidays, breaking an extended period of above-normal temperatures in most regions.

Lower 48 storage inventory currently totals 3,826 Bcf, 251 Bcf greater than last year and 249 Bcf greater than the 5-year average. Capacity holders have withdrawn an average of 44 Bcf from storage for the same week in November over the last five years, so the storage surplus is likely to expand.

In the latest November ’23 Macro Supply and Demand Forecast, East Daley forecasts storage to total 3,774 Bcf at the start of December, or 289 Bcf above the 5-year average.

EDA’s latest Macro Forecast presents an early review of the market balance for Winter 2023-24. We project storage inventory will finish the winter withdrawal season at 1,780 Bcf, about 250 Bcf above the 5-year average of 1,533 Bcf.

Rigs - US rigs decreased by 2 W-o-W to bring the total count to 594 for the November 17 week. The Permian and Eagle Ford are down 2 rigs W-o-W, and the Powder, Uinta and Marcellus NE PA each lost 1 rig. The ArkLaTex, Bakken, Barnett, and DJ basins each added 1 rig.

On the midstream side, DCP Midstream (PSX) is up 6 rigs total with additions on its Permian and DJ systems. Targa Resources (TRGP) is down 3 rigs with losses on its Permian and Eagle Ford systems. Energy Transfer (ET) gained 6 rigs on its Permian, ArkLaTex and Anadarko systems. EnLink Midstream (ENLC) is down 6 rigs with losses on its Midland and Delaware systems.