Infrastructure – Moss Lake Partners has filed the initial paperwork for a new 42-inch gas pipeline out of the Permian Basin, joining a crowded field to build the next greenfield project to the Gulf Coast.

Moss Lake has started the pre-filing review at the Federal Energy Regulatory Commission (FERC) for the DeLa Express pipeline. The project would transport up to 2 Bcf/d over 690 miles from West Texas into Louisiana, connecting Permian supply to Gulf Coast demand centers in Port Arthur, TX and Cameron Parish, LA.

Based in Houston, Moss Lake will be competing against several other projects to move Permian gas east to the Texas Gulf Coast, including Targa Resources’ (TRGP) Apex and Energy Transfer’s (ET) Warrior pipelines.

East Daley Analytics tracks regional gas supply and flows in the Permian Basin Supply and Demand Forecast and the new Houston Ship Channel Supply and Demand Forecast. We expect start-up of the 2.5 Bcf/d Matterhorn Express Pipeline to alleviate severe gas egress constraints out of the Permian for a window of time. But the reprieve will be brief as steady Permian supply growth creates a need for more infrastructure to service that growth.

Given the long lead time required to permit, contract and build new large-scale projects, midstream companies now are negotiating the commercial contracts required to back financing for the next wave of pipeline projects. See East Daley’s coverage in The Daley Note for more information about DeLa Express.

Flows – Freeport LNG feedgas volumes have fallen to near zero in pipeline samples since April 11, the second unexplained outage to occur this year at the Texas liquefaction facility.

It is unclear whether the latest outage at Freeport will be extended. The company reported another trip at Train 3 in a filing with the Texas Commission on Environmental Quality (TCEQ), citing an issue with the ventilation flow meter.

Pipeline deliveries to Freeport LNG fell by over 0.5 Bcf/d in the second half of January following electrical issues caused by Winter Storm Heather. The company reported the motors driving the refrigeration compressors in Train 3 needed replacement, and expected the train to be offline through the last week of February. In early March, another train went offline. Freeport announced at the time that it expects to continue maintenance work through May.

Flows – East Daley’s ArkLaTex Basin pipe sample has fallen nearly 2 Bcf/d over two months, from 12.9 Bcf/d in February to 11.0 Bcf/d in the latest week ending April 14.

The decline in the Haynesville sample has been steep though expected after producers guided to deferred production earlier this year. Chesapeake (CHK) offered the most detailed guidance, laying out plans to slow the start-up of new wells and to drop a rig and frac crew in the Haynesville.

CHK said it plans to spend $670MM to maintain productive capacity at around 1.18 Bcf/d in the Haynesville. But the producer said actual gas deliveries would drop sharply by the end of 2024, estimating a 30% quarterly decline in 4Q24 vs 4Q23.

Ahead of the pending merger with CHK, Southwestern Energy (SWN) did not provide guidance in its 4Q23 earnings release, but East Daley assumes the company will follow a similar production plan to CHK. In fact, sample flows provide evidence of this already.

Based on East Daley’s rig allocation data, Southwestern continues to operate 7 rigs in the ArkLaTex, with 6 rigs on DT Midstream’s (DTM) Blue Union gathering system. While nearly every system sample in the Hayneville is trending downwards, Blue Union’s sample has shown the sharpest decline, dropping by -335 MMcf/d over the last two months.

The trend in Blue Union sample suggests that while SWN continues to drill, the E&P is likely building inventory of drilled but uncompleted wells (DUCs), or is completing wells and deferring turn-in-lines. Similarly, Energy Transfer’s (ET) Enable Haynesville system is down 273 MMcf/d and its major drillers are CHK and SWN.

Storage – The Energy Information Administration (EIA) reported a 24 Bcf injection into working gas for the week ending April 5 as the market kicks off the 2024 injection season. The latest EIA report was bearish compared to consensus estimates for a 14 Bcf injection.

Traders expect EIA to report a 52 Bcf injection in its survey for the April 12 week, according to a survey by The Desk. EIA reported a 61 Bcf injection for the same week in 2023, and the 5-year average for the week is also a 61 Bcf injection.

Working gas inventories currently total 2,283 Bcf, in line with East Daley’s forecast in the monthly Macro Supply and Demand Forecast. The surplus to the 5-year average totals 633 Bcf, while the surplus to last year stands at 435 Bcf.

