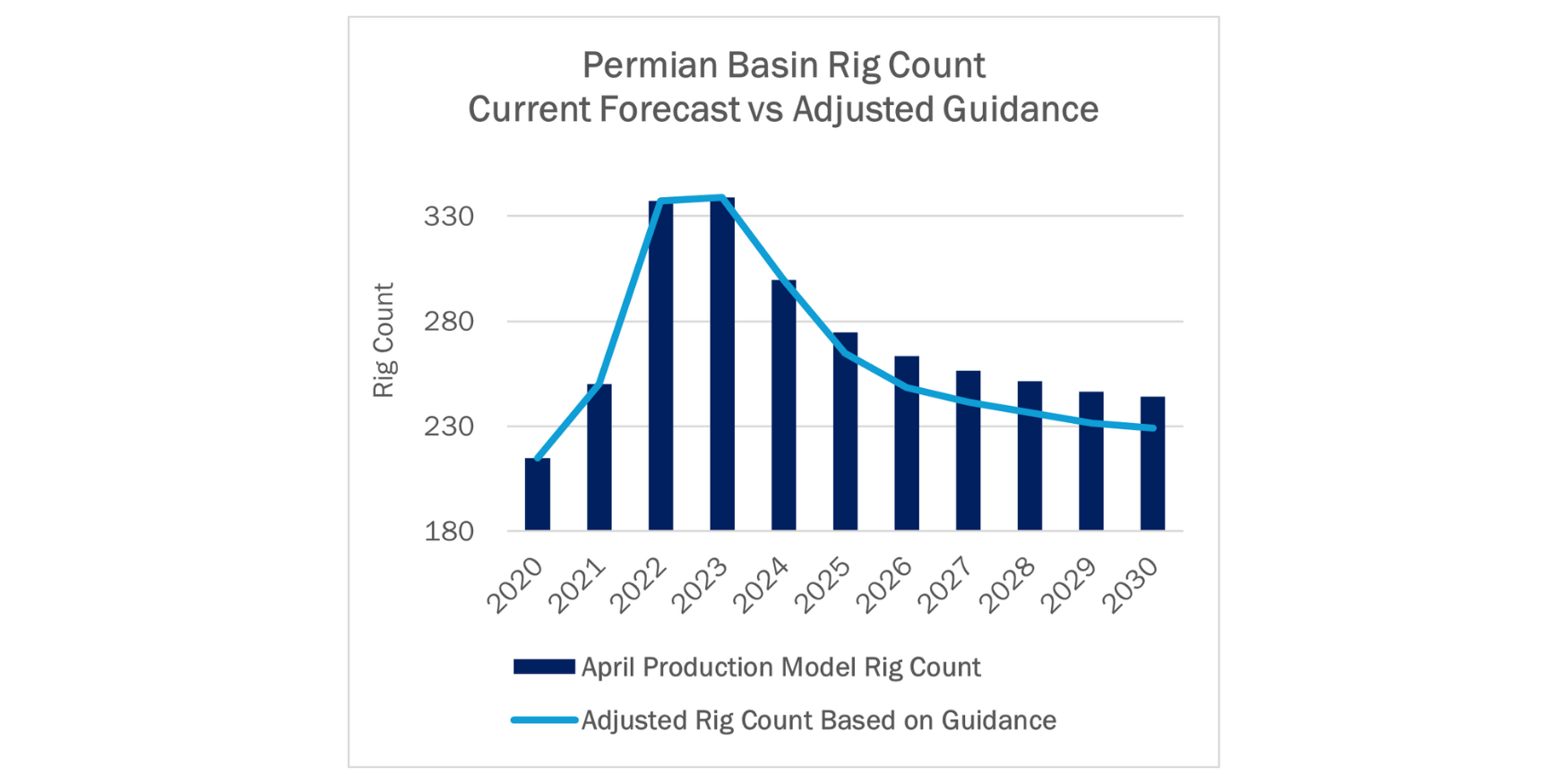

After years of steady gains, the Permian Basin is entering a more tempered growth phase as producers recalibrate spending plans. Several intend to pull back on drilling activity and have revised guidance lower after the recent drop in oil prices to $60/bbl.

Diamondback (FANG) set the tone for 1Q25 earnings updates, trimming its 2025 capital budget by $400MM and unveiling plans to drop 3 rigs and a frac crew from the Permian in 2Q25. Management made it clear: growth is viable at $60/bbl WTI, but anything below that price level puts the basin in maintenance mode — with potential for activity to stall around $50 WTI.

Coterra Energy (CTRA) followed suit, dropping its Permian guidance from 10 to 7 rigs and lowering capex to $2.0–2.3B. The producer has left the door open for deeper cuts if prices weaken further. Devon Energy (DVN) surprised to the upside, beating oil guidance thanks to strong Delaware performance. Still, DVN shaved $100MM off its capital plan and doubled down on a $1B optimization strategy to boost free cash flow without sacrificing output.

EOG Resources (EOG) reported $1.3B in free cash flow and production above forecasts, but also reduced capex guidance by $200MM. Even Matador Resources (MTDR) is tapping the brakes. The Delaware-focused producer plans to drop 1 rig mid-year, citing a need for discipline even as its capital guidance holds steady for now.

Taken together, the updates tell a cohesive story: the Permian is no longer on a breakneck growth trajectory. Instead, producers are embracing capital discipline in a $60/bbl price environment with more downside risk.

Moderating activity will inevitably ripple through the G&P landscape. Systems that have seen consistent volume growth may now face slower ramps or even volume declines. Infrastructure developers and midstream operators will need to reassess assumptions tied to basin-level growth and reoptimize for a flatter profile in 2025.

