Exec Summary:

Market Movers: ONEOK (OKE) acquired the remaining 49.9% interest in the Delaware Basin JV from NGP XI Midstream Holdings, LLC for $940MM.

Rigs: KMI Bakken rig activity continues to climb while other Bakken systems owned by OKE see Y-o-Y reduction in drilling activity.

Flows: EPD systems are the current low performers relative to history, but volumes are still expected to grow Y-o-Y vs 2Q24.

Calendar: EDA will be in NYC June 17-19 and July 29-31. Please reach out if you would like to schedule a market update while we are in town.

Market Movers:

ONEOK (OKE) continued its buying spree by acquiring the remaining 49.9% interest in the Delaware Basin joint venture from NGP XI Midstream Holdings, LLC for $940MM. OKE will pay $530MM in cash and $410MM in stock under the deal announced June 3. The JV owns G&P assets in West Texas and New Mexico with 785 MMcf/d of gas processing capacity.

Deal Economics: East Daley estimates the deal adds $110MM in incremental EBITDA to OKE in the first 12 months following the acquisition, putting the multiple at a reasonable 8.5x. Counterparty data in Energy Data Studio shows EOG Resources (EOG), Coterra Energy (CTRA) and Matador Resources (MTDR) are the main producers feeding the system, contributing a combined 485 MMcf/d of throughput. EDA currently shows the system running at 620 MMcf/d (79% utilization), providing plenty of room for throughput growth.

