Natural Gas Weekly: June 27th, 2024

Infrastructure – Venture Global’s Plaquemines LNG will be the next LNG facility to come online, adding ~3.4 Bcf/d of new demand in the toe of the Louisiana boot. Three major pipeline expansions are coming online over the next few quarters to feed the project, while also displacing gas bound for Florida markets.

First, the Venice Lateral extension on Enbridge’s (ENB) Texas Eastern Transmission (TETCO) will add 1.26 Bcf/d of new capacity, pulling gas from Gillis on TETCO’s Louisiana mainline to feed Venture Global’s Gator Express header pipeline. The TETCO interconnect is in-service, but other than a single day of test volumes, the line is not currently flowing. At CERAweek in March, Venture Global announced that Plaquemines would start taking gas in June, with first LNG production expected this summer. East Daley forecasts Plaquemines LNG Ph1 (2.25 Bcf/d) to ramp to full capacity by 2Q25.

The next pipeline expansion to come online is Kinder Morgan’s (KMI) Evangeline Pass project on Southern Natural Gas pipeline (SNG) and Tennessee Gas Pipeline (TGP). SNG plans to add 1.1 Bcf/d of southbound capacity and lease it to TGP, receiving gas from TGP in Mississippi and redelivering that gas to TGP in southern Louisiana, after which it will flow to the Gator Express interconnect. KMI reports a tentative in-service date of November ’24. TGP also plans to feed Gator Express an additional 0.9 Bcf/d of gas from its 500 Leg.

The last major supply expansion is TC Energy’s (TRP) Columbia Gulf East Lateral Xpress Project (EXLP), consisting of 575 MMcf/d flowing east from Gillis and 150 MMcf/d flowing west from Venice, for a total of 725 MMcf/d. The estimated in-service date for ELXP is February ’25.

With eastbound flows out of Louisiana running near capacity, in route to meet power demand in Florida, and more than 3 Bcf/d of new demand in the region, East Daley expects FGT Z3 gas buyers to pay a premium starting in 2025. Transco’s Southeast Supply Enhancement project is forecasted to begin operations in 2028 (~1.6 Bcf/d, ISD 4Q27) which will help alleviate the pressure. The figure below shows EDA’s forecast for pipe flows in the southeastern Louisiana sub-region of the Southeast Gulf Forecast.

East Daley Analytics tracks Plaquemines and other Louisiana-based LNG projects in the Southeast Gulf Supply and Demand Forecast. The Southeast Gulf forecast combines our regional supply forecasts for the Haynesville and other Gulf Coast basins with midstream pipe flows/expansions and new LNG demand, for a comprehensive view of the regional gas market.

Flows – In 2Q24 the Haynesville averaged about 43 rigs, a 40% decline from 2Q23. The depressed price environment has led producers to significantly reduce rig activity. The Henry Hub spot price for 2Q24 has averaged $2.09, marking the sixth consecutive quarter at a sub $2.75 average price. The decline in drilling activity and the curtailment programs of producers have resulted in a 22% Y-o-Y decline in the pipeline sample in the Haynesville, a 16% reduction from 1Q24.

