Executive Summary: Rigs: The total US rig count decreased by 6 during the week of April 13 to 571. Infrastructure: Supply growth from the Permian Basin will bring more barrels to Gulf Coast terminals this year, as well as increased pipeline congestion. Storage: East Daley expects a 6.6 MMbbl withdraw from commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending April 25.

Rigs:

The total US rig count decreased by 6 during the week of April 13 to 571. Liquids-driven basins decreased by 7 W-o-W from 470 to 463.

- Permian (-5):

- Delaware (-4): Permian Resources, Occidental Petroleum, EOG Resources, Chevron

- Midland (-1): Occidental Petroleum

- Anadarko (-1): American Warrior

- DJ (-1): Chevron

- Eagle Ford (-1): Grit Oil & Gas Management

- Uinta (+1): Scout Energy Partners

Infrastructure:

Supply growth from the Permian Basin will bring more barrels to Gulf Coast terminals this year, as well as increased pipeline congestion. East Daley forecasts Permian crude oil production will increase 306 Mb/d from 2024 to 2025 averages, nearly all of which is destined for export docks.

The Permian barrel has direct and economic access to all US Gulf Coast export terminals other than Louisiana’s LOOP. With refinery demand relatively flat or slightly declining, these export terminals are critical to connecting supply growth to markets.

Today’s premiere export dock is the Enbridge Ingleside Energy Center (EIEC) in Corpus Christi. EIEC is the largest crude oil export terminal in North America, loading 25% of US Gulf Coast exports. In 2H24, EIEC loaded ~1.1 MMb/d (47%) of the ~2.42 MMb/d exported through Corpus Christi export docks.

Enbridge (ENB) could handle even more barrels at Ingleside but is held back by a lack of pipeline egress. EIEC is currently utilizing ~68% of its 1.6 MMb/d capacity, while total pipeline egress to Corpus docks is ~94% used, according to the Crude Hub Model. Enbridge is expanding Gray’s Oak Pipeline by 120 Mb/d in 2025, and EPIC Pipeline is likely to expand 300 Mb/d. These projects could allow utilization at EIEC to climb to as high as 90% (~1.45 MMb/d). Gibson Energy’s South Texas Gateway Export Terminal, also located in Ingleside Corpus Christi, is running at ~75% utilization (~600 Mb/d) and is another important player in the Corpus Christi market.

The Houston and Nederland market is fast approaching Corpus Christi’s dominance at 2.1 MMb/d of crude exports vs 2.4 MMb/d from Corpus. East Daley’s Crude Hub Model forecasts Houston export volumes to exceed Corpus Christi by 3Q25, largely due to pipeline egress constraints. Permian pipelines to Corpus Christi are ~94% utilized and will remain >90% filled after the Gray Oak expansion. Permian pipelines to Houston/Nederland markets have more ample room to grow at ~85% utilization currently. East Daley expects these pipelines to Houston/Nederland will remain at <90% utilization even while the Permian continues to grow.

Enterprise Products’ (EPD) Houston Ship Channel (HSC) dominates among Houston export terminals, exporting ~750 Mb/d in 2024. However, HSC has extraordinary growth potential with capacity of 2.184 MMb/d, plus ample pipeline egress to receive more barrels. EPD’s Midland-to-Echo I and III pipelines have direct access to HSC and are ~95% utilized. However, EPD is returning the Midland-to-Echo II Pipeline to crude service in 4Q25, adding 200 Mb/d of egress from the Permian to Houston.

ONEOK’s (OKE) Seabrook Export Terminal in Freeport, TX and Energy Transfer’s Houston Fuel Oil Terminal (HFOT) add another ~1.2 MMb/d of export capacity in the Houston market. Each terminal is moving ~220 Mb/d.

As the Permian continues to grow, East Daley models adequate capacity from export terminals in the Crude Hub Model. However, we believe the high pipeline utilization will cause congestion and lead to the MEH benchmark widening out. Congestion in the bay to export terminals will also likely increase and lead to higher reverse lightering charges.

