Natural Gas Weekly: November 1, 2023

NOTE: East Daley Analytics is teaming up with Hart Energy on a NEW natural gas market product. Please see the important note below on the NEW Gas & Midstream Weekly newsletter.

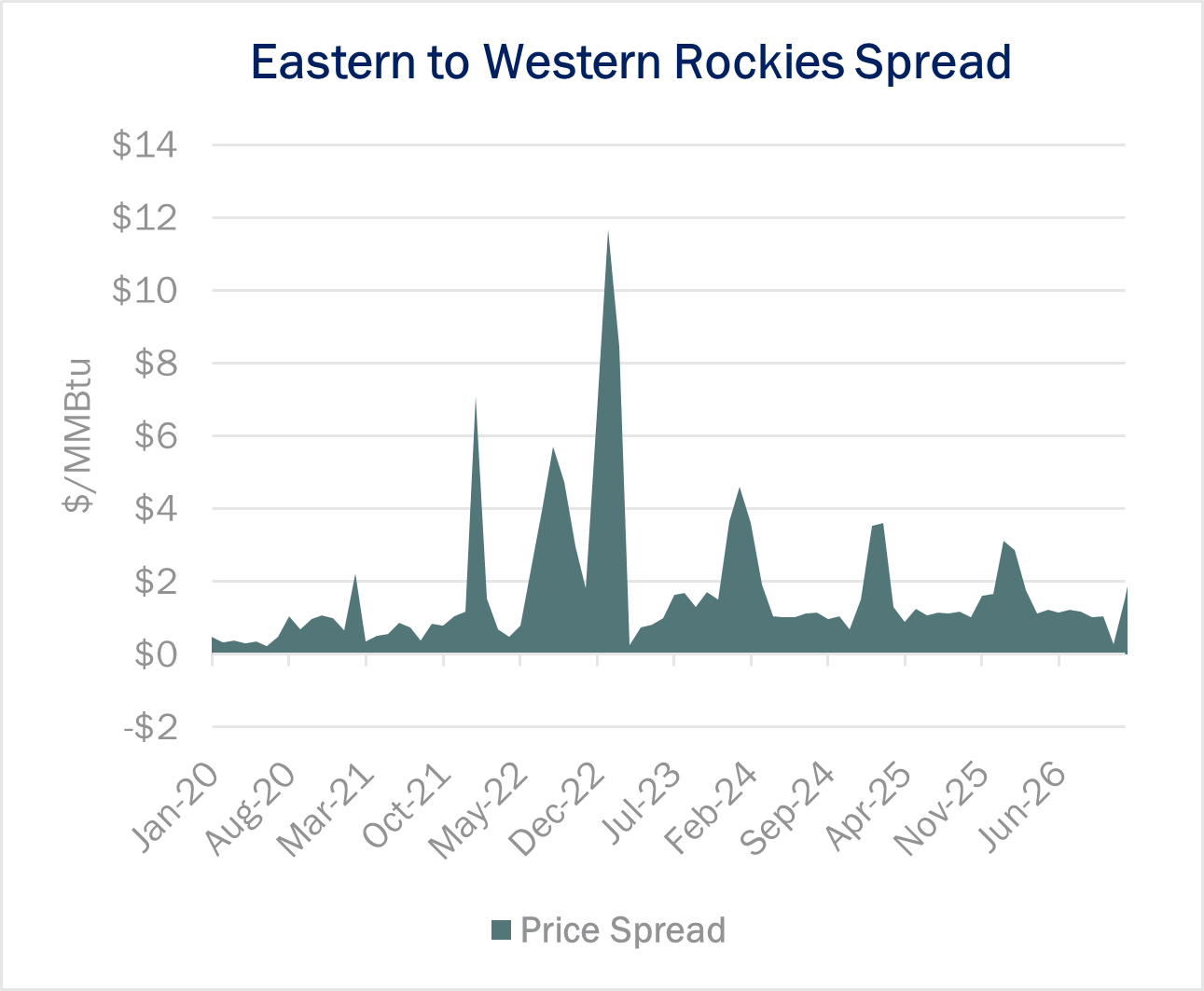

Infrastructure - An early season cold front sent natural gas prices surging this week in western US markets. The price action was particularly notable in the Rockies, where regional prices diverged as temperatures fell at the end of October.

On October 31, the spread between the Opal and Cheyenne hubs widened to $2.50/MMBtu, in what could be an early taste of volatility similar to last winter. The Opal-Cheyenne spread averaged as high as $11.67 in January 2023 as tight conditions on the West Coast pulled Opal prices higher.

On October 31, the spread between the Opal and Cheyenne hubs widened to $2.50/MMBtu, in what could be an early taste of volatility similar to last winter. The Opal-Cheyenne spread averaged as high as $11.67 in January 2023 as tight conditions on the West Coast pulled Opal prices higher.