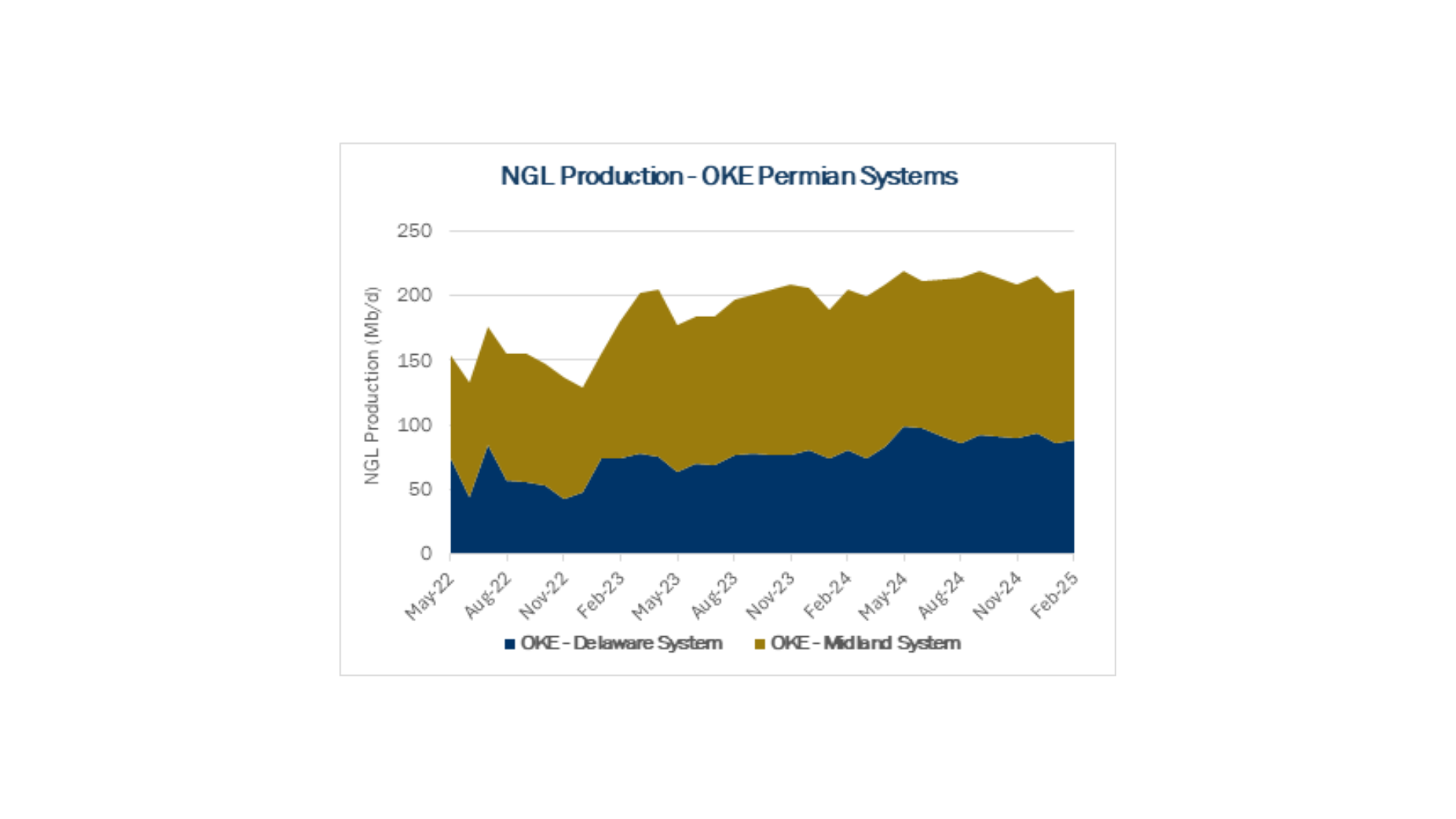

Increased NGL Ownership: We believe the acquisition is mainly driven by OKE’s desire to own more NGLs in the Permian Basin. In Feb ’25, the OKE - Delaware system (inherited from OKE’s purchase of EnLink Midstream earlier this year) produced almost 90 Mb/d of NGLs (see blue area in the chart), or 43% of OKE’s total Permian NGL production. Acquiring the remaining JV interest gives OKE full control of these NGL volumes.

OKE seeks to join an elite group that control NGLs from the field to downstream fractionators and export docks. The company in February announced a JV with MPLX to construct an LPG export terminal in Texas City, plus an LPG pipeline connecting OKE’s Mont Belvieu operations to the Texas City export terminal. OKE also recently completed the 375 Mb/d expansion of its West Texas NGL Pipeline, allowing it to move more NGLs directly from the Permian to Mont Belvieu.

Tapered Growth Expectations: The acquisition gives OKE more upside from moving NGLs from the Permian to the Gulf Coast to feed growing domestic and international demand for ethane and LPGs. There are potential headwinds, however. The Permian growth outlook is less rosy given lower WTI prices, and two of the largest producers on the system (CTRA, EOG) have significant acreage in the Marcellus and Utica they can pivot to, which may defer NGL growth behind OKE’s Permian plants.

Rigs:

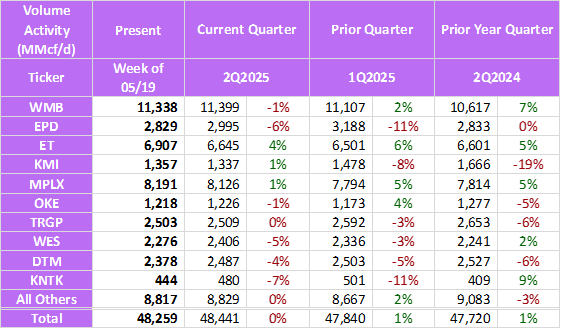

- KMI continues to see increased rig activity W-o-W, adding 1 rig each on the Altamont, Badlands and Bakken G&P systems. The adds come from Continental, Uinta Wax, and Marlo.

- OKE rig count of 16 for the week of 05/19 has some noise in it – the lower figure is caused by rig moves, with rig activity floating around 17-19. Even so, the sharp reduction in both Anadarko and Bakken drilling has led to a Y-o-Y decrease of about 38%.

Flows:

- EPD system volumes are currently 6% below the current average for the quarter, and 11% down vs 1Q24. Despite the downward swing in volumes, current flow samples are in line with those of 2Q24, reflecting limited growth opportunity but stability.

- ET continues to rally volumes in 2Q25. Volumetric results should drive Y-o-Y and Q-o-Q growth in ET’s business.

Calendar: