Natural Gas Weekly: May 30, 2024

Flows – Leading Appalachian producer EQT appears to be restoring ~1 Bcf/d of production first shut by the operator back in February, a bearish signal for gas prices.

Pipeline samples for G&P systems that serve EQT jumped last week, up ~700 MMcf/d from levels over the last three months after EQT shut-in some production in late February (see figure). Flows remain higher earlier this week on the systems tracked by East Daley Analytics.

The timeline for the apparent return of EQT’s shut-in volumes would line up with our prediction three months ago, when we predicted EQT would restore its gas output in June ‘24. EDA’s view was based on the expected start-up of Mountain Valley Pipeline (MVP), as well as higher seasonal demand for power generation entering the summer.

Flows have increased on systems in the Southwest Pennsylvania (SW-PA) region of the Marcellus, the same systems that took a hit when EQT curtailed its production. EDA estimates the bulk of this lost production has come from Equitrans Midstream’s (ETRN) Pennsylvania gathering system.

The restart of volumes suggests a price floor over which EQT will run its wells closer to full capacity. Dominion South prices have averaged just above $1.50/MMBtu in May ’24 and DomSouth futures have traded at $1.70 for June ’24. In 2020, EQT also shut down some wells when Appalachian prices fell below $1.50.

The higher volumes also coincide with ETRN’s plan to begin flowing gas on MVP by May 22 and start tariffs by June 1, according to a request filed in April with the Federal Energy Regulatory Commission (FERC). However, MVP pushed back that timeline last week.

In a supplemental filing with FERC, MVP said that as of May 21, the pipeline is not yet mechanically completed. MVP said 99% of the new pipe has been hydrotested, but the pipeline has 10 welds remaining before the last segment can undergo hydrostatic testing. While MVP had targeted a June 1 start date, the pipeline now plans to start in “early June,†according to the filing. The delay is likely linked to a rupture MVP experienced on May 1 during hydrostatic testing.

The increased supply will likely put some pressure on natural gas prices. Nevertheless, the move makes sense for EQT. The producer is the largest capacity holder on MVP and will realize premium Zone 5 prices on the Transcontinental (Transco) system once the new 2 Bcf/d pipeline begins service.

Infrastructure – Enbridge (ENB) plans to expand the Eastern Tennessee Natural Gas (ETNG) pipeline to meet new power generation demand in the Southeast region.

ENB introduced the Tennessee Ridgeline Expansion as a secured project in its 1Q24 earnings materials. At an estimated cost of $1.1B, the project will support new demand from the Kinsgston Fossil Plant, a coal plant the Tennessee Valley Authority (TVA) is converting to use natural gas.

ETNG has filed with the Federal Energy Regulatory Commission (FERC) for a certificate to construct the project. The expansion includes 130 miles of 30-inch pipe looping, plus meter modifications and an 8 MW solar array to be installed behind the meter. The project will add 300 MMcf/d of firm capacity on ETNG to the Kinsgston plant in Morgan County, TN. ETNG is seeking approval by November 1, 2024 to begin construction in 2025 and start service by November 1, 2026.

Environmental groups including the Sierra Club and Appalachian Voices are opposing the Tennessee Ridgeline Expansion, challenging the market need in filings at FERC. The TVA has filed its own comments at FERC in support. The agency noted it has entered a final environmental impact statement and a record of decision to proceed with the Kingston plant conversion. In its letter to FERC, the TVA said the switch to gas would not be possible without the ETNG expansion.

East Daley expects to see more opportunities like the Tennessee Ridgeline Expansion for midstream companies as switching from coal to gas continues. From 2012 to 2022, coal-fired generation by utilities declined 45%, according to EIA data (see figure). Between industrial reshoring, data center demand and coal-switching, the industry has ample opportunities to grow domestic demand.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a net injection of 77 Bcf into working gas storage inventories for the week ending May 24, roughly equivalent to the EIA report for the week ending May 17 (78 Bcf). Inventories would rise to 2,788 Bcf, in line with our forecast in the monthly Macro Supply & Demand Forecast.

The surplus to the 5-year average would decrease by 27 Bcf to 579 Bcf based on market estimates, slipping under the 600 Bcf mark for the first time in 12 weeks. The last time the storage surplus was under 600 Bcf was the week ending March 1.

