Executive Summary: Rigs: The total US rig count decreased by 11 during the week of April 27 to 548. Infrastructure: Kinder Morgan (KMI) is still months out from starting the conversion of Double H Pipeline from crude oil to NGL service, yet new data suggests some Bakken shippers have already moved on. Storage: East Daley expects a 4.2 MMbbl injection from commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 9.

Rigs:

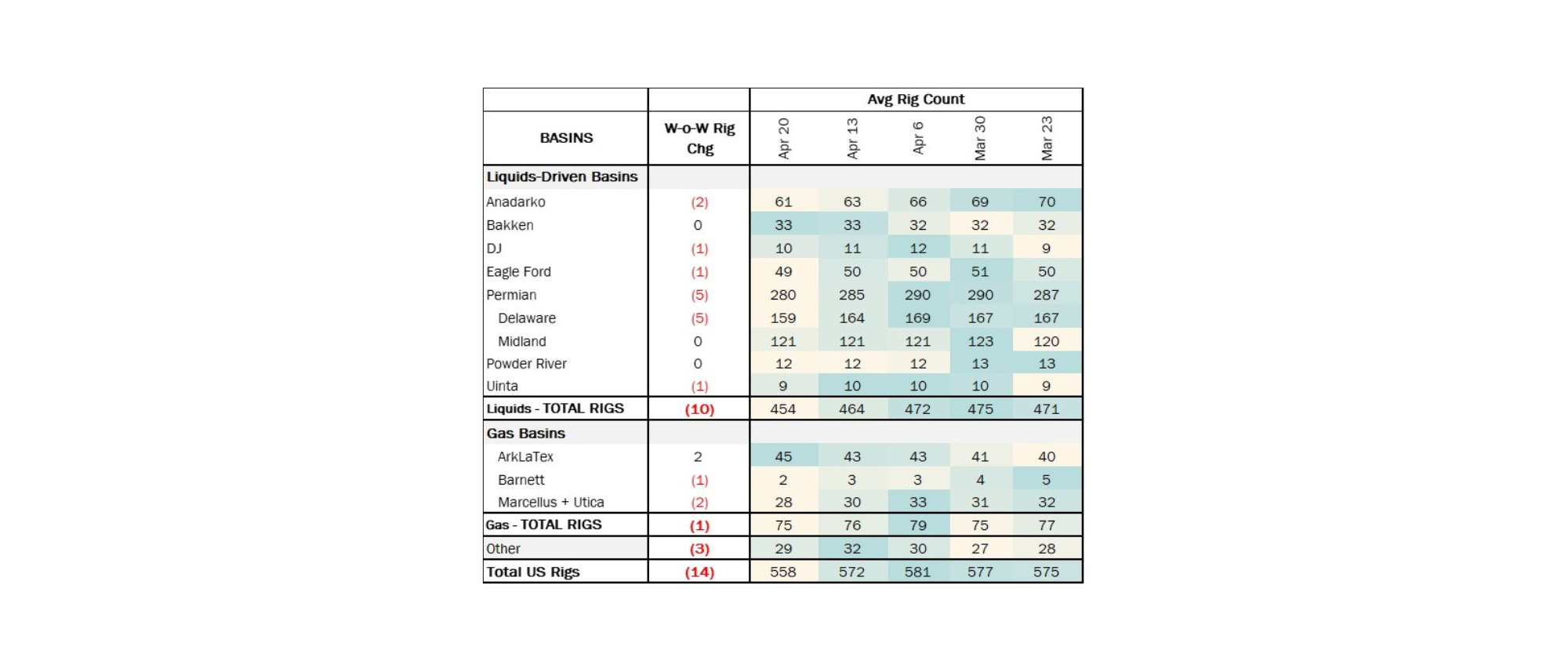

The total US rig count decreased by 11 during the week of April 27 to 548. Liquids-driven basins decreased by 7 W-o-W from 452 to 445.

