Natural Gas Weekly: January 24, 2024

Flows – Operators continue to restore production following a mid-January Arctic blast. The front, named Winter Storm Heather by meteorologists, brought extreme cold and heavy snow that disrupted operations in several oil and gas basins. A rapid warm-up is helping the recovery, but overall production remains lower.

In the Bakken, residue gas samples dropped 38% (-0.95 Bcf/d) over a five-day period (January 12-16) vs the trend in the first week of January, likely due to wellhead freeze-offs. The impact is higher than declines of 0.3-0.5 Bcf/d seen during past winter storms in the upper Midwest. East Daley has 100% sample coverage in the Williston Basin, so our estimates of freeze-offs are reliable.

Supply disruptions also spread to the Anadarko (-1.2 Bcf/d), ArkLaTex (-1.7 Bcf/d) and Permian (-0.9 Bcf/d) basins as temperatures dropped over the MLK holiday weekend.

Pipeline samples this week show gas production has started to recover but is still ~7% lower than flows registered for the first week of January. East Daley expects supply will fully recover in the next one or two weeks as the upcoming 6- to 10-day outlook from the National Weather Service expects above-normal temperatures across most of the US.

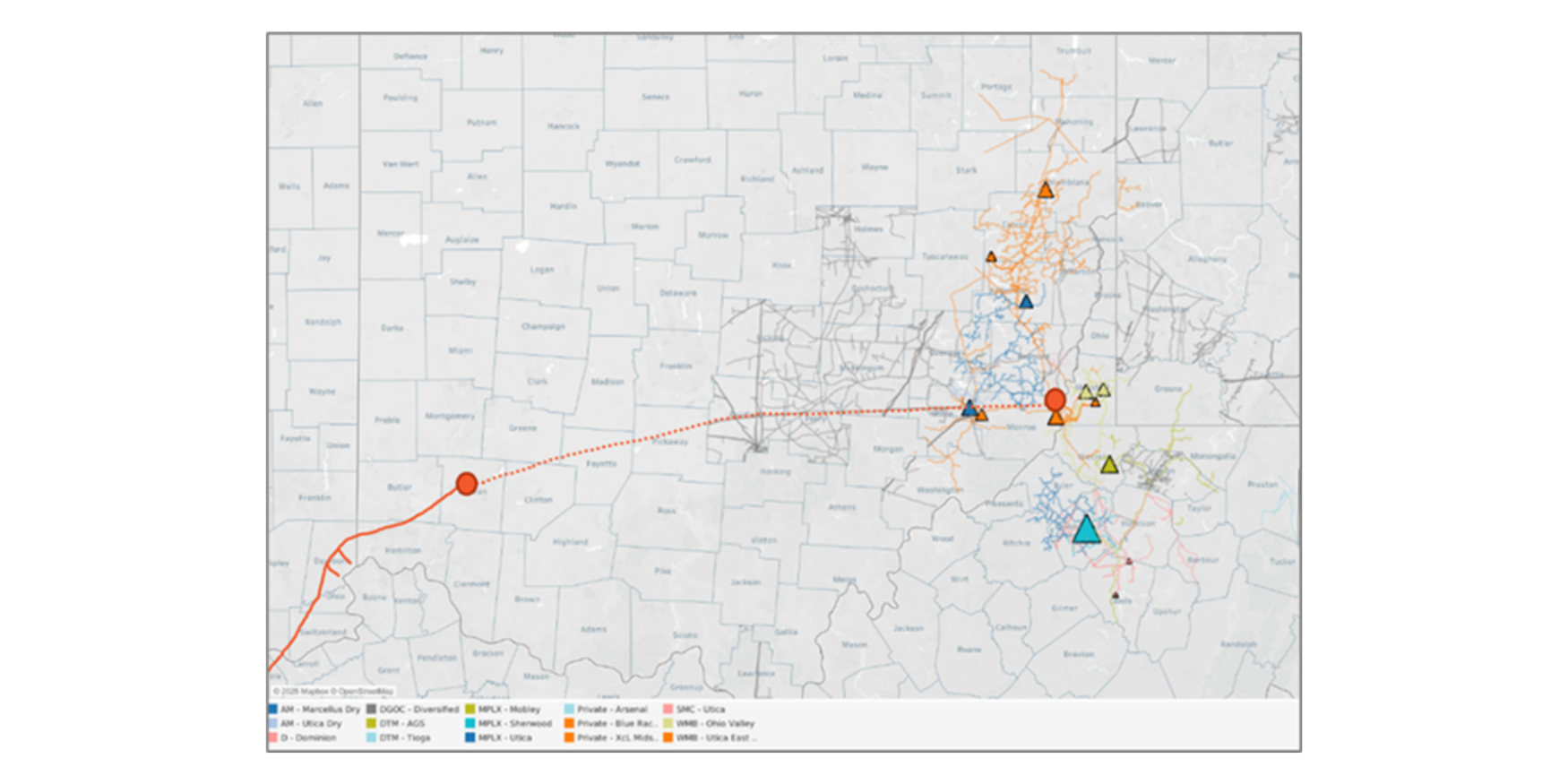

Infrastructure – A new joint pipeline project is helping move more natural gas south out of the Williston Basin to markets in the Rockies.

Kinder Morgan (KMI) and WBI Energy have teamed up on the 94 MMcf/d project. In the company’s 4Q23 earnings, KMI said Phase 1 of its Bakken xPress project began service in November ’23. The KMI project coincides with the start of WBI Energy Transmission’s Grassland South project.

Grassland South is a 15.3-mile pipeline connecting ONEOK’s (OKE) Bear Creek processing plant to KMI’s Big Horn Gas Gathering system in northeastern Wyoming. The gas delivered to Big Horn will travel south to KMI’s Fort Union Gas Gathering and then move onto the Wyoming Interstate (WIC) system.

