Flows – Leading Appalachian producer EQT has shut in ~1 Bcf/d of natural gas production in response to low prices, the company said in a March 4 press release. The producer began shutting wells on February 24, according to flow samples tracked by East Daley in the Northeast.

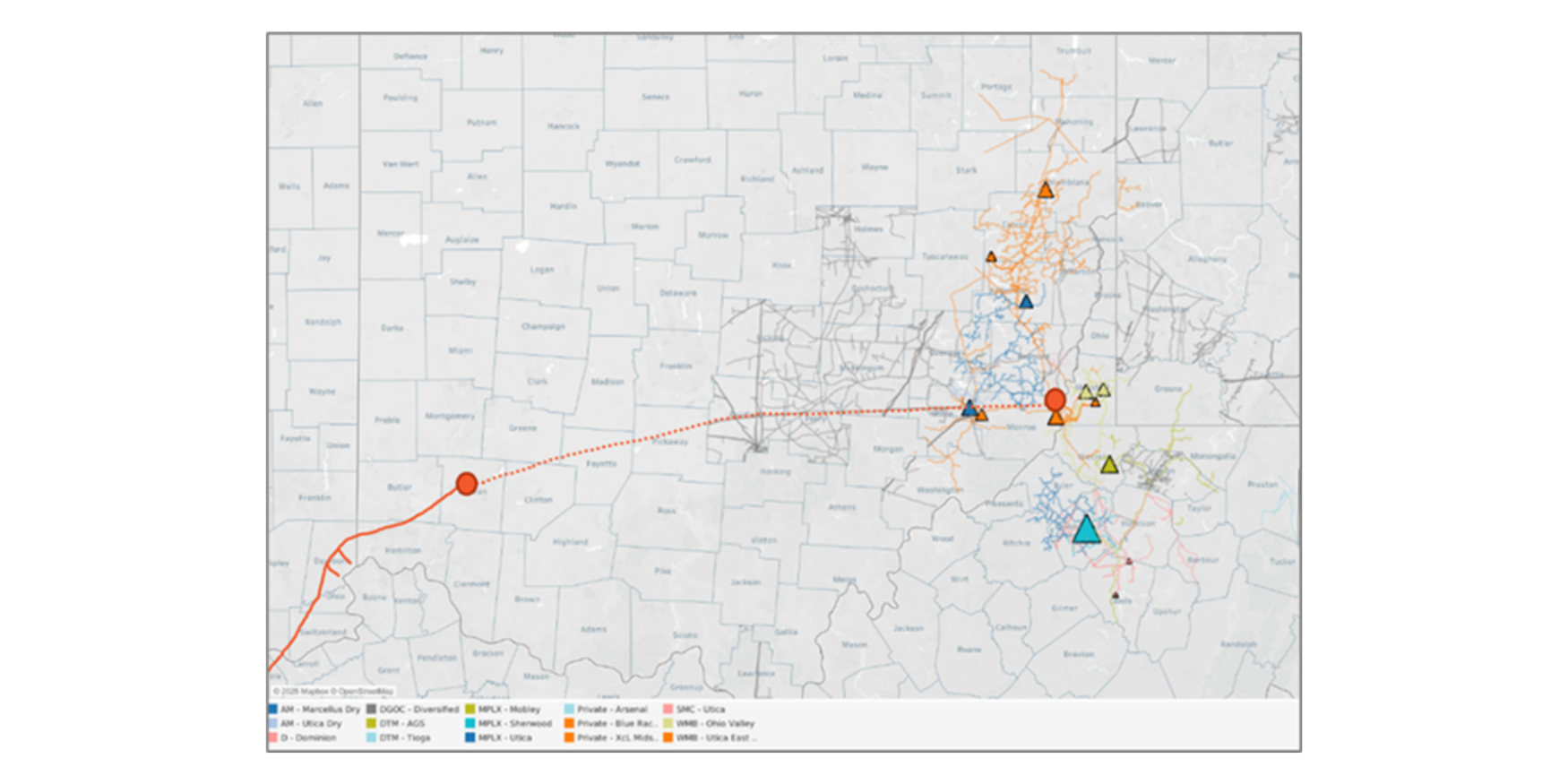

EDA’s proprietary tagging of G&P pipeline data allows us to track shut-in wells in real time and measure the impact to midstream systems. It appears EQT has cut its production exclusively in the Southwest Pennsylvania (SW-PA) region of the Marcellus, where EQT produces ~3.1 Bcf/d of gross gas normally. The shut-ins have reduced production in the region by one-third. Most of the decline (~750 MMcf/d) has occurred on Equitrans’ (ETRN) gathering system (see red line in figure).

EQT employed a similar strategy in 2020, shutting in ~1.4 Bcf/d when Appalachian prices fell below $1.50/MMBtu. The producer brought supply back three months later, only to reduce volumes once again in September ‘23. EQT restarted full production heading into the winter after prices recovered above $1.50.

Last summer, Dominion South prices fell to as low as $1.15/MMBtu, but East Daley did not observe material shut-ins at the time. The difference this year, and similar to 2020, is oversupply and weak prices are occurring amid the winter heating season.

We estimate EQT will begin bringing back production in May, ahead of the expected start of Mountain Valley Pipeline (MVP). Historically it has taken EQT about two months to restore production after restarting wells. This would mean recovery to EQT’s 2023 production levels by the end of June.

MVP is expected to begin service on June 1, and EQT holds over 1 Bcf/d of capacity on the new pipeline. The start of MVP should help Dominion South spot pricing. In our Macro Supply and Demand Forecast, EDA forecast Henry hub prices will recover to $2.50/MMBtu by July 2024, providing additional uplift to Appalachian prices.

