Flows –Hedge fund Citadel has acquired E&P company Paloma Natural Gas for $1.2B, setting a high price on acquisitions in the Haynesville. Paloma is a midsized private operator, producing ~450 MMcf/d at the basin’s peak in 2023. Gas production declined to ~350 MMcf/d by YE24.

East Daley Analytics tracks rigs and volumes for Paloma and other Haynesville producers in Energy Data Studio. The company did not run any rigs for most of 2024 when gas prices were low, but has added back 2 rigs in 2025 as the market has recovered. Paloma operates on the Louisiana side of the ArkLaTex, sending most of its volumes to Kinder Morgan’s (KMI) Kinderhawk and Williams’ (WMB) Louisiana Magnolia gathering systems.

Last year, Rockcliff, a portfolio company of Quantum Energy Partners, was acquired by Tokyo Gas subsidiary TG Natural Resources for $2.7B. TGNR is one of the largest producers on the East Texas side of the Haynesville, reporting 1.3 Bcf/d of gross production in 2023 from five Texas counties. Production totaled ~1.1 Bcf/d at YE24.

Aethon could be the next company to be sold, though it is a significantly larger producer than either Paloma or TGNR. Aethon produces well over 2 Bcf/d from a widespread Louisiana and East Texas footprint, including acreage in the highly touted Western Haynesville, where wells are consistently reporting initial production rates of over 30 MMcf/d. For comparison, East Daley’s average East Texas IP rate is just under 12 MMcf/d. Given Aethon’s productive capacity and associated gathering footprint, we estimate that Aethon could sell for over $7B.

EDA sees potential synergies with Comstock Resources (likely as a merger rather than acquisition), which also drills in the Western Haynesville, and with BP. BP has signaled a shift back towards oil and gas in its corporate philosophy. At the recent CeraWeek conference, BP CEO said that “the Haynesville’s time has come†in response to rising natural gas prices. An acquisition of the second-largest producer in the Haynesville, closely linked to US LNG exports, would be a healthy addition to BP’s book of business.

