Natural Gas Weekly: May 8th, 2024

Flows – The US interstate gas sample fell by 1.2 Bcf/d (2%) W-o-W for the week of May 5, continuing a trend that points to declining supply in reaction to low natural gas prices this spring.

The Haynesville (ArkLaTex) and the Northeast (Marcellus+Utica) saw the largest W-o-W decreases, down 180 MMcf/d (-1.7%) and 370 MMcf/d (-1.2%). The decline in the Haynesville sample since March has been steeper than East Daley had expected after producers guided to deferred production earlier this year.

Gas samples in liquids-targeted basins were relatively flat W-o-W. The Permian Basin sample rose by 1.5%, suggesting some production may have recovered from recent pipeline maintenance in the basin. Waha gas has frequently traded below zero this spring as production growth runs headlong into shipping restrictions during pipeline maintenance. We expect Waha prices to continue trading at a steep discount until the new Matterhorn pipeline begins taking linefill later this year.

Overall, pipeline samples have declined by 2.9 Bcf/d in the last four weeks, from 70.3 Bcf/d in early April to 67.4 Bcf/d. In our latest Macro Supply and Demand Forecast, EDA models Lower 48 gas production to average 102.6 Bcf/d in 2024; however, we are likely to lower that view based on the recent pipeline trend.

Infrastructure – Feedgas volumes to Cameron LNG have declined by over 700 MMcf/d so far in May, according to pipeline samples, as Sempra Energy (SRE) completes annual maintenance on one of three liquefaction trains. Pipeline samples show deliveries to Cameron fell to just under 1.4 Bcf/d on Tuesday (May 7).

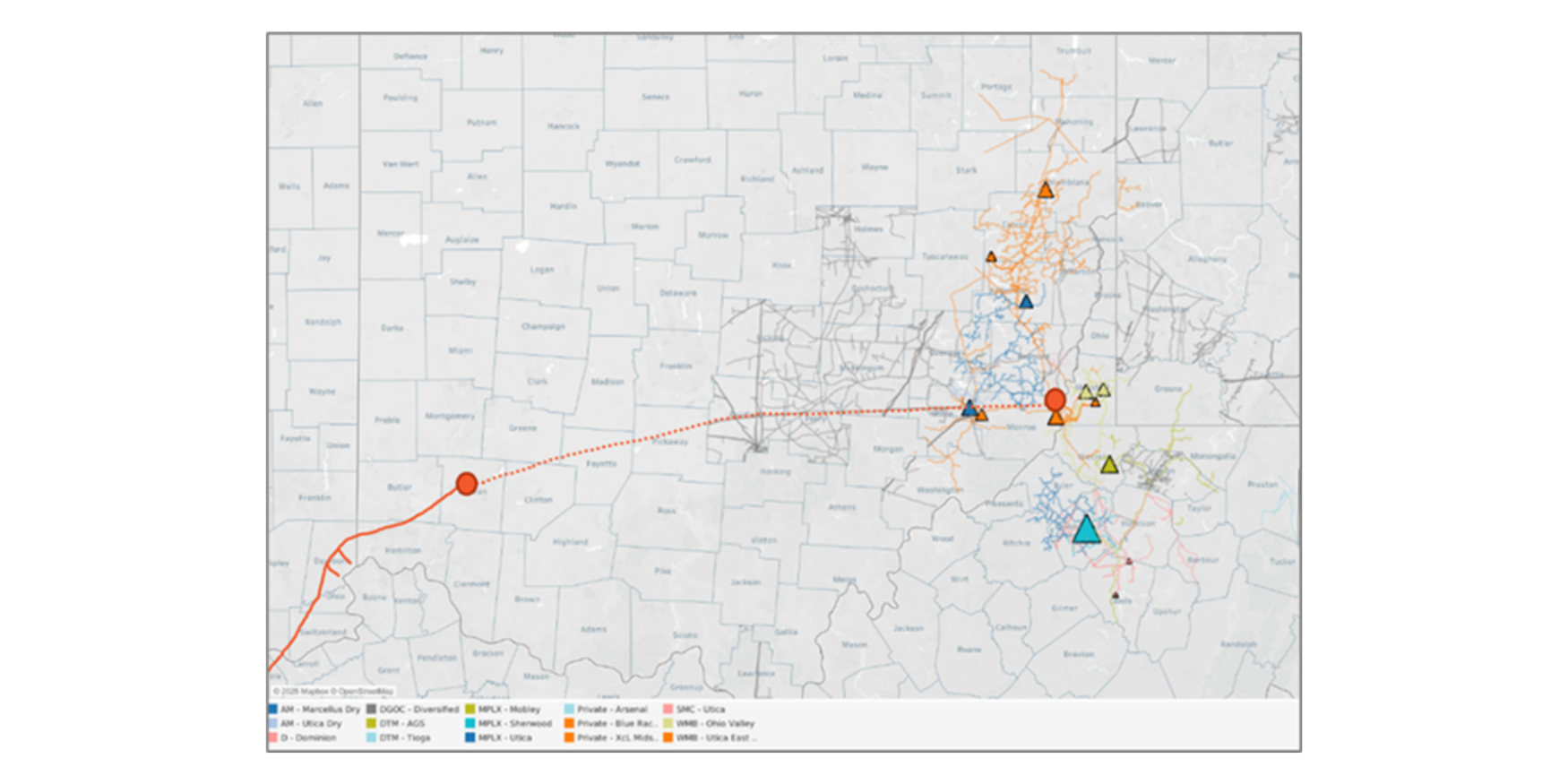

Maintenance at the Port Arthur, TX LNG facility typically takes about three weeks to complete, based on past pipeline deliveries to the facility (see chart). East Daley expects volumes to Cameron LNG will return to the full intake of ~2.2 Bcf/d by the end of May.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a net injection of 85 Bcf into working gas storage inventories for the week ending May 3. Inventories would rise to 2,568 Bcf, in line with our forecast in the monthly Macro Supply and Demand Forecast.

The storage surplus to the 5-year average would increase slightly by 3 Bcf to 645 Bcf based on market consensus, marking the ninth straight week of a surplus over 600 Bcf. The surplus to last year would come in at 449 Bcf.

While the inventory surplus remains stubbornly high, the June prompt-month contract has shown some strength through the first full week of May. The June Henry Hub contract is trading above $2.20/MMBtu and has gained about $0.26 (+13%) since May 1.

A combination of demand and supply factors have led to the upswing in price. Power demand in May has remained strong, up about 3.0 Bcf/d vs last year’s levels. Additionally, this week saw Freeport LNG return to service after months of outages and failed restarts. Finally, sustained lower production appears to be giving bulls a shoulder to lean on as the market prepares for elevated summer demand.

Rigs – US rigs declined by 7 W-o-W to bring the total count to 567 for the April 28 week. The Permian is down 2 rigs. The Anadarko, Bakken, DJ, Eagle Ford and Powder River all lost 1 rig.

On the midstream side, Energy Transfer (ET) is down 4 rigs with losses on its Permian, Eagle Ford, Anadarko and ArkLaTex systems. Targa Resources (TRGP) gained 4 rigs on its Permian systems.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.