While WBI spent the capital to build the lateral, WIC has executed 92 MMcf/d of leases on Big Horn and Fort Union to move volumes through those pipeline systems. The pathway provides access to the Cheyene and CIG hubs in the Rockies.

East Daley’s Bakken Supply and Demand Forecast includes impacts of the KMI/WBI projects. We believe the new Grassland South pipeline will help producers in the Williston and indirectly, in Western Canada as well.

The November in-service of the projects can be seen in pipeline samples from the Bear Creek plant. The Grassland lateral had been flowing close to full capacity prior to last week’s winter storm, when cold weather reduced production at Bear Creek (see figure). Nevertheless, the joint projects should provide more room for Bakken production to grow.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to post a potentially historic storage withdrawal from working gas inventories for the week ending January 18. The average estimate is for a 324 Bcf withdrawal, according to a survey by The Desk. The weekly EIA report includes soaring Res/Com heating demand and multi-basin production losses caused by Winter Storm Heather, forcing utilities and pipelines to lean heavily on storage to meet load.

Only two other weekly EIA storage reports have topped withdrawals of 300+ Bcf, as expected in Thursday’s report. The highest weekly withdrawal occurred the week ending January 5, 2018 at 359 Bcf. Winter Storm Uri in February 2021 caused a withdrawal of 338 Bcf for the week ending February 19, 2021.

The 5-year average withdrawal for the week ending January 18 is 148 Bcf, so the storage surplus is due to significantly contract. However, the tightening will be short-lived with widespread above-normal temperatures expected in key consuming regions through the rest of January.

In the new January ‘24 Macro Supply and Demand Forecast, East Daley forecasts storage to finish the 2023-24 winter withdrawal season at 1,884 Bcf, or 255 Bcf above the 5-year average of 1,629 Bcf. At the halfway point of winter, we break down our outlook for supply and demand for the rest of the season in the latest Macro Forecast.

