Natural Gas Weekly: April 11, 2023

Infrastructure – Federal regulators have given Enbridge (ENB) the go-ahead to start service on a pipeline lateral serving new LNG demand on the Louisiana Gulf Coast.

On April 4, the Federal Energy Regulatory Commission (FERC) granted ENB’s Texas Eastern Transmission (TETCO) permission to place the Venice Lateral extension into service in Pointe Coupe Parish, LA. The new lateral on TETCO’s Line 40 will feed Venture Global’s Gator Express, the LNG header system serving the Plaquemines LNG export project under construction in southeastern Louisiana.

The Venice Lateral includes three miles of 36-inch pipe that will replace an existing 2.2-mile segment. TETCO will also construct a new compressor station in Pointe Coupe Parish to replace two existing compressors in Iberville and Lafourche parishes. The Venice Lateral will be able to move up to 1.26 Bcf/d to Gator Express and Venture Global’s Plaquemines project.

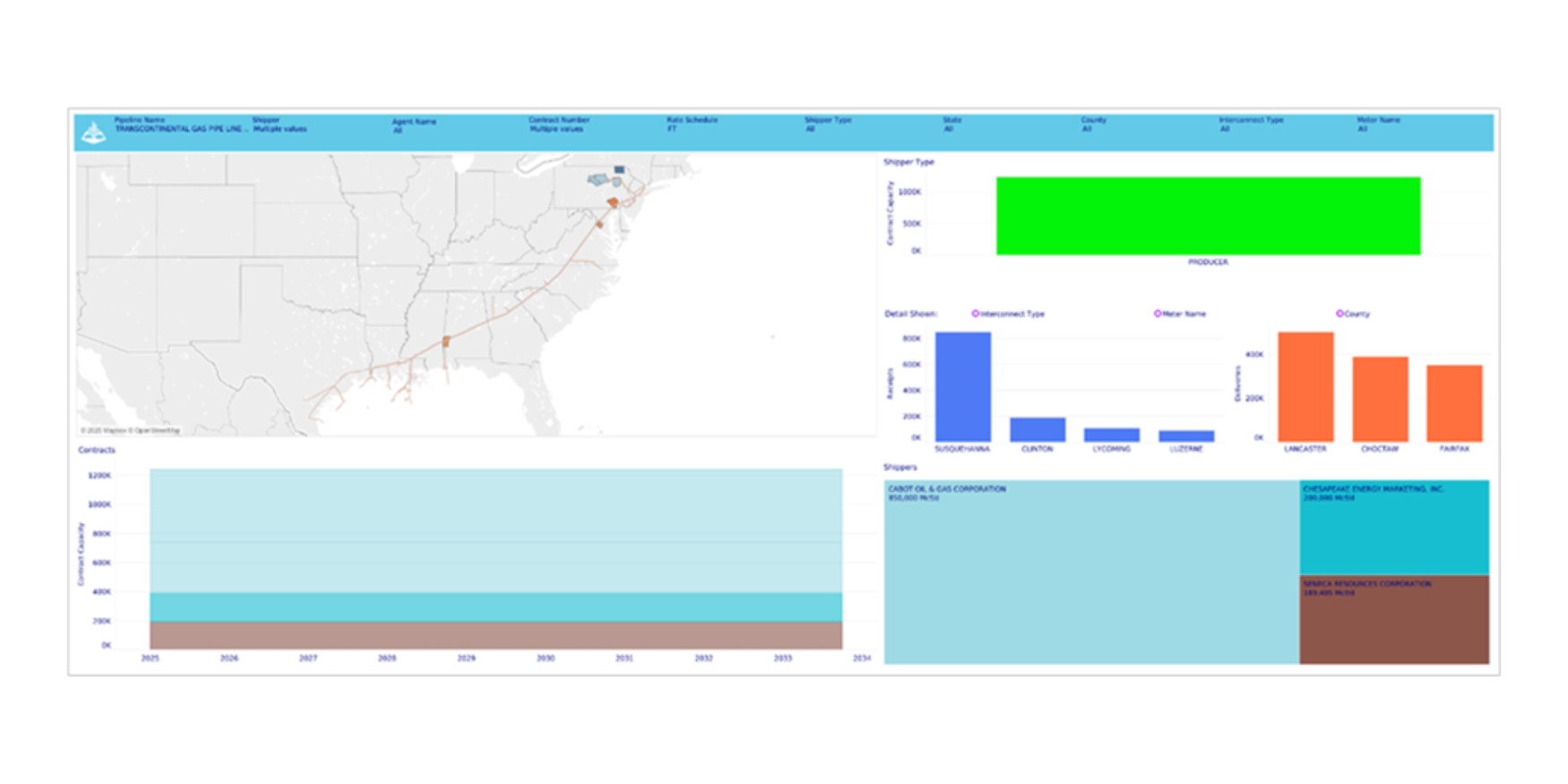

Plaquemines is part of the next LNG project wave set to transform the US natural gas market through 2030. East Daley tracks Plaquemines, the Venice Lateral and other infrastructure projects in the new Southeast Gulf Supply and Demand Forecast. The figure from the report shows our forecast for pipeline flows in southeastern Louisiana sub-region. The Southeast Gulf Forecast connects EDA’s Haynesville supply forecast in East Texas and Louisiana to regional pipeline flows, midstream expansions and Gulf Coast LNG projects for a comprehensive view of the regional market.

At the CERAWeek conference in March, Venture Global announced that Plaquemines would begin taking gas sometime in June, with first LNG projection expected this summer. East Daley forecasts Plaquemines LNG Phase 1 (2.25 Bcf/d) to ramp to full capacity by 2Q25 in the Southeast Gulf Supply and Demand Forecast.

Flows – The U.S. interstate gas sample was flat W-o-W for the week of April 7. Gas-driven basins were relatively flat with some puts and takes between the Haynesville (ArkLaTex) and the Northeast (Marcellus + Utica).

