Despite a $10/bbl correction in oil prices, the rush is still on to build natural gas processing in the Permian Basin. Developers have used 1Q25 earnings to announce several new projects, and companies remain bullish as they position to capture value as close to the wellhead as possible.

Vaquero Midstream announced a new 200 MMcf/d cryogenic plant in the Delaware Basin. That project includes a 70-mile looping line and is expected to begin service by 1Q26. Meanwhile, Phillips 66 (PSX) is moving forward with 300 MMcf/d in new plant expansions in the Delaware, due to start in 1Q27.

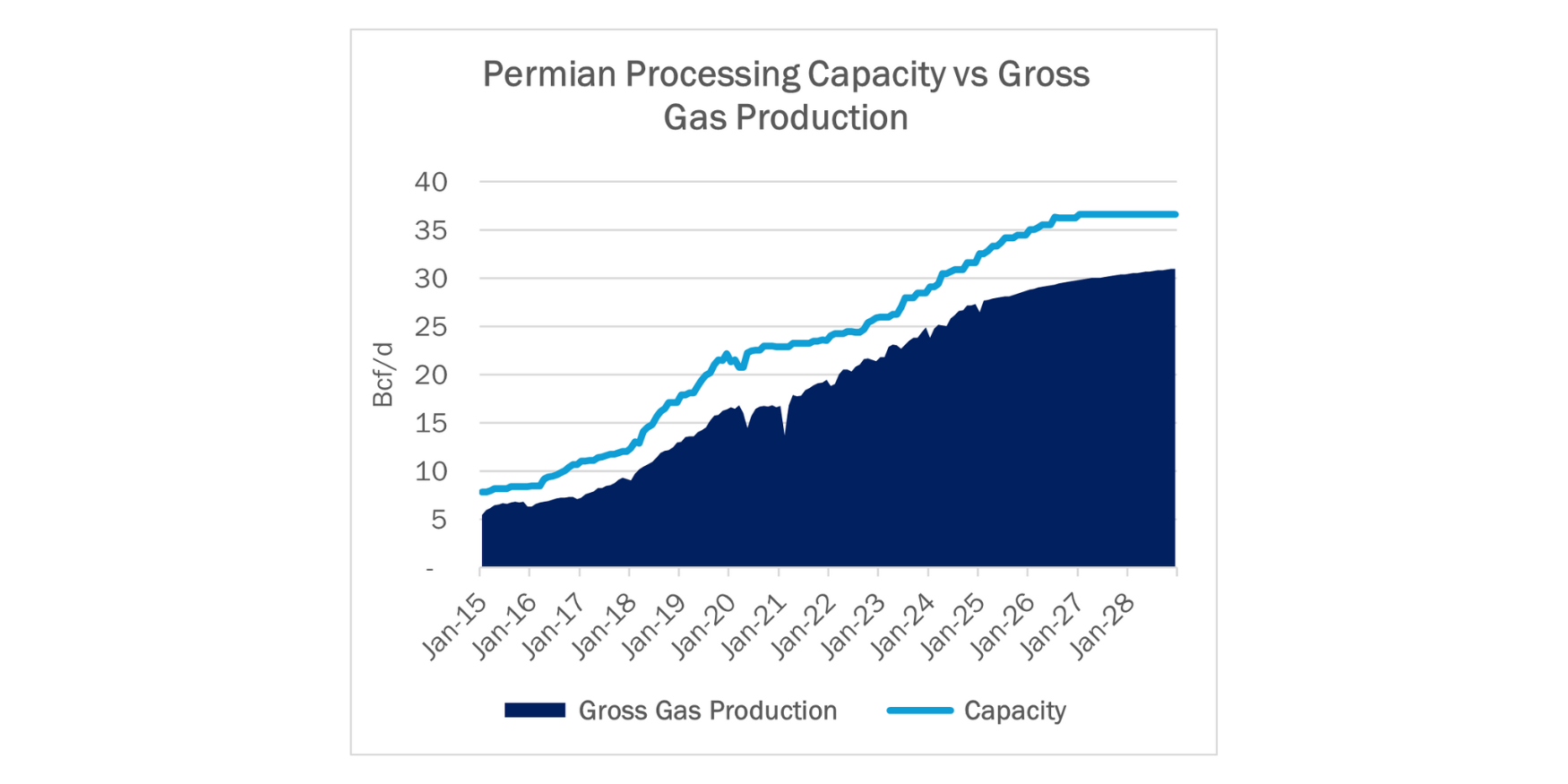

By YE26, East Daley forecasts nearly 5.2 Bcf/d of additional gas processing capacity across the Permian compared to 2024. In our latest model updates, Permian gross gas production still grows 2.1 Bcf/d (8%) by 2025 and 1.3 Bcf/d (5%) by 2026 vs the 2024 average, even in the face of $60 WTI prices.

Two distinct groups have emerged in the race to capture volumes. Integrated midstream companies like Enterprise Products (EPD) and Targa Resources (TRGP) are aggressively expanding their footprints to secure NGL barrels, not just at the wellhead but across the entire value chain: gathering, processing, transportation, storage and export.

Meanwhile, a mix of smaller companies including Brazos Midstream, Durango Midstream and Vaquero, along with non-integrated public companies like ONEOK (OKE), Western Midstream (WES) and MPLX, are also investing in new capacity. These companies could eventually become acquisition targets for the larger, integrated players looking to consolidate their hold on the market.

EPD (21% share) and TRGP (39% share) alone account for more than half of the announced new gas processing capacity. The remainder of the new capacity comes from a mix of private and smaller public operators that continue to compete for volumes in a crowded landscape.

Targa reported its Permian G&P volumes grew 14% in 1Q25 from 1Q24, and anticipates volume growth and stable rig activity despite oil price volatility. TRGP said its newest plant, Pembrook II in the Midland Basin, will go into service ahead of schedule in 3Q25.

With the development surge, EDA’s analysis suggests that G&P capacity will remain ahead of supply growth for now. Potential constraints are more likely to emerge further downstream, a risk that TRGP and EPD appear willing to accept in exchange for securing critical volumes for their NGL transport and export networks.

In addition to the EPD and TRGP projects, the Vaquero and PSX announcements show competition is intensifying elsewhere in the Permian. For Phillips 66, the 300 MMcf/d expansions will reinforce its downstream NGL position following the $2.2B acquisition of EPIC. The development highlights a broader trend: midstream companies are not simply racing to keep up with production, but are building to dominate future flows from the wellhead to global markets. – Maria Paz Urdaneta Tickers: EPD, MPLX, OKE, PSX, TRGP, WES.

Data Center Demand Monitor - Available Now!

Introducing Data Center Demand Monitor by East Daley Analytics. This is your go-to source for tracking data center projects and demand. We monitor and visualize nearly 300 US data center projects. Use Data Center Demand Monitor to forecast demand, identify pipeline corridors and track data center projects. — Request your demo now of the Data Center Demand Monitor!

Get the FERC Intrastate Pipeline Data

Introducing East Daley’s latest data file: FERC 549D Intrastate Contract Data. This new offering delivers contract shipper data for intrastate pipelines — scrubbed and ready to use. Use the 549 data to identify which intrastate pipelines have available capacity, understand pipeline rate structures, gain insights into shippers, and spot contract cliffs and opportunities for higher rate renewals. Reach out to East Daley to learn more.

The Daley Note

Subscribe to The Daley Note for energy insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices and EDA research likely to affect markets in the short term.

-1.png)