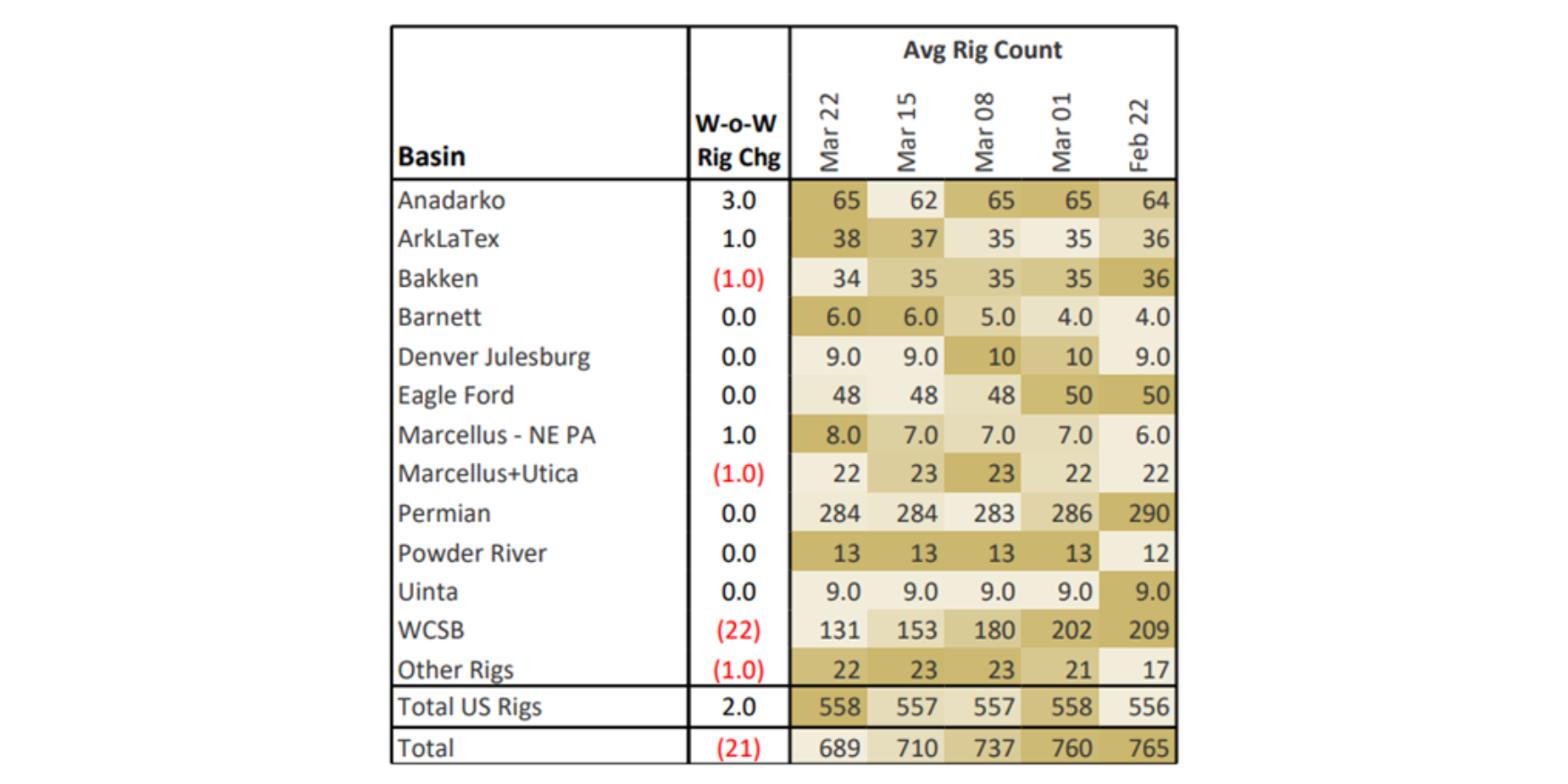

Rigs – US rigs decreased by 3 W-o-W to bring the total count to 592. The Permian lost 3 rigs for the January 14 week, while the ArkLaTex and Marcellus+Utica each fell by 1 rig. The Eagle Ford gained 2 rigs.

On the midstream side, EnLink Midstream (ENLC) is down 4 rigs with losses in the Anadarko and Permian basins. Enterprise Products (EPD) gained 2 rigs on its Eagle Ford system. Targa Resources (TRGP) lost 3 rigs on its Permian and Eagle Ford systems.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.