Natural Gas Weekly: August 1, 2024

Infrastructure – The expected start-up of the Matterhorn Express Pipeline has been pushed to 4Q24, according to a recent update by the contractor building the project. The revised construction schedule would delay by several months new natural gas volumes from the Permian Basin and keep prices under pressure in West Texas.

The timeline for the 2.5 Bcf/d Matterhorn project has been a subject of widespread industry speculation. Whitewater Midstream, the lead developer of the project, predicted a 3Q24 start-up date when Matterhorn reached FID in May 2022, but has been tight-lipped since on the project schedule.

With limited new information, market watchers have leaned on Gulf Companies, the engineering, procurement and construction (EPC) contractor building Matterhorn, for updates. Gulf Companies maintains a list of projects the company is building on its website, and recently had posted a 4Q24 completion target for the 400-mile Matterhorn mainline from Waha to the Katy hub, according to a review by East Daley Analytics. By last Friday (July 26), the language regarding Matterhorn start-up had been removed from the company’s website.

However, EDA has reviewed a revised construction schedule from Gulf Companies (updated as of June ’24) predicting completion of the Matterhorn project on September 17, 2024. That schedule is no longer publicly available, but would be consistent with the 4Q24 in-service target recently indicated on Gulf Companies’ website.

As a result, we are pushing back the start of Matterhorn volumes to October ‘24 in updates to our regional gas models, including the Houston Ship Channel and Permian Basin reports. We had previously forecast linefill beginning in July based on a previous schedule from Gulf Companies (published in September ’22). The just-released Macro Supply and Demand Forecast also assumes a delayed Matterhorn start.

The Matterhorn delay will keep Permian supply growth bottled up for a few more months, a factor supporting steep discounts to basin gas prices. Last week, Waha gas traded around $0.20/MMBtu. The revised schedule will also postpone cash flow for project investors. Along with Whitewater, Matterhorn partners include Devon Energy (DVN), EnLink Midstream (ENLC) and Marathon Petroleum (MPC).

Once flowing, Matterhorn will add more Permian gas to a saturated South Texas market. Pipeline capacity from the Permian Basin to South Texas increases to 12 Bcf/d after Matterhorn comes online, more than triple capacity of just 3.4 Bcf/d in early 2019, according to the Houston Ship Channel report.

As this new Permian supply floods into South Texas, EDA expects to see downward pressure on Houston Ship Channel basis. See the new Houston Ship Channel Supply and Demand Report for more information. An interactive dashboard is coming soon to Energy Data Studio – an early peek is shown in the figure.

