Quarterly Company Financials

Report Published: January 11, 2022

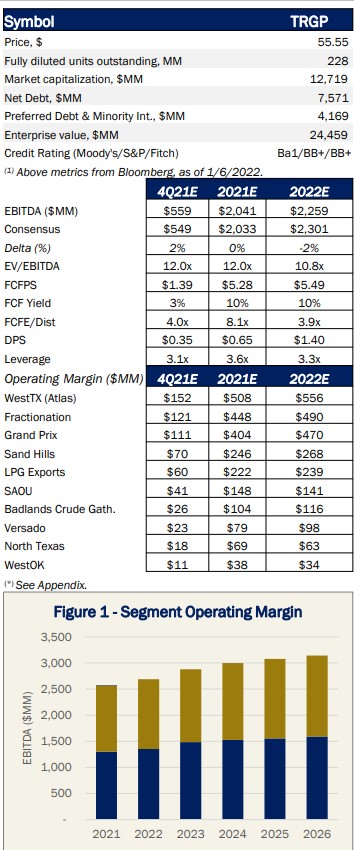

4Q21 Earnings Preview: East Daley forecasts Targa 4Q21 Adj. EBITDA of $559 million, up $53 million (10%) Q-o-Q and $10 million (2%) above consensus. We expect continued growth in G&P volumes, exports, fractionation, and Grand Prix volumes. Additionally, we model an uplift from commodity prices and marketing revenues.

and $10 million (2%) above consensus. We expect continued growth in G&P volumes, exports, fractionation, and Grand Prix volumes. Additionally, we model an uplift from commodity prices and marketing revenues.

- We estimate modest 4Q21 volume growth in the Permian based on producer commentary from Endeavor and Pioneer. We currently model ~3% growth Q-o-Q for the Midland and Delaware systems.

- The estimated average realized natural gas prices increased Q-o-Q from $3.51 to $4.74/MMBtu. We model NGL prices remained flat and condensate avg. realized prices declined Q-o-Q. This is based on TRGP’s disclosed hedging position but could mean upside to our forecasts if hedging risks are less severe than anticipated.

- We model Grand Prix volumes increased 5% Q-o-Q, from 417 Mb/d to 438 Mb/d, partly due to modeled increases on TRGP’s G&P footprint but also increased volumes from Eagle Claw and Sendero Midstream. We also forecast additional volumes from the Blue Stem pipeline.

- Fractionation volumes are modeled to increase by 15.1 Mb/d Q-o-Q (for a total of 677.1 Mb/d). We previously anticipated contract roll-offs during 2H2021. However, we no longer believe this to be the case – DCP’s contract with the Cedar Bayou facility, though announced in 2011, is believed to have taken effect in 2013. Assuming a 10-year term, we anticipate minimal risk in 2023.

- We forecast exports to recover from maintenance events and weather disruptions in 3Q21. EIA’s propane, butane, and Isobutane Gulf Coast export data indicates a 5% increase Q-o-Q. Previously, we referenced EIA’s total LPG exports (which includes ethane in its dataset) but have modified our forecast to better reflect TRGP’s export profile.

- Midland gas processing capacity appears to be constrained. TRGP can shift volumes to its Delaware processing plants and other third parties if needed, but more infrastructure is required. We currently forecast an additional plant will be required after Legacy (2022). Depending on how much natural gas from the Midland can be processed at TRGP’s Delaware plants, there may be a need for another processing plant on top of the additional plant already forecasted in our model.

- Currently, some TRGP plants feed other NGL pipelines. We anticipate TRGP will eventually shift these volumes to Grand Prix. Some of these NGLs, along with Permian volume growth, drive increased transportation, fractionation, and export volumes in our forecast.

- EBITDA outlook: We are 2% below consensus for 2022, likely because of G&P inflation caps and a more bearish view on operating expenses. East Daley is in line with consensus in 2023 but is 3% above the Street for 2024-2026. This is likely due to our rig and volume forecasts overall.

