Flows – On the company’s first earnings call March 6, Venture Global (VG) reported some surprising figures for the Plaquemines LNG ramp schedule in 2025. To date, Plaquemines has produced LNG from 16 trains, running at 140% of the stated nameplate capacity of 1.33 Bcf/d. VG has built 34 of Plaquemines’ total 36 trains on site, with the remaining two deliveries expected later this month.

East Daley has observed ~1.6 Bcf/d of feedgas flows to the facility in March and an average of 1.18 Bcf/d over 1Q25. VG reported that 24 cargoes have been contracted so far in 1Q25, and 4-5 more are expected in March. However, VG guided to a potential 92 cargoes in 4Q25, which would indicate that it expects all trains to be online by the end of 2025, equating to over 3 Bcf/d of demand.

VG also clarified that Phase 1 and 2 of the Plaquemines project refer to when capacity will achieve commercial operations (i.e. cargos will still be sold on a commissioning basis until then), a measure that is less meaningful for folks who care about physical balances.

Prior to the latest guidance, Easy Daley assumed that Plaquemines Phase 1 would cap out at 2 Bcf/d, and the remaining 1 Bcf/d would come online later in 2026. Even under that assumption, we anticipated significant growth out of the Haynesville in order to balance the market, adding 2.5 Bcf/d of production between 2024 and ’25 (exit to exit).

There is some slack in our Macro Supply & Demand Forecast, as we have pushed back substantial completion of Corpus Christi Stage 3 (1.5 Bcf/d) back from 4Q25 to 3Q26. However, the current ramp schedule for Plaquemines forewarns of serious market imbalances if producers don’t start ramping activity soon.

Flows - The Matterhorn Express Pipeline has ramped deliveries to the Katy market since late January and reached several milestones earlier this month.

Matterhorn flows to interstate pipelines hit a new high of 1.59 Bcf/d on March 3. The WhiteWater-backed pipeline also recently posted flows of over 1.5 Bcf/d for 11 straight days, from February 23 to March 5 (see figure).

Deliveries have ramped recently to Kinder Morgan’s (KMI) Tennessee Gas and Natural Gas Pipeline (NGPL) systems, pacing the new highs. Matterhorn also connects to intrastate systems in Katy where visibility is limited, so deliveries could be higher.

East Daley follows the 2.5 Bcf/d Matterhorn pipeline in the Houston Ship Channel Supply & Demand Report. Started in October ’24, Matterhorn is part of a trend of pipeline expansions bringing more Permian gas to South Texas and creating volatility in regional prices. See the Houston Ship Channel Supply & Demand Report for a detailed breakdown on the market outlook.

Infrastructure – Seasonal pipeline maintenance is set to impact volumes from the Permian Basin, as several major pipelines prepare to take capacity offline.

El Paso Natural Gas (EPNG), Gulf Coast Express (GCX), and Permian Highway (PHP) have announced service outages in March and April. While EPNG regularly experiences maintenance-related capacity reductions due to the system’s size and age, significant curtailments of 400 MMcf/d or more on the North Mainline and at Cornudas will have a greater impact on egress.

Meanwhile, planned reductions on PHP and GCX will limit eastbound egress to the Gulf Coast. These outages will be shorter in duration, with maximum capacity cuts of 820 MMcf/d and 950 MMcf/d, respectively.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a 46 Bcf storage withdrawal for the week ending March 7. A 46 Bcf draw would be 10 Bcf less than the 5-year average withdrawal, and would move the 5-year deficit to 214 Bcf from 238 Bcf. The storage deficit vs last year expanded to 585 Bcf last week and would expand by another 27 Bcf this week.

Henry Hub spot prices have averaged $4.34/MMBtu this month, an uptick over February’s average of $4.22. In our Macro Supply & Demand Report, East Daley predicted February ’25 prices to average $4.25, and we expect the same price average for March.

The Henry Hub ticked above $4.50/MMBtu the first two days of this week, but has since retreated below $4.20. Similarly, the prompt-month April contract lost $0.35 (nearly 8%) on Wednesday, reflecting an outlook for weaker demand the rest of the month. Gas-weighted heating degree days (GWHDDs) are forecast to be over 10% below the 10-year norm for March. The forecast could place this month among the top ten warmest March’s ever, according to Maxar Weather.

March withdrawals typically come in much lighter as temperatures warm and consumers use less gas for heating. March 2013 and 2014 saw the two largest monthly withdrawals at 379 and 344 Bcf respectively. In the latest Macro Supply & Demand Report, East Daley anticipates March 2025 will see about 220 Bcf of withdrawals.