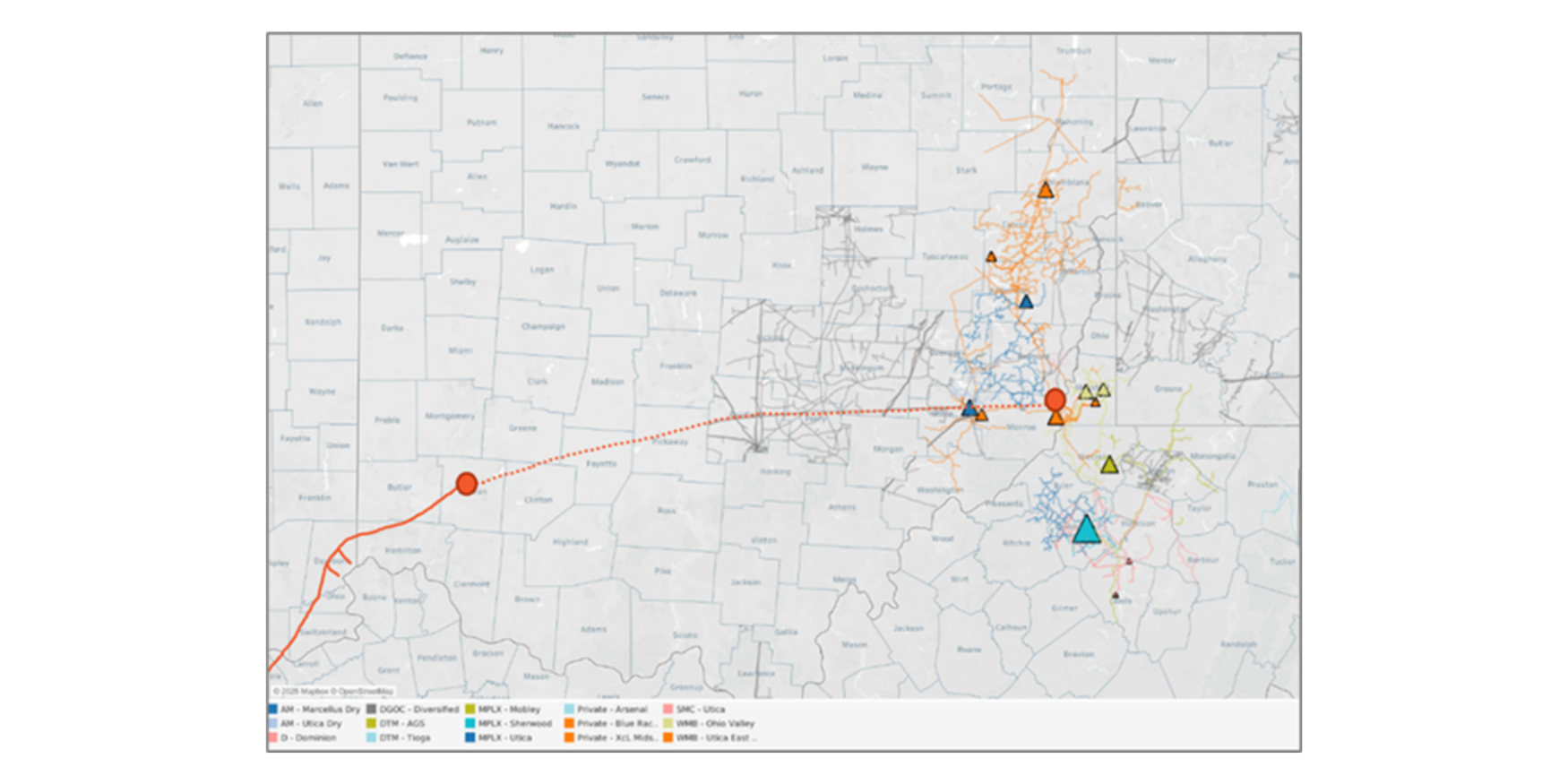

Infrastructure – DT Midstream (DTM) has started service on the LEAP Phase 3 expansion in Louisiana, the company revealed in its 2Q24 earnings update. The project is fully contracted under long-term take-or-pay agreements and brings the pipeline’s total capacity to 1.9 Bcf/d.

DTM is working to firm up customers for a Phase 4 expansion that is expected to add ~300 MMcf/d of capacity. The company also revised upward its expectations for potential pipeline capacity on LEAP from 3 to 4 Bcf/d.

DTM completed a new 1 Bcf/d interconnect with TC Energy’s (TRP) Gillis Access project in March ‘24, improving LEAP’s access to growing LNG demand.

Since February, LEAP throughput has declined by over 350 MMcf/d. However, we suspect that a significant share of those missing volumes have migrated to TRP’s intrastate Gillis Access line. During its earnings call earlier this week, DTM reported that, on average, Blue Union gathered volumes declined just 20 MMcf/d from 1Q to 2Q24.

Flows – Last Friday (July 26), El Paso Natural Gas Pipeline (EPNG) released a revised maintenance schedule for July and August 2024 that will limit flows to a total of 31 locations in New Mexico, Texas and Arizona. The work will reduce pipeline capacity by 123 MMcf/d.

KMI didn’t make any changes to its Caprock North and North Mainline forecast, which will continue to impact Waha basis prices and be heavily discounted against Henry Hub. Even with the flexibility the Permian Basin has to move gas through both interstate and intrastate pipelines, we are seeing a tight egress market from Waha into the Houston Ship Channel area.

Looking at the interstate meter sample, flows to EPNG have declined, while Transwestern Pipeline has seen an increase in flows over the last week (see figure). This suggest some volumes to the Southwest are being rerouted. Still, while rerouting helps gas egress, the Waha basis is expected to remain heavily discounted through 4Q24. Once completed, the Matterhorn pipeline will add up to 2.5 Bcf/d of capacity to the Waha-HSC corridor, covered by East Daley in the Permian Supply & Demand Forecast.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a 33 Bcf injection into working gas for the week ending July 26, in line with the 5-year seasonal average.

Last week EIA reported a 22 Bcf net injection, on the high side of market estimates. Inventories would rise to 3,264 Bcf based on market estimates, in line with East Daley’s monthly Macro Supply & Demand Forecast. The surplus to the 5-year average would hold at 456 Bcf, while the surplus to a year ago would increase by 18 Bcf to 267 Bcf.

In the latest Macro Supply & Demand Forecast, EDA forecasts working gas inventory will reach 3,884 Bcf by the end of October. This implies an injection pace 18.6 Bcf/week slower than the 5-year average over the next 15 weeks. For the first 15 weeks of the season, injections have only averaged 12.7 Bcf/week slower than the 5-year average. We forecast the injection pace must slow considerably from August-October in order to stay under demonstrated peak storage capacity of 4,203 Bcf. If capacity holders match the 5-year average injection rate each week, inventories would end up at 4,182 Bcf. Last year’s injection pace would result in 4,036 Bcf of inventories (see figure).