Infrastructure – Equitrans (ETRN) once again has delayed the start of Mountain Valley Pipeline (MVP). In the company’s 4Q23 earnings call, ETRN pushed back guidance for the in-service date to May 31, 2024.

In the Northeast Supply and Demand Forecast, East Daley had previously modeled MVP to start on April 1, 2024. ETRN said weather was the largest factor for these additional delays. Commissioning is expected to take one month and is factored into ETRN’s new guidance.

We do not anticipate additional legal delays for MVP. However, ETRN has a track record of overly optimistic guidance, and a potential late-season snow could cause additional delays.

In the weak price environment, MVP should help marginally elevate Appalachian prices by opening additional capacity to Zone 5 of the Transcontinental system, which historically is short gas during peak-demand periods. However, in the Northeast Supply and Demand Forecast we forecast MVP will flow below capacity, operating at ~50% utilization the rest of the year. MVP will see a slight uplift from smaller expansions in the area, but we do not expect the pipe to consistently flow near its 2 Bcf/d of capacity until 2027, when Transco plans to start a 1.6 Bcf/d expansion.

Storage – Traders expect the Energy Information Administration (EIA) to post a light withdrawal of 38 Bcf from working gas for the week ending March 1, according to a survey by The Desk. Inventories would fall to ~2,336 Bcf for the week, in line with East Daley’s forecast in the monthly Macro Supply and Demand Forecast.

The storage surplus to the 5-year average would balloon to over 550 Bcf based on market estimates. The last week of February saw much above-normal temperatures across the Midwest and Northeast, cutting into seasonal heating demand.

Following this week’s EIA report, there are four more weeks left in the formal winter withdrawal season. Should storage withdrawals maintain pace with the 5-year average, inventory would exit March at about 2,179 Bcf. This would be the highest end-of-winter inventory since March 2012, keeping pressure on prices as the market transitions to the shoulder season.