For April, East Daley expects storage injections to fall below the 5-year average as the impact of sub-$2/MMBtu prices tighten the market. In the latest Macro Supply and Demand Forecast, we model inventories at 2,480 Bcf by the end of April, meaning the 5-year surplus would fall to 580 Bcf. While this is encouraging from a price perspective, our yield curve indicates that Henry Hub cash prices should remain below $2.00/MMBtu in the near term.

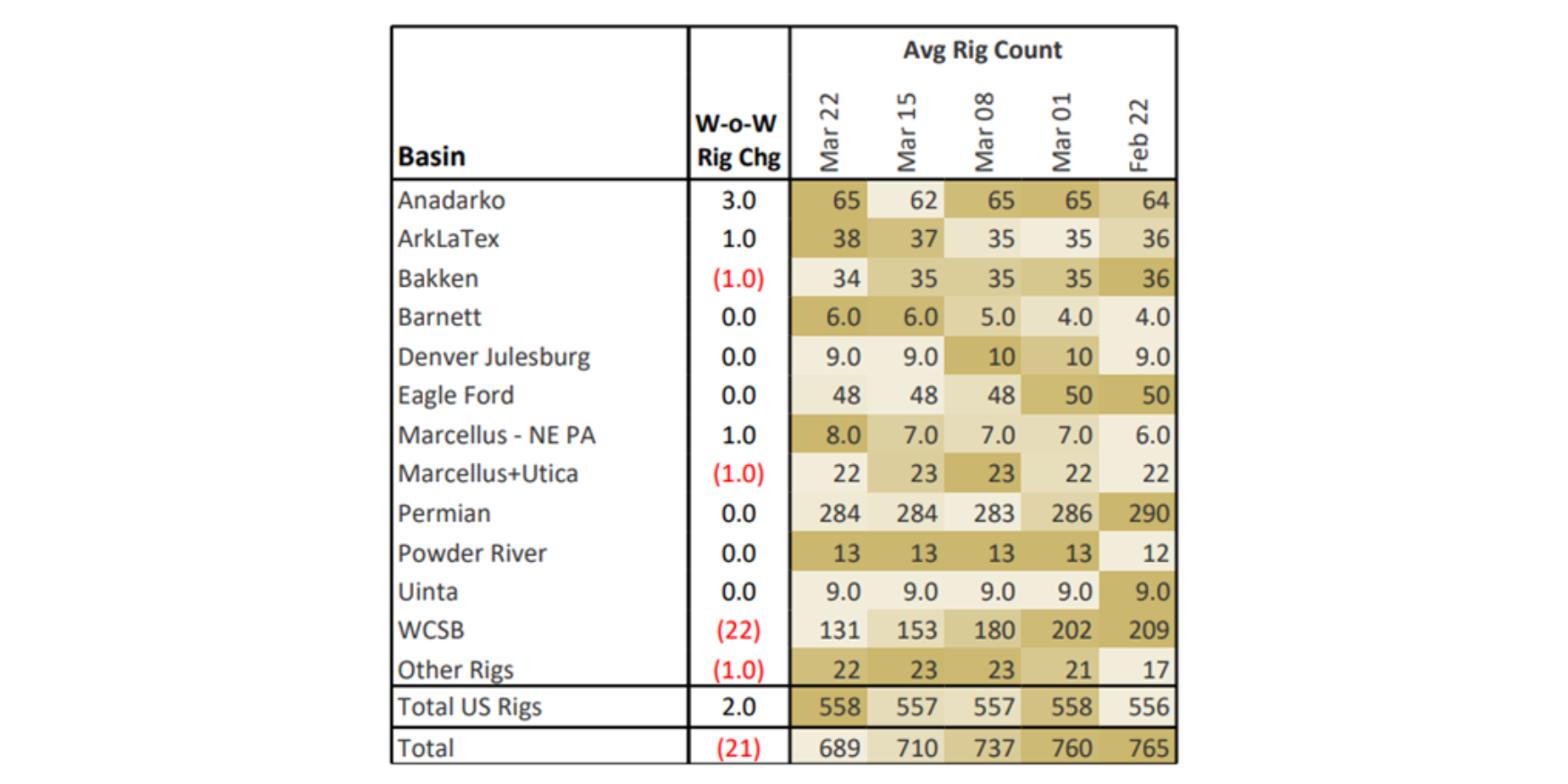

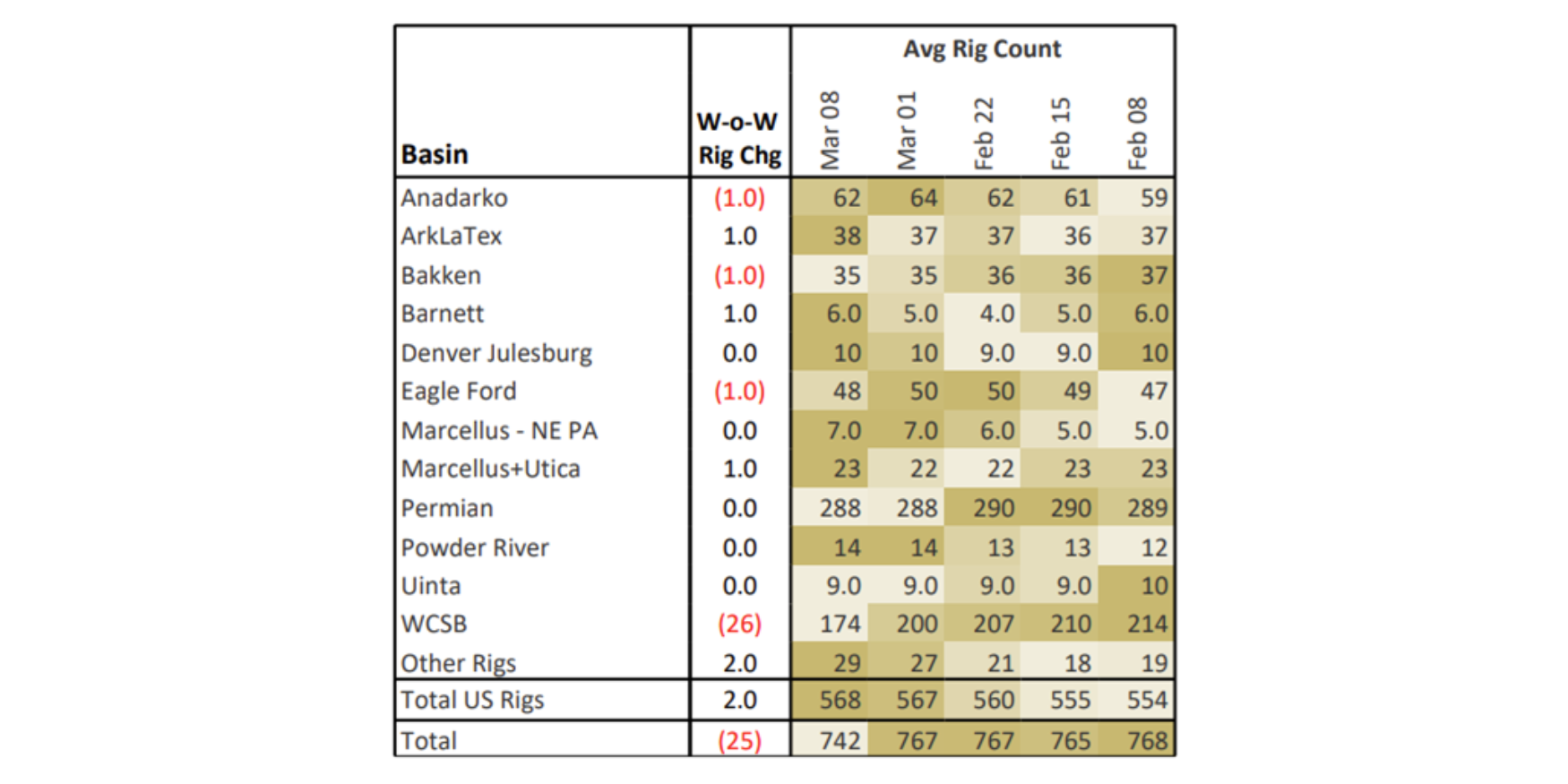

Rigs - The US rig count decreased by 3 W-o-W to bring the total rig count to 587 for the March 31 week. The Eagle Ford, DJ and Powder River basins each gained 1 rig. The Permian lost 3 rigs and the Bakken is down 2 rigs.

On the midstream side, ONEOK (OKE) is down 2 rigs with losses on its Bakken and Anadarko systems. Kinder Morgan (KMI) lost 2 rigs on its Bakken and Eagle Ford systems. Targa Resources (TRGP) gained 4 rigs on its Permian and Eagle Ford systems. Equitrans Midstream (ETRN) is up 1 rig on its Pennsylvania Utica system.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.