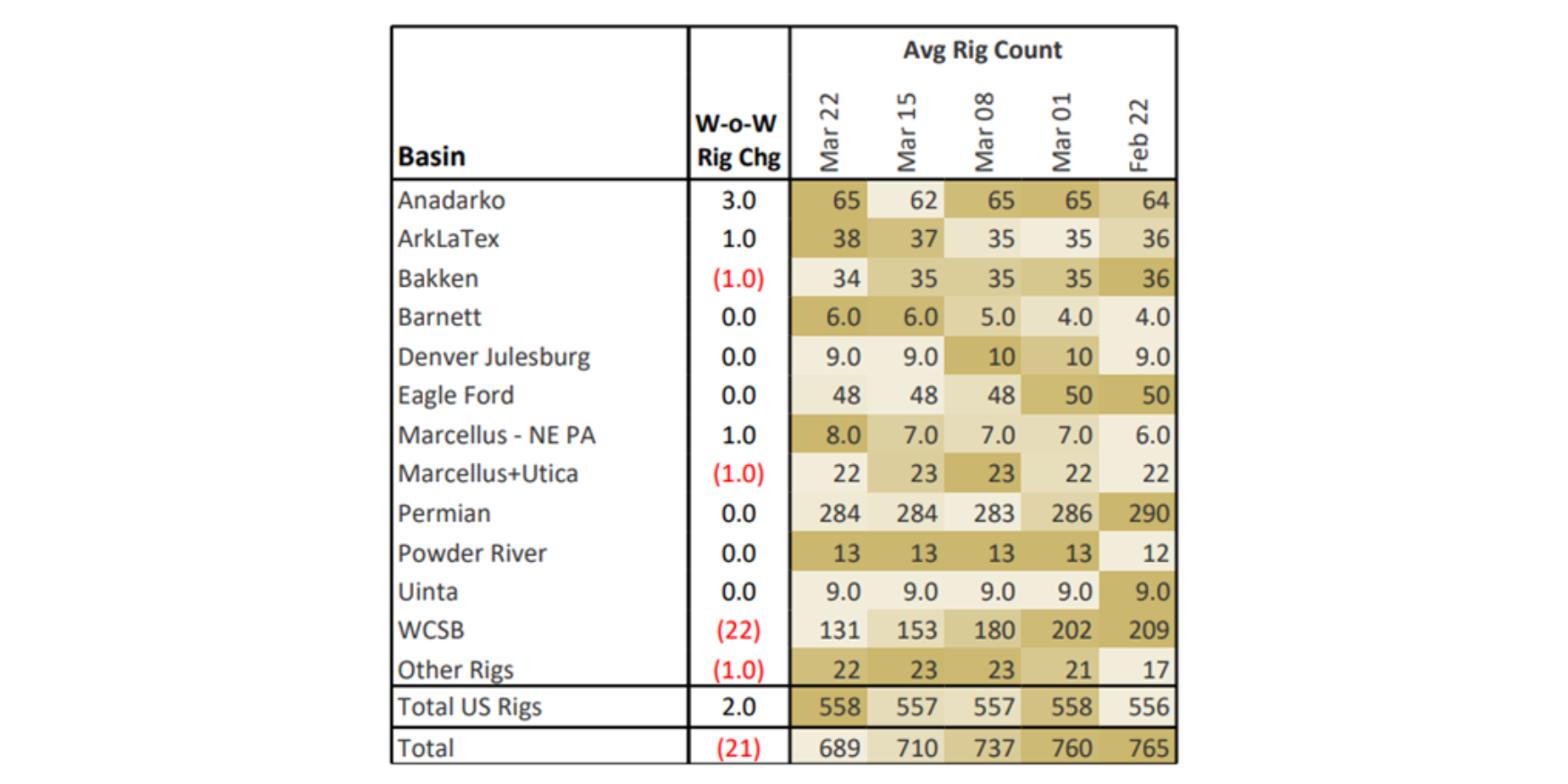

Rigs – US rigs declined 10 W-o-W to bring the total count to 538. The Permian and Anadarko basins are down 4 rigs on the week while the ArkLaTex, Bakken, Powder River and Eagle Ford are down 1 rig each. The Marcellus + Utica is added 1 rig on the week.

On the midstream side, Targa Resources (TRGP) is down 6 rigs total with reductions on its Permian, Eagle Ford, and Bakken systems. Energy Transfer (ET) is down 5 rigs on the week with reductions on its Permian, Eagle Ford, Anadarko, and Marcellus systems. EnLink Midstream (ENLC) is up 2 rigs on its Midland and Delaware systems.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.