Natural Gas Weekly: December 20, 2023

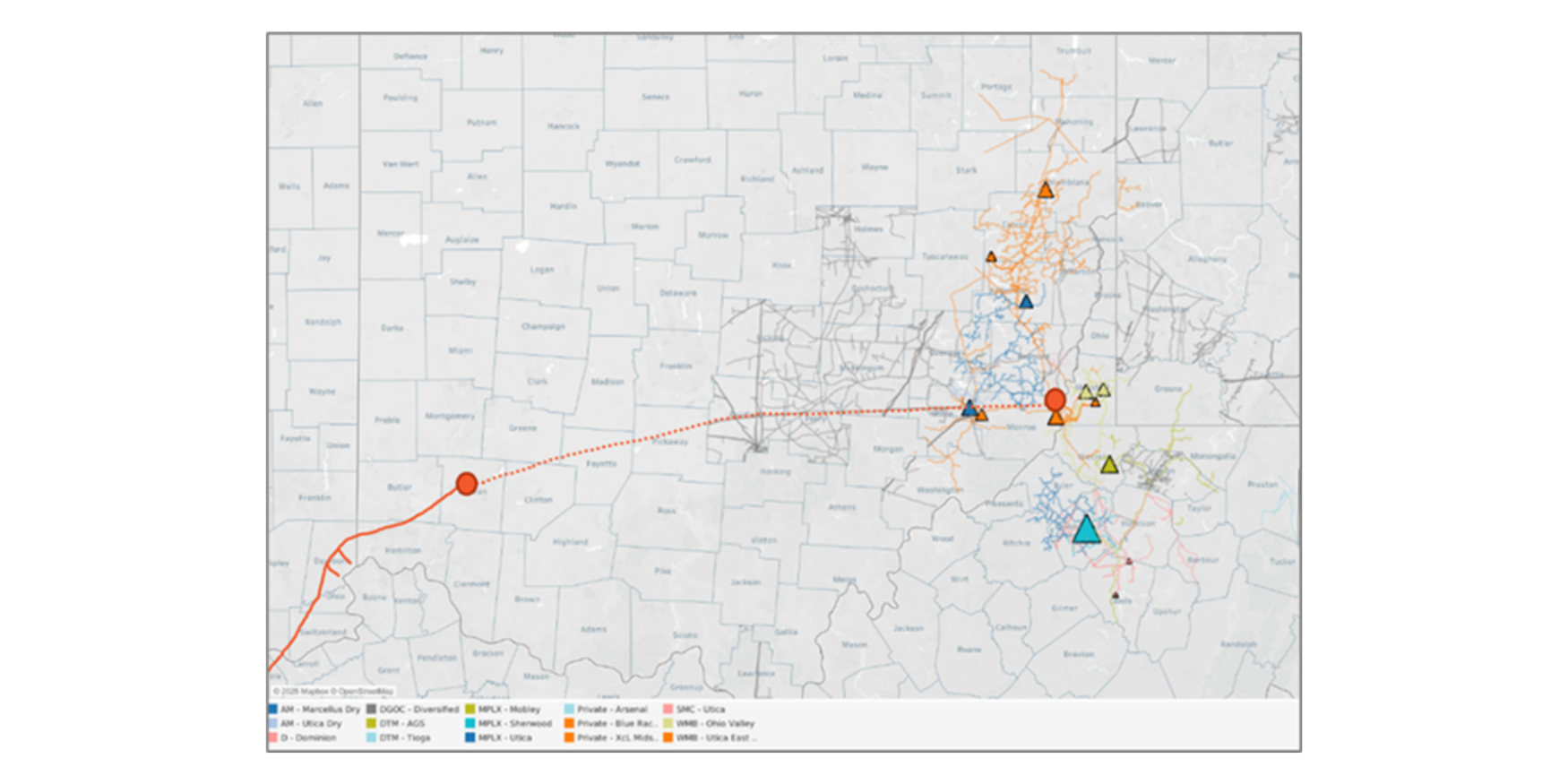

Infrastructure – After years of delay, construction work on Mountain Valley Pipeline (MVP) is nearing an end. In the Northeast Supply and Demand Forecast, East Daley Analytics predicts MVP will begin service in April 2024. How will the new pipeline impact market dynamics in the region?