Samples in liquids-targeted basins were down slightly by 0.7% W-o-W. The primary driver is a drop in the Delaware Basin gas sample. Ongoing maintenance on the El Paso gas pipeline continues to restrict supply and we are seeing a dip in volumes as a result. Additionally, Kinder Morgan’s Gulf Coast Express has announced future maintenance. The restrictions should keep Waha trading at a steep discount until the new Matterhorn pipeline begins taking linefill.

The Eagle Ford pipeline sample is up 12.5%. However the sample coverage in South Texas is low at about 25%, introducing a large error range. We have seen no corroborating evidence via price or flows through infrastructure to confirm any real variability in supply.

In our latest Macro Supply and Demand Forecast, EDA models Lower 48 gas production to average 103.1 Bcf/d in April ‘24, down from 103.3 Bcf/d in March.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a 14 Bcf injection from working gas for the week ending April 5. Working gas inventories would increase to 2,273 Bcf, in line with East Daley’s forecast in the monthly Macro Supply and Demand Forecast. The surplus to the 5-year average would fall by 8 Bcf to 623 Bcf based on market expectations, while the surplus to last year would stand at 418 Bcf.

For April, East Daley expects the injection rate to fall below the 5-year average and further cut into the surplus. By the end of April, we model inventories at 2,480 Bcf, meaning the 5-year surplus would fall to 580 Bcf. While this is encouraging from a price perspective, our yield curve indicates that Henry Hub cash prices should remain below $2.00/MMBtu in the near term. In the Macro Supply and Demand Forecast, we project cash prices to cross the $2.00/MMBtu threshold in June ‘24.

Rigs - The US rig count decreased by 3 W-o-W to bring the total rig count to 587 for the March 31 week. The Eagle Ford, DJ and Powder River basins each gained 1 rig. The Permian lost 3 rigs and the Bakken is down 2 rigs.

On the midstream side, ONEOK (OKE) is down 2 rigs with losses on its Bakken and Anadarko systems. Kinder Morgan (KMI) lost 2 rigs on its Bakken and Eagle Ford systems. Targa Resources (TRGP) gained 4 rigs on its Permian and Eagle Ford systems. Equitrans Midstream (ETRN) is up 1 rig on its Pennsylvania Utica system.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.