Executive Summary: Market Movers: Devon has sold its 12.5% equity interest in Matterhorn for $375MM, and more midstream companies are successfully bringing projects to market to serve data center demand. Rigs: The US rig count totaled 473 for the week of April 21, down 7% from 1Q25 and 9% lower than 2Q24. Flows: Volumes averaged 48.5 Bcf/d for the week of April 21, up 1% from 1Q25 and 2% higher than 2Q24. Calendar: EDA provides updated plant volumes 05/15| SOBO Earnings 5/16

Market Movers:

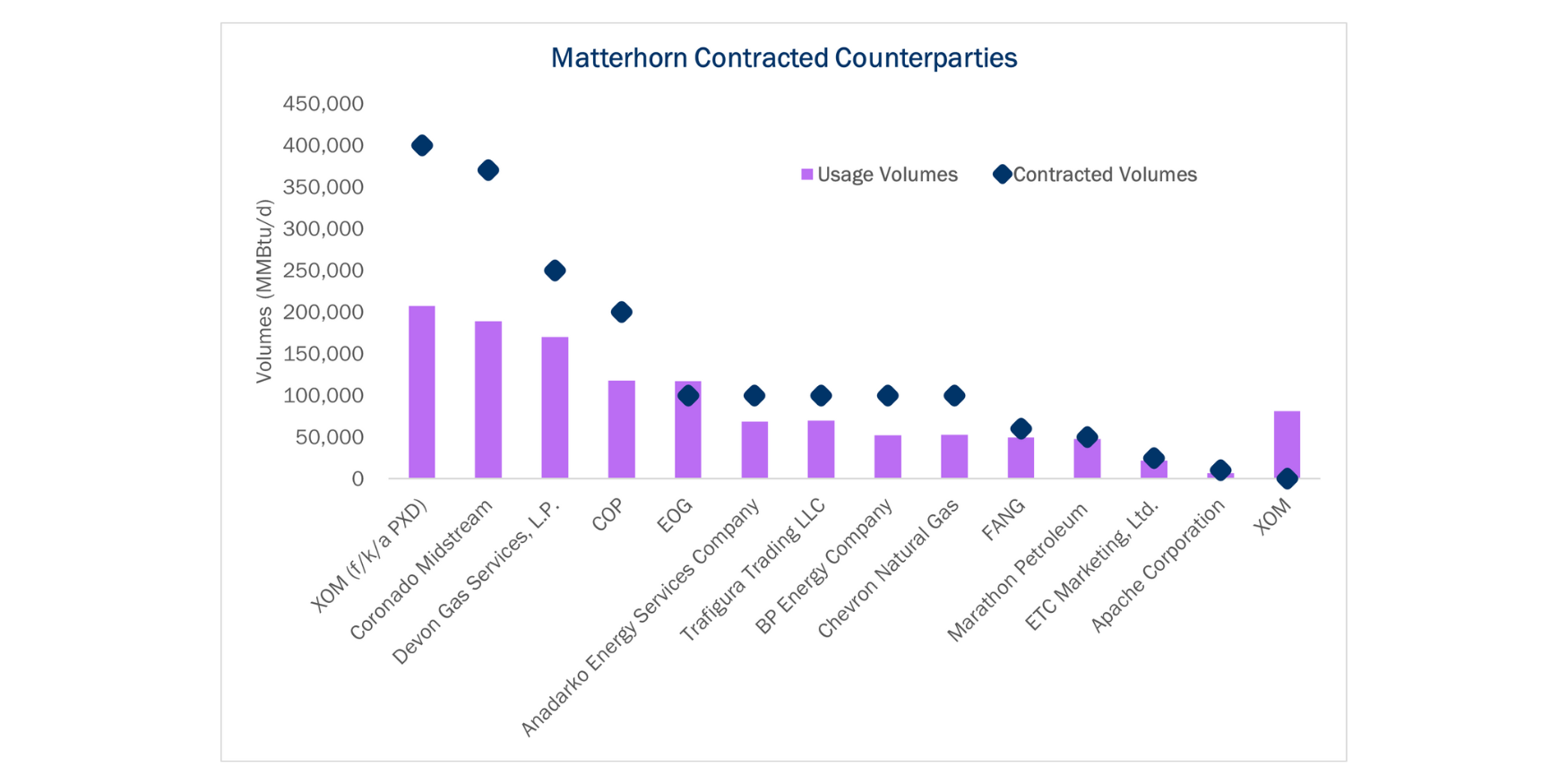

Devon Energy Sells Stake in Matterhorn

Devon Energy (DVN) has agreed to sell its 12.5% equity interest in Matterhorn Express Pipeline for $375MM, placing a marker on the value of the newest Permian natural gas pipeline. East Daley estimates a $5.5-6.1B enterprise value based on the transaction.