- Outlook Change: We increased our fractionation volumes considerably based on the above commentary, linking volumes more closely with Grand Prix. We also included inflation rate escalators in G&P rates.

Gathering & Processing Rates Report

To bring greater transparency to markets, East Daley Analytics is undertaking a broad study of G&P system rates. We maintain asset-level financial models for over 1,000 assets owned by public companies. From this asset pool, we’ve identified 200+ G&P systems for which we can confidently assess rates. We’ve created a G&P rate methodology based on our balanced public asset models.

Report Published: March 11, 2022

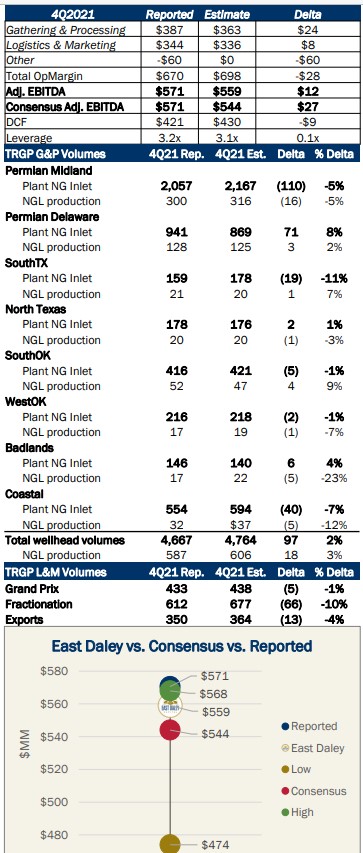

4Q21 Earnings Review: Targa reported 4Q21 Adj. EBITDA of $571 million, $12 million above East Daley and $27 million above Bloomberg consensus EBITDA.

Gathering & Processing: The G&P segment reported 4Q21 Adj. EBITDA of $387 million, $24 million above East Daley.

- Volumes: Total G&P volumes averaged 2% above our estimates while NGL volumes were ~3% above estimates. The Midland was surprisingly lower, which could be due to accounting changes, offsetting higher-than-expected Delaware throughput. We previously forecasted a need for two additional processing plants (after Heim) as well as constrained volumes on the Versado system. Management previously announced Legacy but has since announced Legacy II and a supplemental plant in between the Delaware/Midland (Midway). All three plants will add 825 Mcf/d in processing capacity.

- Realized Prices: Average realized price of $4.43/MMBtu outperformed our modeled average realized price of $4.36/MMBtu supplemented by higher realized prices for NGLs of $0.76/gal (vs. our modeled estimates of $0.69/gal). Average realized prices for condensate also outperformed expectations, coming in at $70.29/bbl vs. our modeled price of $60.04/bbl.

Logistics & Marketing: The L&M segment reported 4Q21 Adj. EBITDA of $344 million, $8 million above East Daley as a result of increased NGL sales/marketing volumes and lower-than-expected operating expenses.

Grand Prix volumes of 433 Mb/d were in line with modeled estimates of 438 Mb/d. Exports rebounded as expected but still lagged estimates by 4% for the quarter. In addition, fractionation volumes were as much as 10% below our 4Q21 forecast due to an unplanned maintenance event. TRGP is also planning a low-cost expansion (~32,873 b/d) at its Galena Park export facilities, targeting a mid-2023 start.

Uses of FCF / Strategy/ Macro Themes:

- EBITDA /FCF Outlook: TRGP guided to full-year 2022 EBITA guidance of $2.3 - $2.5 billion. Permian volumes provided by management are expected to be 12%-15% over 2021 average volumes. TRGP recently repurchased the remainder DevCo interest and subsequently sold off Gulf Coast Express Pipeline (GCX). As a result of the pipeline sale, TRGP said it intends to accelerate the repurchase of its preferred shares. TRGP also stated it anticipates paying a $0.35 dividend per quarter for 2022. As outlined during the quarterly call, TRGP has about $369 million left on its $500 million share repurchase program. Management also discussed the possibility of bolt-on acquisitions near its footprint that fit TRGP’s natural gas and NGL “profile”.