While MVP will be able to carry up to 2 Bcf/d to southern Virginia, EDA expects the pipeline to transport only ~750 MMcf/d on average in 2024 due to downstream constraints at Zone 5 of the Transcontinental Gas Pipe Line (Transco). The Zone 5 bottleneck will persist at least until 2027, when Transco plans to start its Southeast Supply Enhancement expansion and add more downstream capacity.

East Daley clients can use the “Gas Pipeline Customer Contracts†screen in Energy Data Studio to analyze the shipper profile for MVP. Appalachian producer EQT is the largest capacity holder on MVP, followed by several LDCs and utilities in the mid-Atlantic. MVP provides these LDCs and utilities with optionality to source gas and connects them directly to cheaper supply within the Appalachian Basin.

According to contract data in Energy Data Studio, EQT has a firm transport (FT) portfolio that provides takeaway from the Appalachian region for about half its gas production, meaning the producer sells its remaining supply within the basin (see figure above). MVP will enable EQT to shift some gas sales from the basin, where Dominion South prices are typically discounted, and realize premium pricing at Transco Zone 5. As a result, EDA does not expect downside risk to any of EQT’s other pipeline contracts as a result of MVP.

By providing another connection between Dominion South and Transco Zone 5, MVP will help collapse the spread between the two markets to variable shipping cost. EDA anticipates less volatility in Transco Zone 5 pricing once MVP is placed in service.

Flows – A recent adjustment by the Railroad Commission of Texas (TRC) to its natural gas data reporting could play havoc with some forecasting models.

In the agency’s latest Drilling Productivity Report (DPR), released December 18, the Energy Information Administration (EIA) noted a change in the TRC’s methodology for reporting natural gas production. The TRC has discontinued applying a “well separation extraction loss factor†to condensate production reported by operators. As a result of the change, TRC-reported gross natural gas production fell by 2-3% in the historical data series for Texas.

East Daley believes the TRC’s methodology change ultimately does not impact residue gas production from Texas, though it will change how we calculate shrink from the wellhead to the residue stream. We have noted a slight discrepancy comparing the latest EIA drilling report. Since September 2023, EDA has been in line with the latest DPR release.

In the Permian Supply and Demand Forecast, EDA forecasts gross natural gas production from the Permian to average 25.5 Bcf/d in 2024, or 8% (2.0 Bcf/d) higher than the 2023 average.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to post a -81 Bcf withdrawal from working gas for the December 14 week, according to a survey by John Sodergreen’s The Desk. The estimate is in line with the withdrawal for the same week last year (-82 Bcf) but is 26 Bcf less than the 5-year average withdrawal (-107 Bcf).

If market estimates prove accurate, the storage surplus to the 5-year average would increase once again to 286 Bcf, the largest storage surplus since the week ending August 11, 2023.

Weather forecaster Maxar predicts December will finish with 688 gas-weighted heating degree days (GWHDDs), which would be the third-warmest December dating to 1950. Only December 2021 and December 2016 showed lower total GWHDDS at 679 and 636, respectively.

With above-normal temperatures in forecasts for the balance of the month, storage withdrawals should continue to lag. In the Macro Supply and Demand Forecast, East Daley expects storage to exit December at ~3,450 Bcf, the highest seasonal inventory level in 12 years.

Rigs – US rigs remained flat W-o-W with the total rig count holding at 603 for the December 10 week. The Permian lost 5 rigs while the Anadarko and ArkLaTex added 3 rigs and 1 rig, respectively.

On the midstream side, Targa Resources (TRGP) lost 4 rigs total with reductions on its Permian systems. Enterprise Products (EPD) gained 3 rigs on its Eagle Ford and ArkLaTex systems. West Texas Gas gained 2 rigs on its Permian systems.