This would mark the sixth report out of eight in the new injection season where the reported injection has trailed the 5-year average, a bullish sign that lower production is beginning to tighten the market. June in particular should be a good test of the undersupply situation, as we expect power burn to average 39.2 Bcf/d in the Macro Forecast, similar to last June’s burn. We expect the next three EIA reports (through the week ending June 14) to continue the trend of below-normal injections.

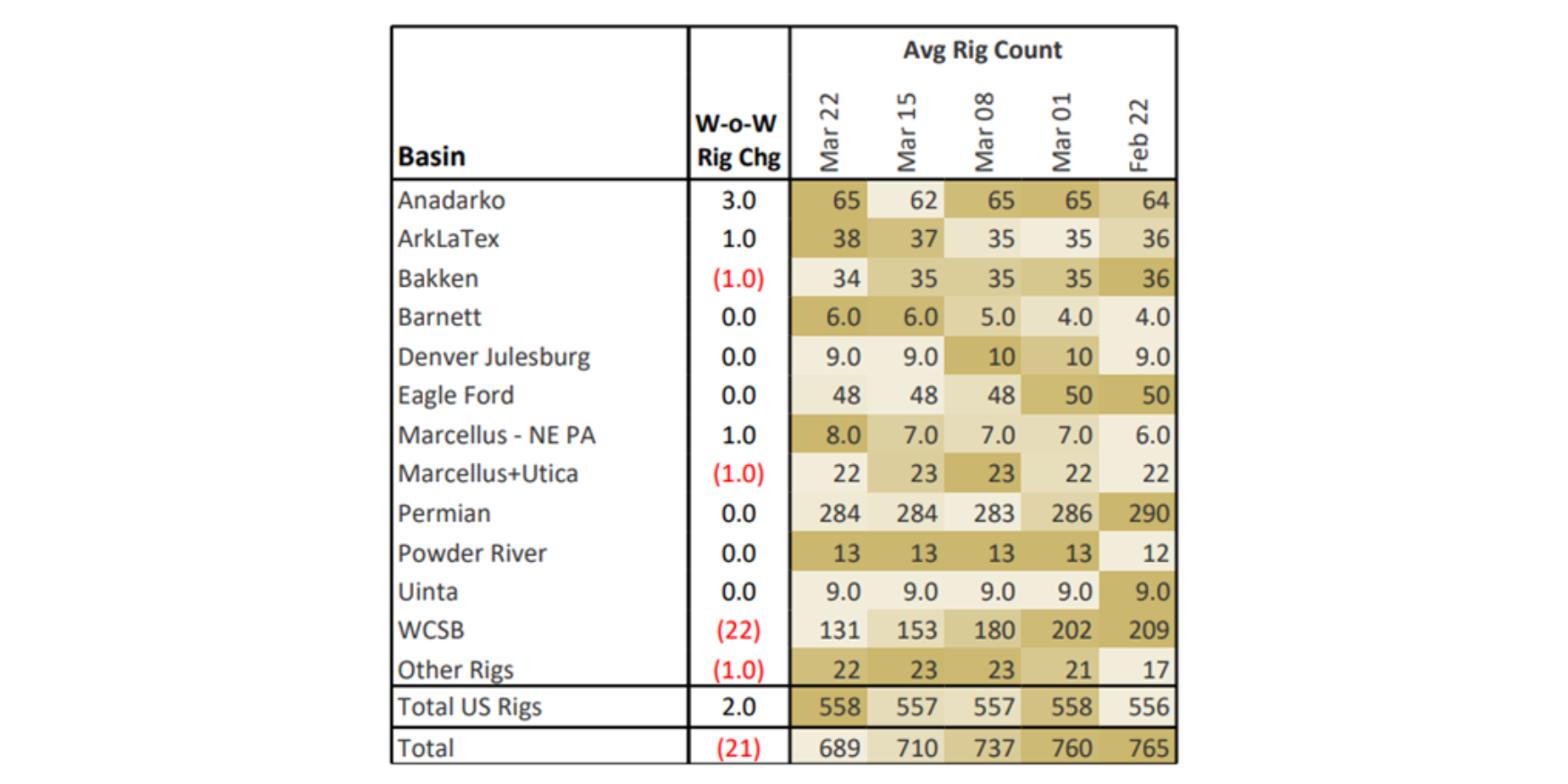