This is where East Daley Analytics’ Producer to System dashboard becomes a powerful tool. The database in Energy Data Studio helps bridge the gap between upstream activity and midstream exposure by showing how changes to production guidance directly connect to individual G&P systems.

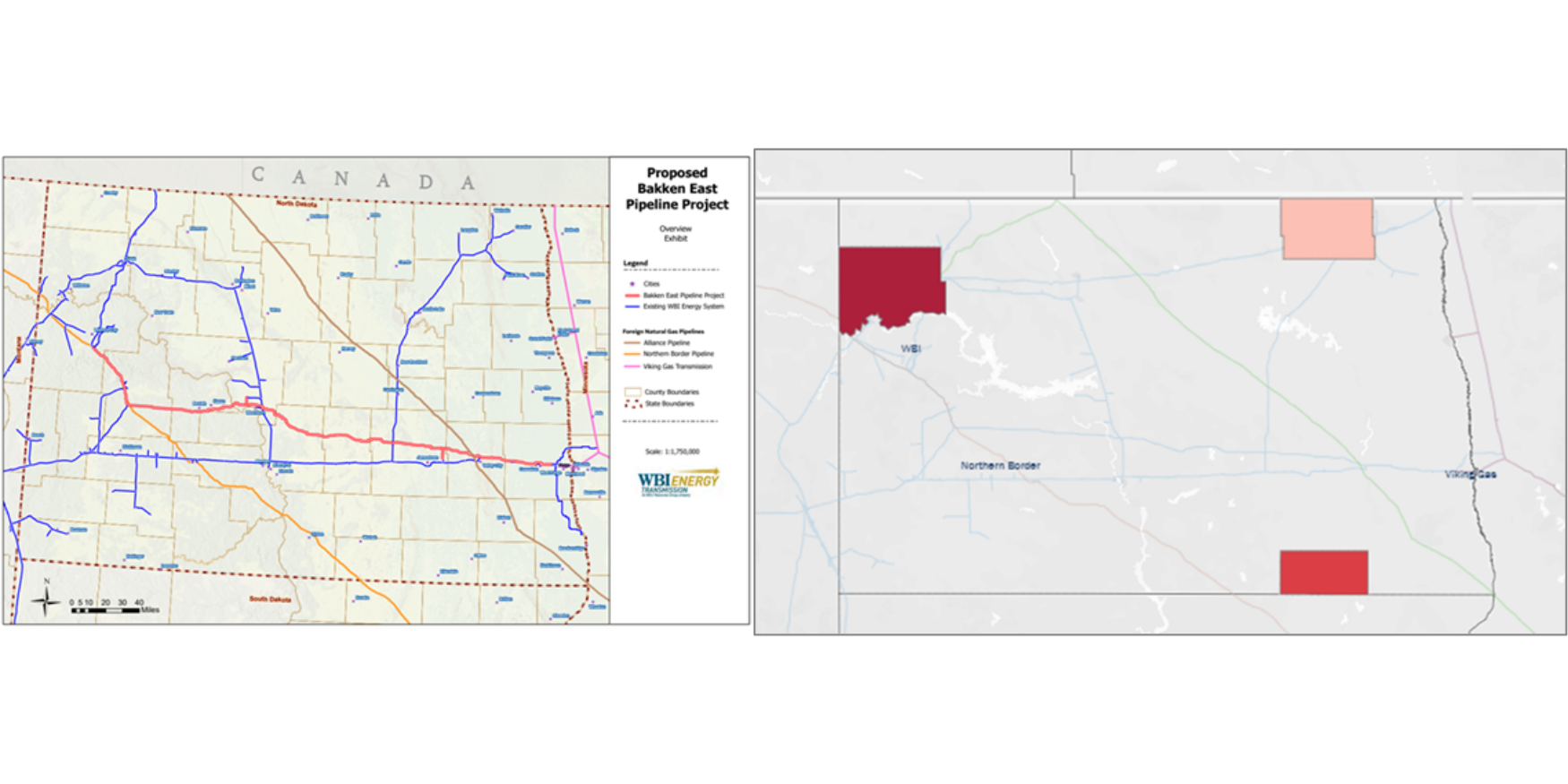

Diamondback, for example, did not specify where it intends to cut rigs, but the Producer to System dashboard for FANG (pictured above) shows its core operations are in the Midland Basin, particularly in Martin, Midland and Howard counties. These areas are likely to feel the brunt of the cutbacks. FANG delivers gas to G&P systems in the area owned by Enterprise (EPD), ONEOK (OKE) and Energy Transfer (ET), according to the dashboard, so these assets could be vulnerable to a slowdown in volumes.

Reach out to East Daley to learn more about the Producer to System dashboard. – Maria Paz Urdaneta Tickers: CTRA, DVN, EOG, EPD, ET, FANG, MTDR, OKE.

Data Center Demand Monitor - Available Now!

Introducing Data Center Demand Monitor by East Daley Analytics. This is your go-to source for tracking data center projects and demand. We monitor and visualize nearly 300 US data center projects. Use Data Center Demand Monitor to forecast demand, identify pipeline corridors and track data center projects. — Request your demo now of the Data Center Demand Monitor!

Get the FERC Intrastate Pipeline Data

Introducing East Daley’s latest data file: FERC 549D Intrastate Contract Data. This new offering delivers contract shipper data for intrastate pipelines — scrubbed and ready to use. Use the 549 data to identify which intrastate pipelines have available capacity, understand pipeline rate structures, gain insights into shippers, and spot contract cliffs and opportunities for higher rate renewals. Reach out to East Daley to learn more.

The Daley Note

Subscribe to The Daley Note for energy insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices and EDA research likely to affect markets in the short term.

-1.png)