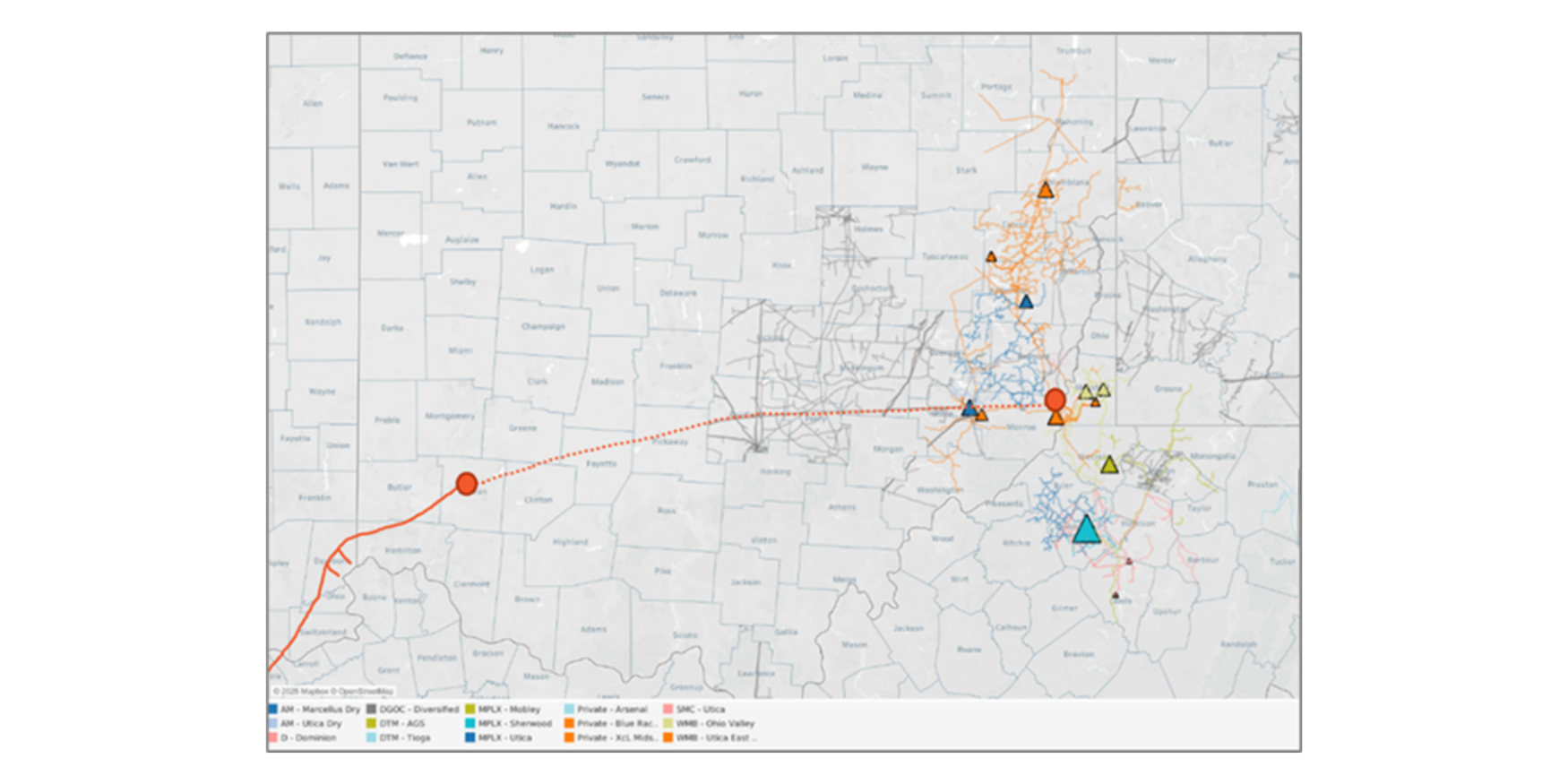

Infrastructure - Williams (WMB) is pursuing Project Socrates, a new investment in midstream and power infrastructure to support data centers being developed in Ohio. WMB is investing $1.6B in the project, including a power generation facility coupled with a supportive pipeline network. The company is targeting completion in 2H26, according to an 8-K filing.

East Daley Analytics tracks over 300 data center proposals like Project Socrates in the Data Center Demand Monitor. According to WMB’s website, the Socrates Power Solution Facilities will feature two power generation sites with a combined capacity of 400 MW in New Albany, OH.

Project mapping In the Data Center Demand Monitor shows that Franklin County, OH is an active area for data center projects. The county is set to host 2.2 GW of load from new data centers by developers such as AWS, DBT, Google, and Vantage. The map shows this cluster of potential load. The Project Socrates facilities could either support announced projects or back yet-to-be-revealed AI growth plans.

The 8-K filing states that Williams will back both the pipeline and generation components of the project. Based on the tight timeline, EDA believes that the pipeline will likely be intrastate. WMB operates the Blue Racer, Cardinal, and Flint G&P systems in Ohio, which could serve as origination points for the gas needed to support the project.

The boom in data center construction is spurring growth in U.S. gas demand and creating expansion opportunities for midstream companies. If Williams sources gas from its own G&P footprint, it can optimize the full value chain by gathering, transporting and converting gas to electricity, earning a rate at each stage. This strategy would increase in-basin consumption and would allow Northeast gas production to grow relative to EDA’s current forecast in the Macro Supply & Demand Forecast

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a 33 Bcf net storage injection for the week ending March 21, reflecting above-normal temperatures across most of the Lower 48. A 33 Bcf injection would make a big dent in the 5-year storage deficit, cutting it by 64 Bcf to 124 Bcf. The storage deficit vs last year would decrease by 63 Bcf to 561 Bcf.

Spring has arrived early in many regions, kicking off the start of injections much earlier than normal. EIA reported a 9 Bcf net injection for the week ending March 14, and forecasts call for balmy temperatures to continue for the rest of the month in many regions. March will likely register as one of the top ten warmest month of all time and leave end-March inventory at around 1,750 Bcf, slightly higher than East Daley’s outlook in the Macro Supply & Demand Report.

Henry Hub prices have traded lower W-o-W on the easing heating demand. The prompt month has fallen about $0.20 since last Wednesday (March 19) to trade near $3.84/MMBtu Wednesday. Looking ahead, EDA projects prices will rise this summer based on higher power and LNG feedgas demand. In the Macro Report, we forecast prices to average $4.38 in the summer and to peak in August at $4.59.

Rigs – The US rig count increased by 2 for the March 15 week, standing at 555. Basins losing rigs include the Permian (-6), Anadarko (-3) and DJ (-2). The ArkLaTex added 2 rigs on the week. The large W-o-W drop in the Permian is most likely due to rig moves and should recover next week.

On the midstream side, Kinetik (KNTK) is down 2 rigs on its Delaware Basin system. Energy Transfer (ET) is down 2 rigs total with losses on its Permian and Eagle Ford systems.

East Daley’s weekly Rig Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Rig Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.