The West Coast has been intermittently short natural gas supply for the last few years, leading to a wide spread between eastern and western Rockies prices. While there is sufficient capacity to bring gas to the Wamsutter area on pipelines like Rockies Express (REX), there is not enough capacity to move gas further west to the Opal hub in southwestern Wyoming. Opal has connectivity to the Southern California market via Kinder Morgan's (KMI) Kern River Pipeline, causing the point to trade at a premium when West Coast prices surge. The constraint should be loosened in 2026 when Williams (WMB) plans to complete a 325 MMcf/d expansion of Overthrust Pipeline.

East Daley is monitoring western gas markets through our West Coast Supply and Demand Forecast. Launching next month, this new report provides an in-depth view into supply, demand and flow dynamics affecting prices in the West. Reach out for more information on the West Coast Supply and Demand Forecast.

Flows - Pipeline samples in the Williston Basin have moved lower amid below-normal temperatures. Samples have declined by 8% (192 MMcf/d) since October 26 vs the first three weeks of October.

East Daley predicted Bakken production could be impacted by the start of seasonal freeze-offs. Temperatures in the upper Midwest fell up to 17° Fahrenheit below normal as a cold front moved through at the end of October.

East Daley predicted Bakken production could be impacted by the start of seasonal freeze-offs. Temperatures in the upper Midwest fell up to 17° Fahrenheit below normal as a cold front moved through at the end of October.

Currently, the flow sample from the Williston Basin is 2.3 Bcf/d vs an average of 2.5 Bcf/d in the first three weeks of October. We expect production to remain lower until temperatures rise back into the 20s-30s, which is not expected until November 5–9 in the latest National Weather Service 6- to 10-day forecast.

Winter freeze-off events are relatively common in the Bakken and in Rocky Mountain basins. As the mercury drops, produced water can freeze in the wellbore and block the flow of hydrocarbons. East Daley tracks supply impacts from freeze-off events in the Bakken Supply and Demand Forecast and the Bakken Supply and Demand Forecast.

Reduced flows from the Bakken have led to higher inbound supply from Western Canada into the Midwest. Receipts from Canada have increased on the Alliance (+37 MMcf/d) and Northern Border (+116 MMcf/d) pipelines to compensate for lower production.