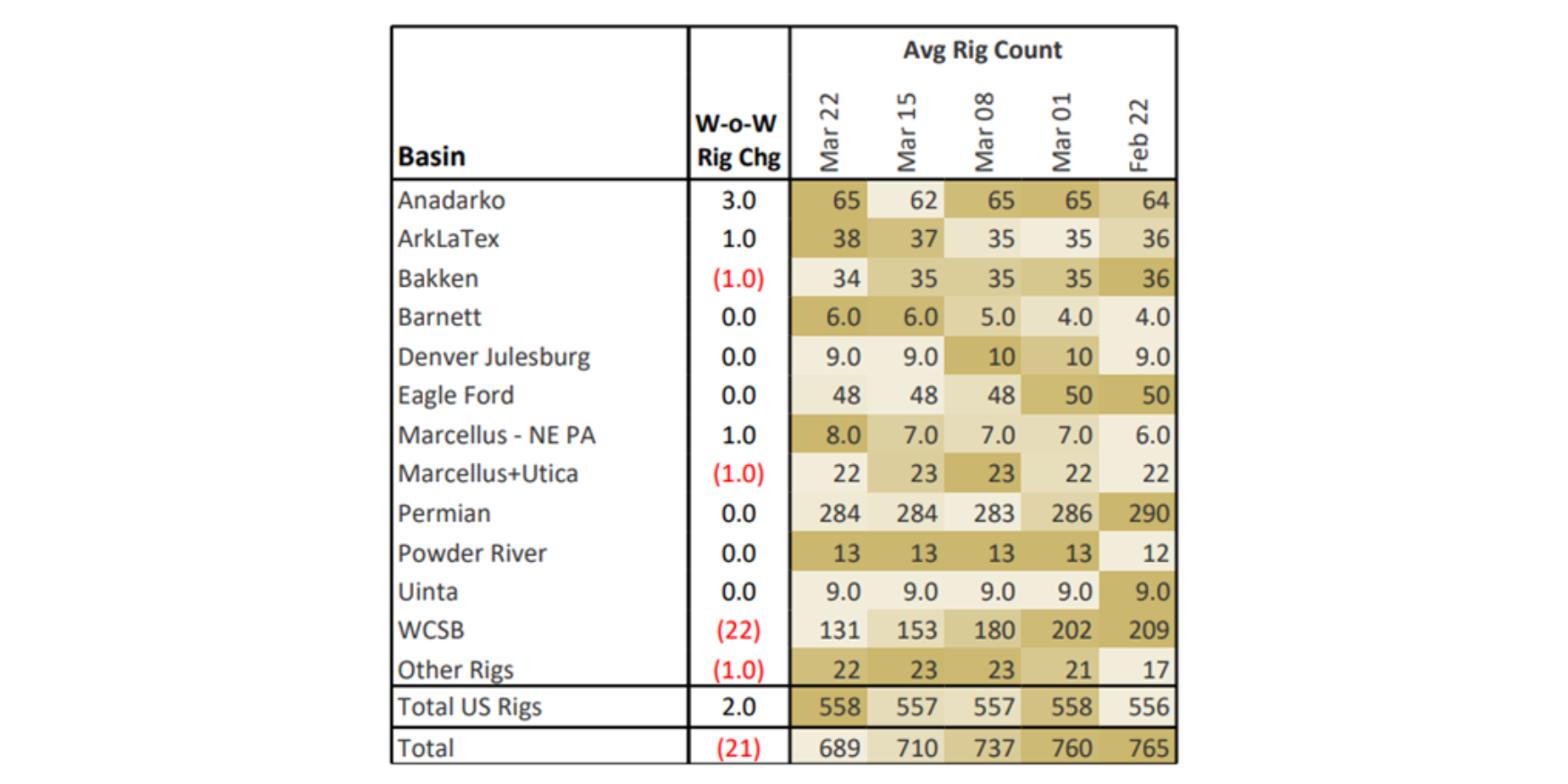

Rigs – The US rig count decreased by 1 for the March 1 week, standing at 555. Basins losing rigs include the Permian (-7) and the Bakken (-2). The large drop in the Permian is most likely due to rig moves and should recover next week. The Anadarko, Barnett, DJ, and Marcellus- NE PA each added 1 rig on the week.

On the midstream side, Phillips 66 (PSX) is down 5 rigs net with losses on its DJ, Eagle Ford and Delaware systems. Kinetik (KNTK) is down 2 rigs total on its Delaware system.

East Daley’s weekly Rig Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Rig Activity Tracker.

The Daley Note

Subscribe to East Daley’s The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.