As shown in the chart below, DVN is one of the largest shippers on Matterhorn. The transaction does not change the producer’s underlying contract with the pipeline. Following the deal, WhiteWater Midstream will hold a 65% interest in the asset, while MPLX and Enbridge (ENB) will each hold a 10% interest. WhiteWater’s 65% stake will be backed by First Infrastructure Capital (62%) and I-Squared (38%).

Matterhorn plans to add compression and expand from 2.0 Bcf/d to 2.5 Bcf/d. In Moody’s debt rating published on May 6, the timing of the expansion is disclosed to be 4Q25, which is later than EDA’s expected in-service of July ’25.

If the ISD is pushed to 4Q25, Waha will continue to trade at a discount for a few extra months, and we could see downside to prices relative to the forward curve (shown below). This would 1) keep a cap on supply growth until 4Q25 vs 2H25 – slower growth for Permian producers already slowed by lower WTI crude prices and 2) present marketing earnings upside for shipper with spare capacity on Matterhorn.

Valuation Read-Through:

- Equity: The $375MM for the 12.5% equity interest grossed to 100% implies an equity value of $3.0B. If we slap on a 20% premium for a controlling ownership piece, the equity value is $3.6B.

- Debt: The Moody’s report notes debt held at the operating company was $2.25B as of March ’25.

- Implied EV: The total value of the asset is $5.5-6.1B based on the market value of equity and known debt outstanding.

- Based on EDA’s forecasted run-rate EBITDA of $425MM, that represents a 13.0x-14.4x multiple, a promising read-through to the market value of similar assets.

Consolidation is often a pre-cursor to non-core asset sales, especially in a lower commodity price environment. EDA expects companies like DVN will look to non-core asset divestitures to shore up leverage or stash dry powder for reinvestment into core business activities.

Data Center Projects Begin to Materialize

East Daley projects hyperscale data center load will drive 4.2–6.1 Bcf/d of additional natural gas demand by 2030 to fuel roughly 81 GW of new power capacity. In response, midstream companies are pursuing projects with markedly different risk profiles and timelines.

Williams’ (WMB) Power Express expansion on Transco will add 950 MMcf/d by 3Q30 to serve Northern Virginia’s “Data Center Alley,” where developers have announced over 20 GW of IT load. Underwritten at a sub-4.0x build multiple and backed by 20– to 30-year contracts with utilities, it shifts volume risk onto offtakers while securing stable, decades-long toll revenues.

TC Energy’s Northwoods project on ANR Pipeline takes a similarly conservative approach, adding 400 MMcf/d in late 2029. The $900MM expansion, funded at a 6.0x multiple and implying about $1.25/Mcf-day (based on ANR’s 82% EBITDA margin), is structured around 20– to 30-year offtakes with municipal and investor-owned utilities planning combined-cycle and peaking plants. By locking in long-tenor utility deals, TRP insulates its pipeline from project-specific load risk, even as permitting and construction span roughly 36 months.

WMB’s Project Socrates in Ohio adopts a faster, integrated model. Pairing 400 MW of gas-fired generation with an intrastate pipeline, it targets in-service in 2H26 — just 18 months after FID. With a $1.6B investment at a 5.0x build multiple, Socrates is underpinned by 10– to 15-year contracts that shield WMB from commodity price volatility but expose it to renewal risk post-expiration. By capturing margins across gathering, transport and generation, WMB broadens its counterparty set and accelerates delivery, even as shorter tenors introduce greater renewal uncertainty.

These three initiatives highlight a strategic divide: TRP and peers like KMI rely on long-term, utility-backed contracts to de-risk capacity demand, while WMB’s generation-plus-pipeline approach trades some offtake certainty for speed and broader market access. As data centers reshape power markets, each model’s success will hinge on balancing revenue security with execution agility.

Rigs:

- Williams (WMB) is experiencing flat Q-o-Q and Y-o-Y activity thanks to timely additions from Citadel’s Paloma acquisition. Many other G&P operations in the Haynesville and Northeast have seen more volatility in their rig allocations due to reduced producer capex.

- DT Midstream (DTM) is still sitting at 3 rigs, half of its rig count in 2Q24. As LEAP prepares to expand in 3Q25, an increase in volumes on Blue Union to fill expansion capacity on LEAP will lean heavily on delayed production and DUC inventories from last year, as drilling activity has remained conservative.

Flows:

- MPLX has seen the biggest swing relative to last week’s flows, with samples connected to its G&P operations down 200 MMcf/d vs the prior week. Despite the near-term volatility, flows remain above 8 Bcf/d, an improvement Q-o-Q and Y-o-Y.

- The other large reduction EDA notes is in the category of “All Other” production points, which has experienced ~190 MMcf/d decline W-o-W. Aside from MPLX, many of the systems in our coverage are showing marginal increases and consistency in W-o-W metrics.

Calendar:

.png?width=737&height=884&name=May%202025%20(1).png)