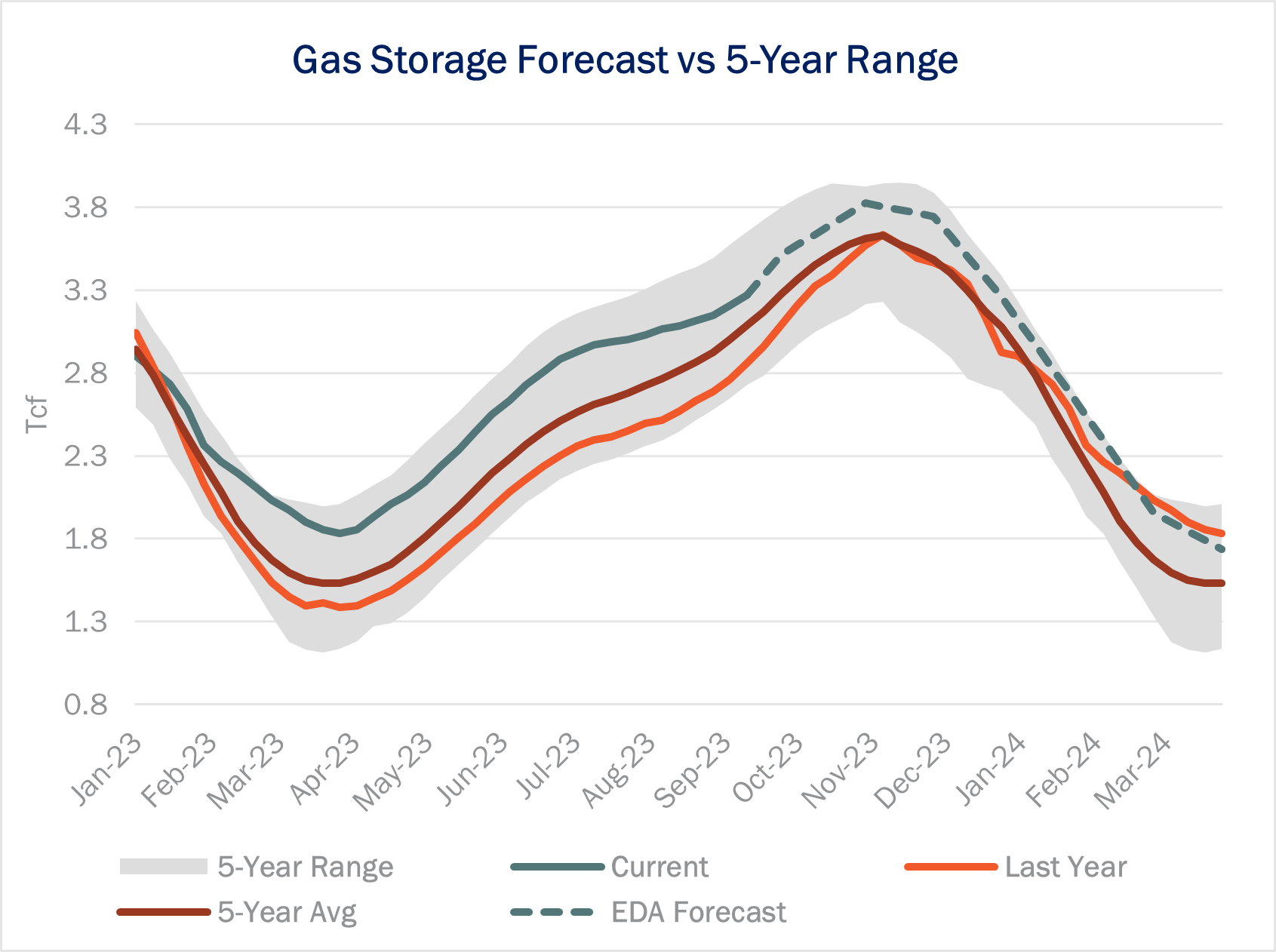

Storage - Traders expect EIA to report an 81 Bcf storage injection for the October 27 week in this Thursday's storage report. Lower 48 storage inventory currently totals 3,700 Bcf, 313 Bcf greater than last year and 183 Bcf greater than the 5-year average.

Storage - Traders expect EIA to report an 81 Bcf storage injection for the October 27 week in this Thursday's storage report. Lower 48 storage inventory currently totals 3,700 Bcf, 313 Bcf greater than last year and 183 Bcf greater than the 5-year average.

The surplus to the 5-year average has been relatively steady over the past five weeks as injections have come more in line with 5-year averages, despite some surprises to the low and high side in weekly EIA estimates.

In the latest October Macro Supply and Demand Forecast, East Daley projects end-of-season storage levels reach 3,795 Bcf, 226 Bcf higher vs inventories at the end of October 2022.

EIA plans to delay the release of next week’s storage report to complete a systems upgrade. In a press release, the agency said it plans to release two weeks of gas storage data the following Thursday (November 16) covering activity for the weeks ending November 3 and November 10.

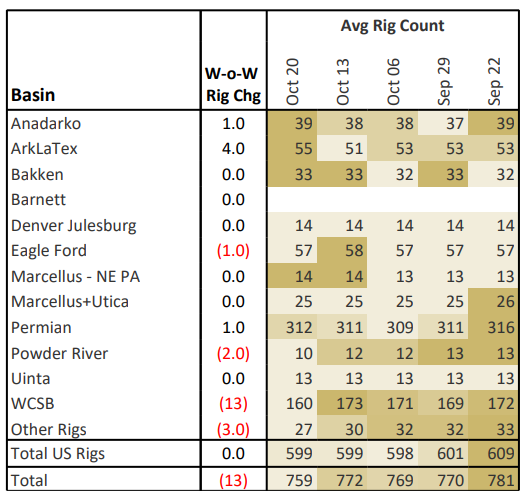

Rigs - The US rig count held flat W-o-W at 599 for the October 20 week. The ArkLaTex is up 4 rigs, while the Permian and Anadarko basins are up 1 rig each. The Powder River is down 2 rigs.

Rigs - The US rig count held flat W-o-W at 599 for the October 20 week. The ArkLaTex is up 4 rigs, while the Permian and Anadarko basins are up 1 rig each. The Powder River is down 2 rigs.

East Daley, Hart Bring NEW Gas & Midstream Weekly on November 9th

East Daley is teaming up with Hart Energy on the NEW Gas & Midstream Weekly newsletter. This new report combines the strengths of Hart Energy's journalistic reporting and analysis on natural gas, LNG, midstream energy and deal-making with EDA's deep research and intelligence of hydrocarbons, storage and transportation.

Published every Thursday morning, this new powerhouse newsletter is an interactive and enlightening read highlighting breaking news, exclusive interviews, videos, charts, maps and more. The newsletter utilizes East Daley's Energy Data Studio tools for natural gas predictive analytics with Hart Energy's Rextag mapping tools to present a holistic view of pricing triggers, infrastructure growth, pipeline and processing bottlenecks, regulatory and legal hurdles, and the inevitable solutions.