- Permian-Midland (-4): ConocoPhillips, Diamondback Energy, Medders Oil Co., FourPoint Energy, LLC

- Bakken (-2): ConocoPhillips, Silver Hill Energy

- Eagle Ford (-1): SM Energy

Infrastructure:

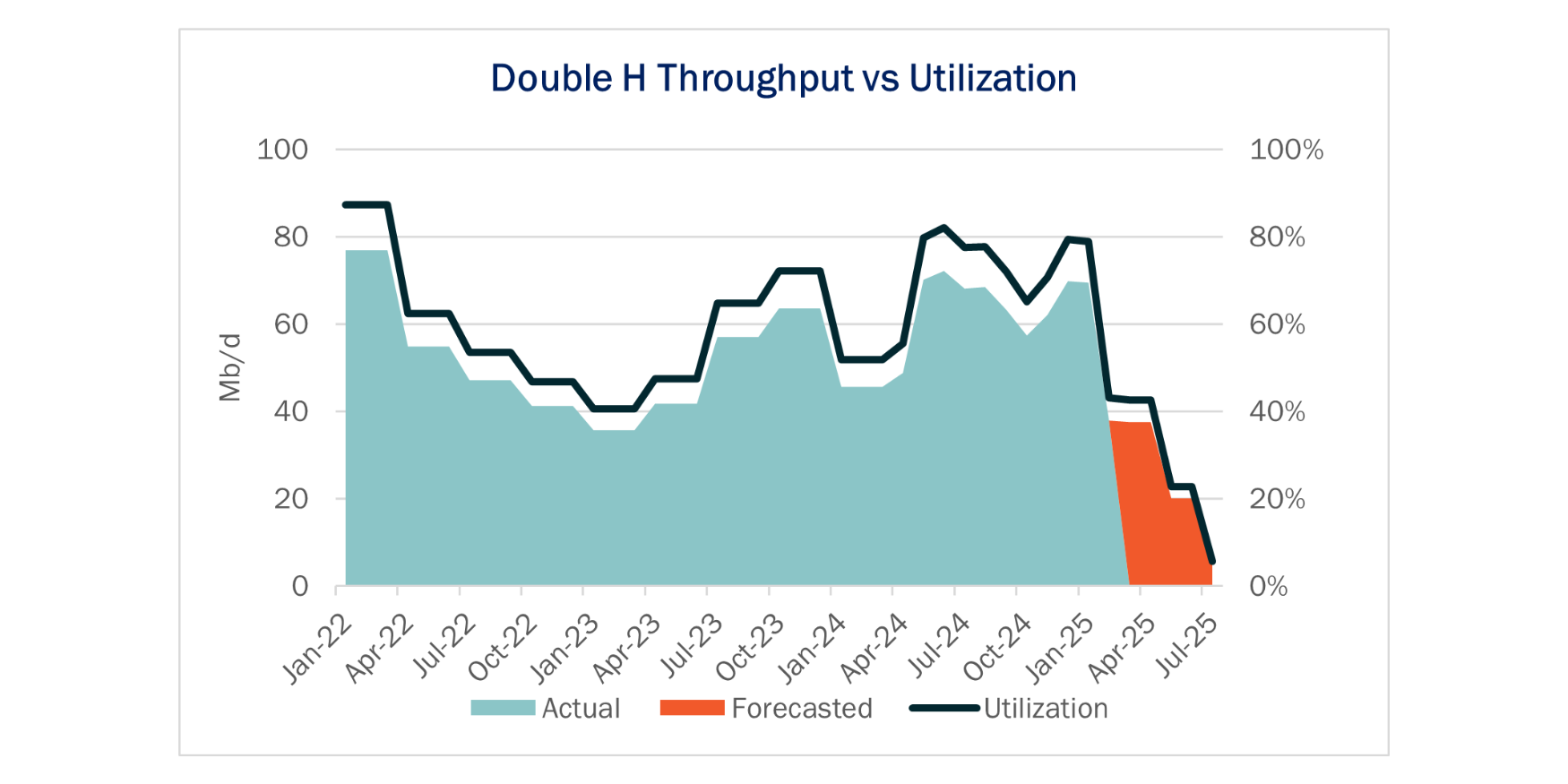

Kinder Morgan (KMI) is still months out from starting the conversion of Double H Pipeline from crude oil to NGL service, yet new data suggests some Bakken shippers have already moved on.