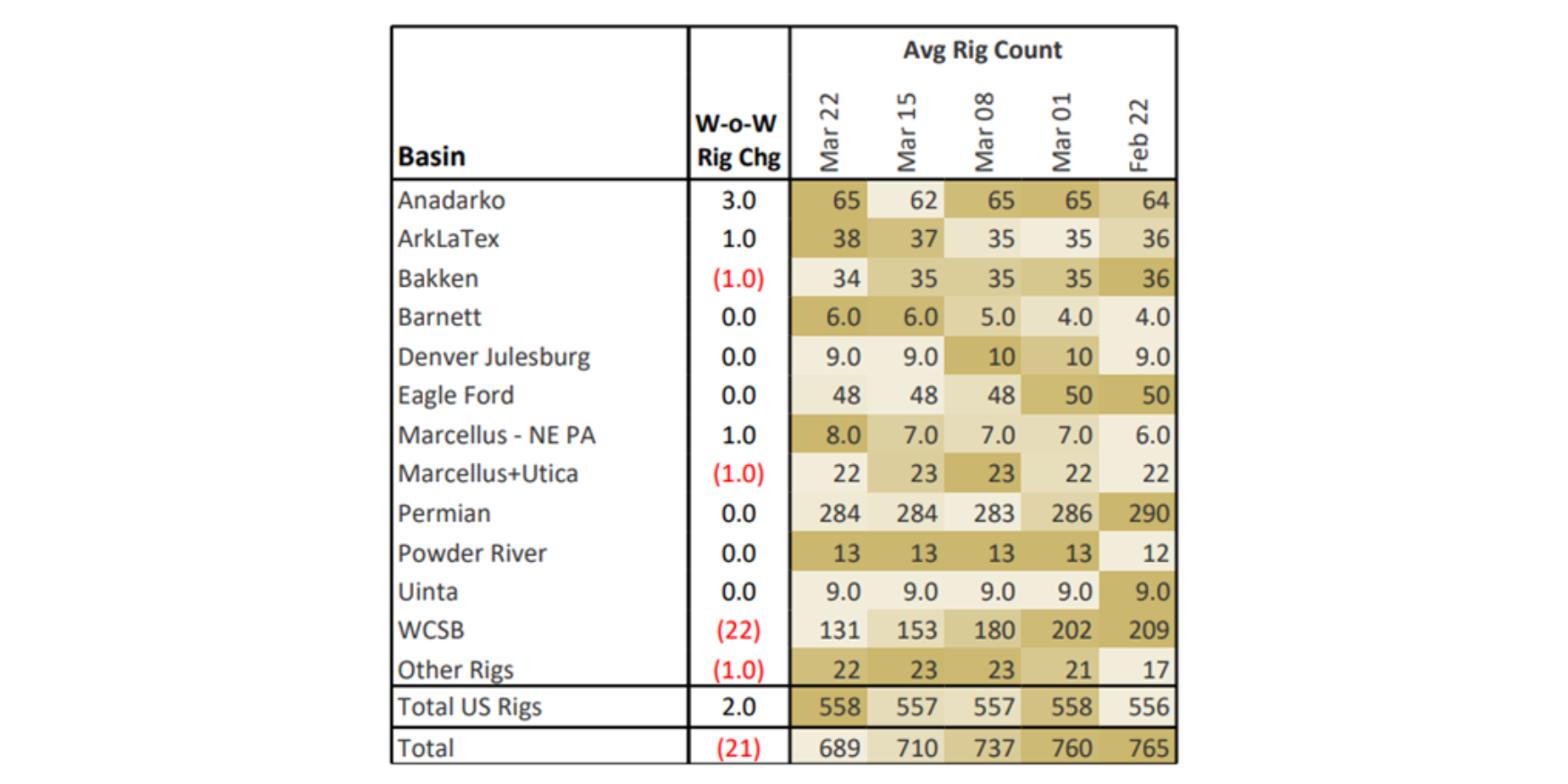

Rigs – US rigs decreased by 3 W-o-W to bring the total count to 594 for the February 25 week. The Permian is down 6 rigs, but this is most likely rigs moving and the count should rebound. The Eagle Ford is down 2 rigs while the Powder River and ArkLaTex basins are down 1 rig each. The Anadarko is up 3 rigs.

On the midstream side, Targa Resources (TRGP) is up 5 rigs with additions on its Permian systems. Western Midstream (WES) gained 2 rigs on its Permian systems. Energy Transfer (ET) is down 3 rigs on its Permian and Eagle Ford systems.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.