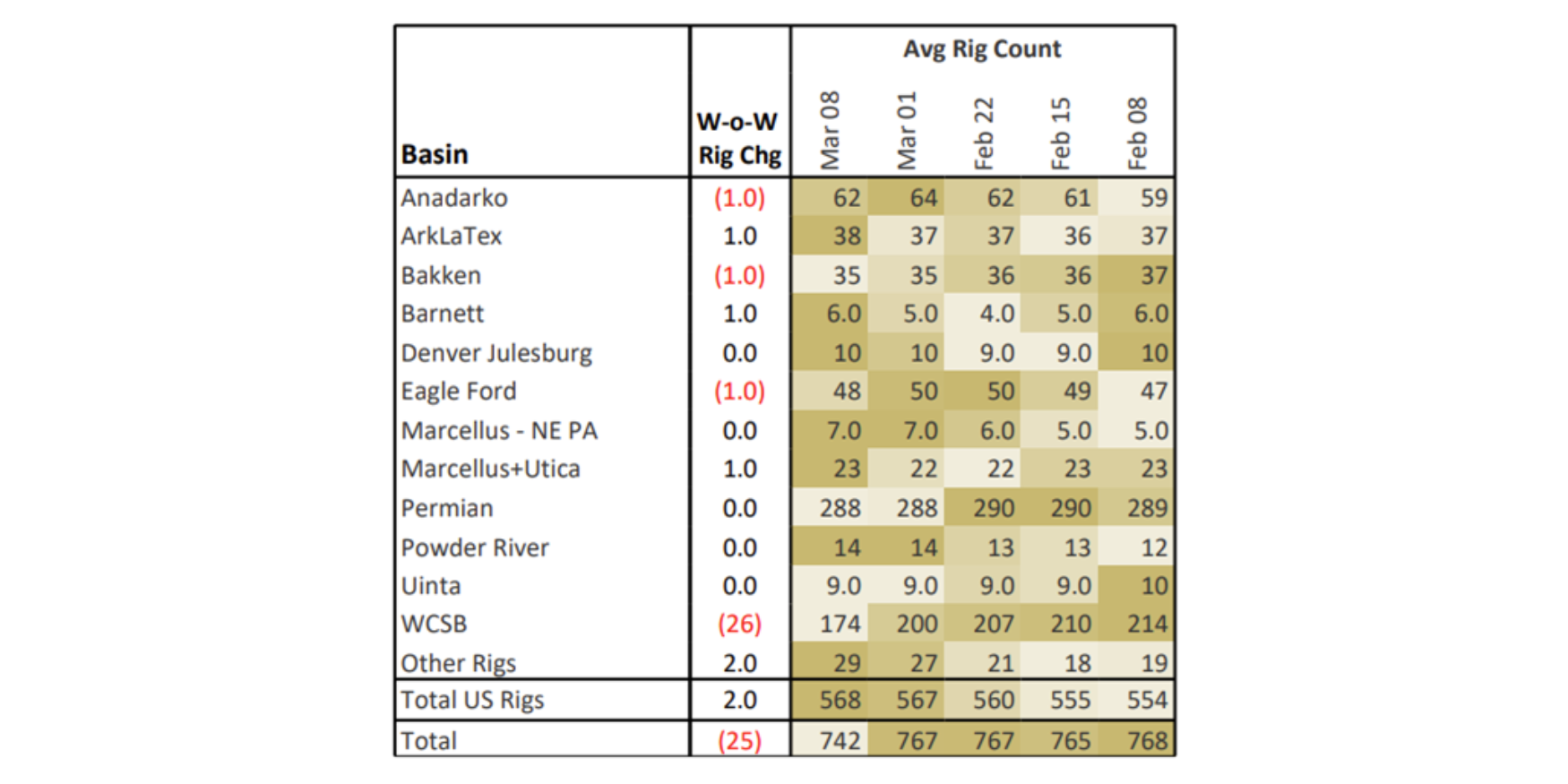

Rigs – US rigs increased by 1 W-o-W to bring the total count to 570 for the May 19 week. The Permian is down 4 rigs, while the Bakken and Powder River Basin lost 2 rigs and 1 rig, respectively. The Anadarko is up 4 rigs and the Marcellus + Utica is up 1 rig.

On the midstream side, Energy Transfer (ET) is up 4 rigs with additions on its Permian and Anadarko systems. Western Midstream (WES) lost 2 rigs on its Permian and Powder River systems.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.