In the latest Crude Hub Model and Bakken-Guernsey-DJ Crude Oil S&D report, East Daley highlighted a significant M-o-M decrease in Double H throughput into the Guernsey market. Data filed with North Dakota regulators indicates throughput decreased ~32 Mb/d from January to February ’25, suggesting contracts are beginning to roll off and that the pipeline will struggle to retain the ~76% utilization it has maintained since May ’24. We now forecast Double H will discontinue oil deliveries post-July ’25, two months earlier than our previous forecast of Sept ’25 (see figure).

Several competing pipelines have held open seasons for Bakken, Guernsey and Denver-Julesburg (DJ) crude egress, shortening the timeline for Double H. Notably, Bridger and Pony Express pipelines announced an open season for joint incentive tariff rates on February 14, and Pony Express began an open season from its Colorado origins on March 7. Furthermore, effective April 1, KMI published a cancellation notice for its Double H joint tariff with Pony Express.

East Daley believes Bridger and Dakota Access Pipeline (DAPL) will be the beneficiaries of Double H’s exit. We expect Bridger will absorb ~50% of the Double H throughput while DAPL will have the opportunity to attract the remaining ~30 Mb/d based on tariff rates and end market. Operated by Energy Transfer (ET), DAPL can move barrels past PADD 2 refiners to the Houston export market and potentially into Louisiana via Bayou Bridge.

With Double H service nearing a close, producers can participate in these open seasons – or partner with a marketer – to secure capacity on favorable routes and tariffs. Those with confirmed capacity agreements are better positioned to preserve or enhance margins, while those without may face higher costs, rerouted flows, or exposure to tighter regional differentials.

Editor's Note: Since publishing this blog, February '25 flow data for Double H Pipeline was revised up to 67.9 Mb/d from 37.8 Mb/d originally. EDA continues to forecast oil flows will cease on Double H starting July '25, though we have slowed the near-term decline with the updated data. (May 27, 2025)

Storage:

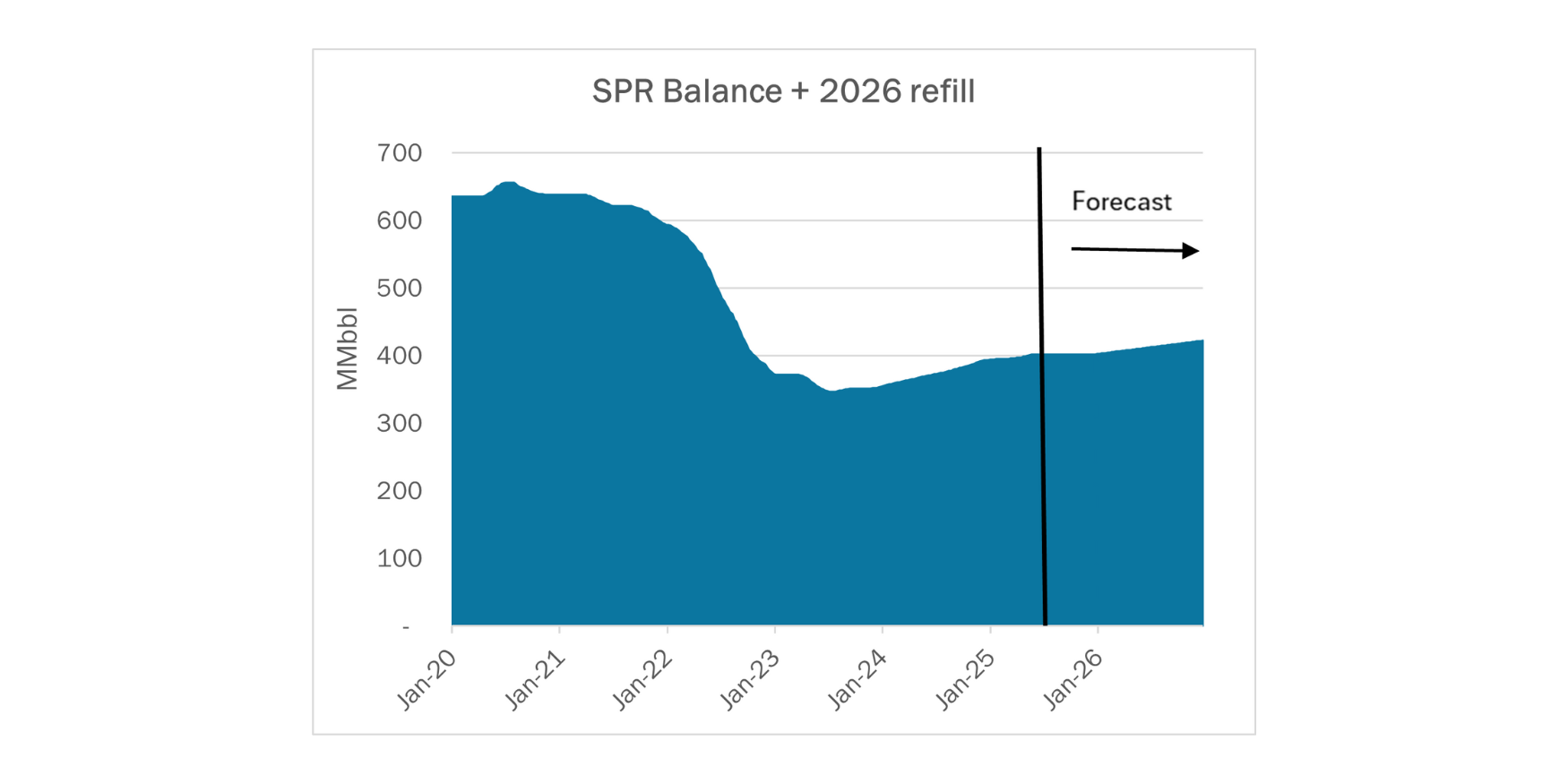

East Daley expects a 4.2 MMbbl injection from commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 9. We expect total US stocks, including the SPR, will close at 842 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, decreased 2.0% W-o-W across all liquids-focused basins. Samples increased 7.3% in the Gulf of Mexico and 4.37% in the Eagle Ford and decreased 1.5% in the Permian and 2.4% in the Williston Basin. The Rockies and the Gulf of Mexico have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

We expect US crude production to be 13.4 MMb/d. According to US bill of lading data, US crude imports increased to 6.2 MMb/d. More than 60% of the supply originated from Canadian pipelines and vessels into the US, with the remainder largely coming from vessels carrying crude from Mexico and Argentina.

As of May 2, there was ~752 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude input into refineries to increase, coming in at 16.4 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 20 vessels loaded for the week ending May 10 and 20 the prior week. EDA expects US exports to be 2.95 MMb/d.

The SPR awarded contracts for 6.0 MMbbl to be delivered To Choctaw February –May 2025 and 2.4 MMbbl to be delivered to Bryan Mound April – May 2025. The SPR has 399 MMbbl in storage as of May 9, 2025.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

SCM Crude, LLC An off-spec penalty was established applicable to any crude barrels tendered at Wink Terminal exceeding the tariff’s Mercaptans specification of equal to or less than 75 ppm. FERC No 1.25.0 IS25-307 Effective May 1, 2025.

White Cliffs Pipeline L.L.C. A new incentive rate was established for movements from Platteville, CO to Cushing, OK which requires an executed TSA. The joint carriers were also updated reflecting Energy Transfer’s corporate organization. FERC No 4.19.0 IS25-299 Effective May 1, 2025.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)