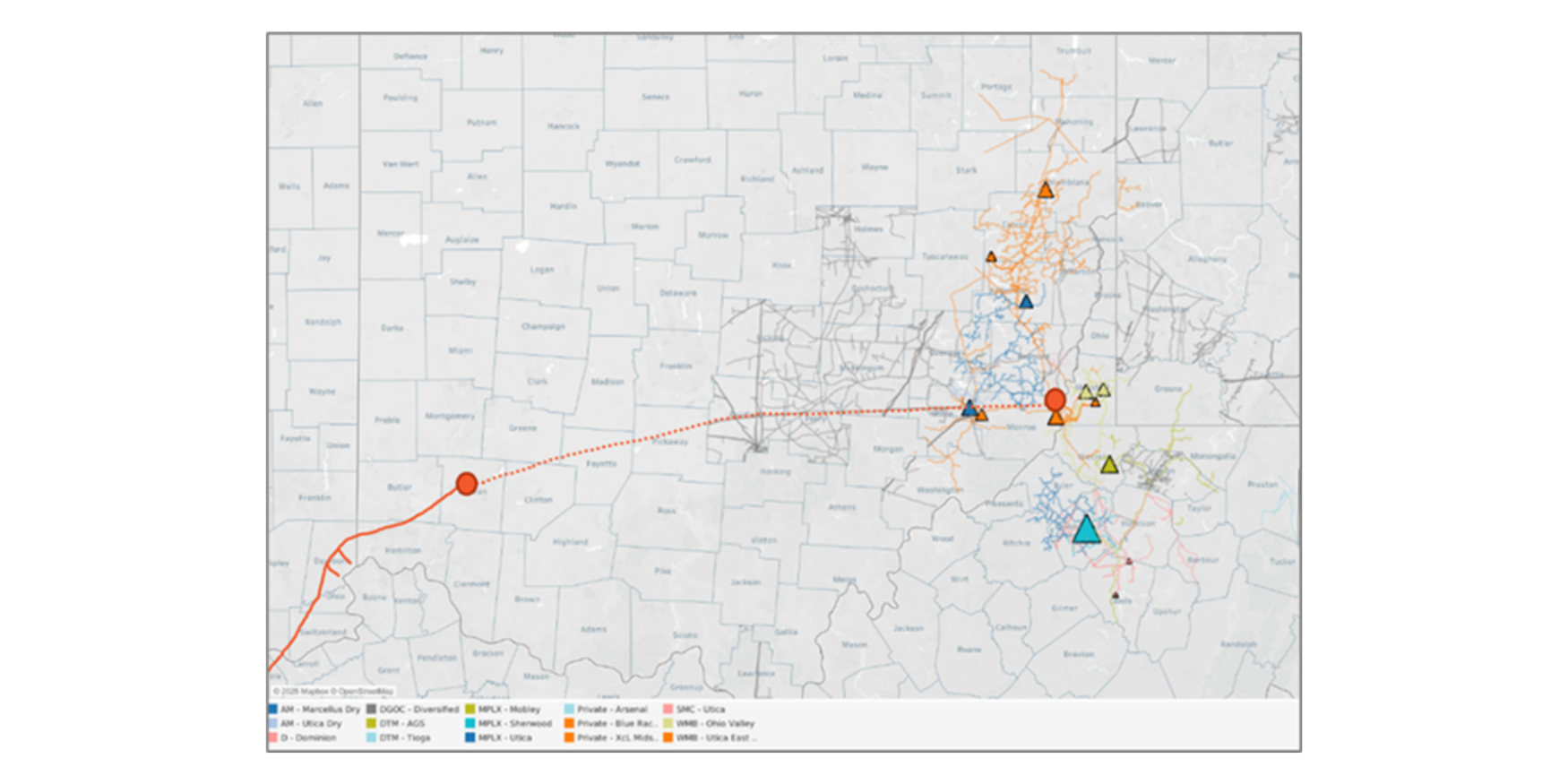

The reduction of rig activity in the Haynesville has affected gathering systems asymmetrically, creating winners and losers in the midstream space. Kinder Morgan’s (KMI) KinderHawk gathering system shows a 70% increase in pipeline sample relative to 2Q23, and a slight decline of 4% relative to 1Q24. The KinderHawk system is a standout in the basin and has been able to maintain production on the wings of strong production from BP wells.

Williams (WMB) and DT Midstream (DTM) have not fared as well as KMI in 2024. Collectively, WMB’s Louisiana-Magnolia and Trace Midstream systems have seen a 31% Y-o-Y reduction in pipeline samples. We attribute these declines to the reduction in Chesapeake drilling activity. DTM’s Blue Union gathering system has experienced a 9% Y-o-Y reduction in pipeline samples driven by a reduction of Southwestern (SWN) rigs.

Overall, the US interstate gas production sample is up about 1% W-o-W for the week of Jun 23 (+0.4 Bcf/d). In liquid-driven basins, the flow sample is relatively flat. The 4% flow drop in the Bakken is due to capacity constraints on Alliance Pipeline due to an imbalance position, which is expected to be resolved by June 30. The sample in the Permian suggests flat production in the basin despite egress capacity constraints, interstate and intrastate pipelines rerouting and producers dropping rigs in the Midland and Delaware. Until Matterhorn comes online, flow restrictions would throw a heavy discount on Waha gas price.

The flow sample in gas-focused basins is up 1% W-o-W this week. In the Arklatex (Haynesville), producers have been curtailing production for the past month due to low gas prices and delayed LNG demand until demand from Plaquemines ramps up. Recent gains in the sample W-o-W may suggest that they are turning wells back on in response to increasing demand this summer and a healthier Henry Hub cash price. In the Northeast (Marcellus+Utica) the sample has been improving since EQT resumed production last month. All in all, gas sample fluctuations across all other gas and liquids-targeted basins, as well as in the other regions were flat W-o-W.

Storage – The Energy Information Administration (EIA) is expected to report a net injection of 54 Bcf into working gas storage inventories for the week ending June 21st. For the same week last year, the EIA reported a 81 Bcf injection, or 27 Bcf higher. Last week’s net injection showed a similar delta of 25 Bcf from the prior year injection as the market remains extremely tight due to lower production levels and cooling degree day driven demand from the power sector. Inventories would rise to 3,099 Bcf, in line with our outlook in the monthly Macro S&D Report.

The surplus to the 5-year average would fall by 31 Bcf to 530 Bcf while the surplus to last year would slip to 316 Bcf. Storage injections must continue to slow down through the balance of summer as space is already hard to come by. Lower 48 inventories are at their highest level ever through the second week of June. The next highest level was reached over 12 years ago for the week ending June 15th, 2012, and was just barely over 3,000 Bcf. If storage injections do not slow down, even a five-year average pace would run through demonstrated peak capacity levels in the East, Midwest, Mountain and Pacific regions leading to operational flow orders and supply curtailments.

Rigs – U.S. rigs are down 5 W-o-W with the total count sitting at 557. The Permian is down 7 rigs while the Anadarko is down 2 rigs. The ArkLaTex, Eagle Ford, and Uinta aeach added 1 rig on the week. On the midstream side Energy Transfer (ET) is down 2 rigs total with reductions on its Permian, Eagle Ford, and Anadarko systems. MPLX LP (MPLX) is down 2 rigs total with losses on its Bakken and Marcellus + Utica systems. EnLink Midstream Partners (ENLC) is up 2 rigs total with additions on its Midland and Delaware systems.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.