Storage:

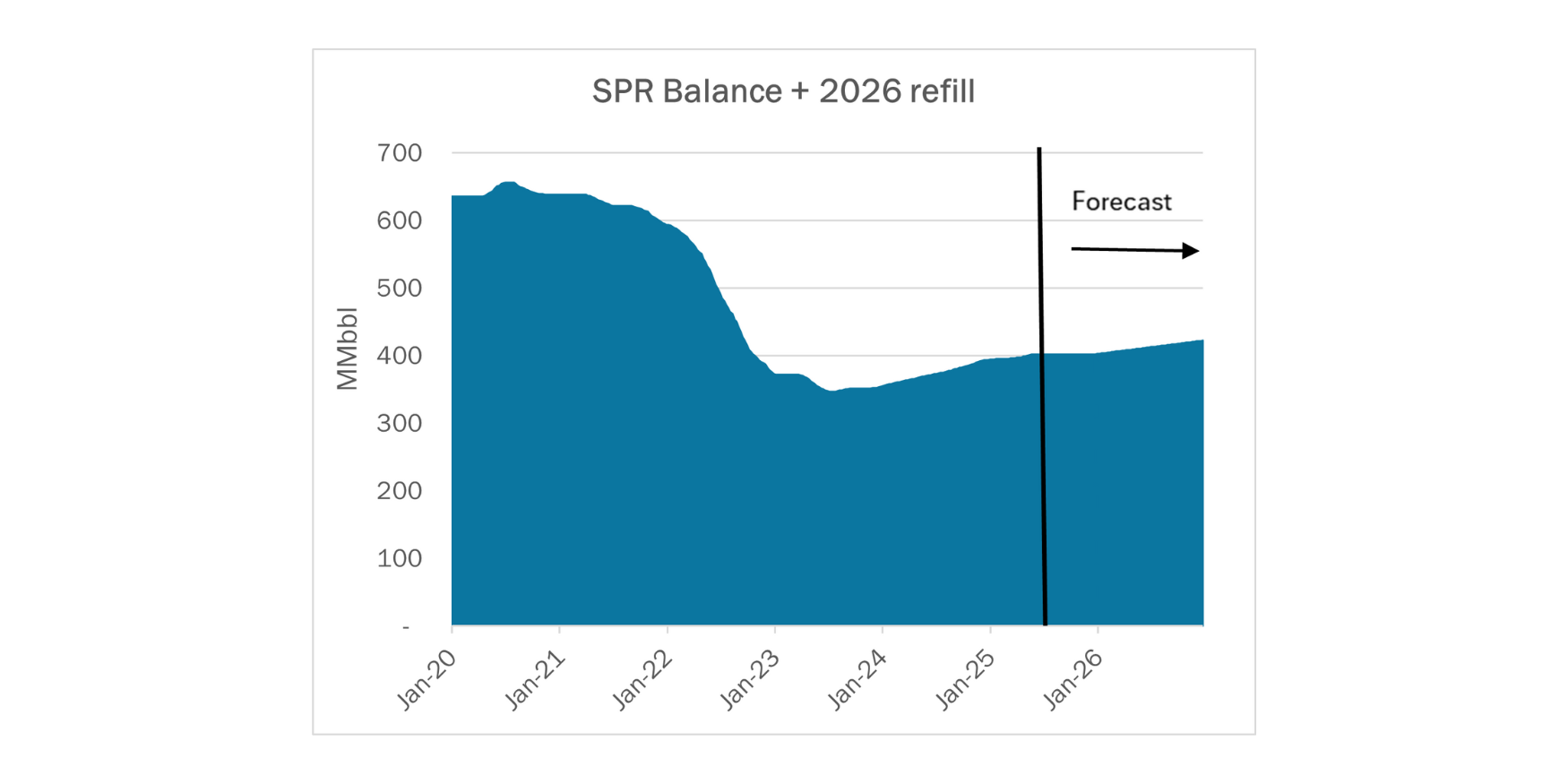

East Daley expects a 6.6 MMbbl withdraw from commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending April 25. We expect total US stocks, including the SPR, will close at 834 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, decreased 0.5% W-o-W across all liquids-focused basins. Samples increased 2.96% in the Williston Basin and 2.8% in the Permian Basin and decreased 3.4% in the Eagle Ford and 6.5% in Gulf of Mexico. The Rockies and the Gulf of Mexico have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

We expect US crude production to be 13.46 MMb/d. According to US bill of lading data, US crude imports increased to 5.6 MMb/d. More than 60% of the supply originated from Canadian pipelines and vessels into the US, with the remainder largely coming from vessels carrying crude from Mexico and Nigeria.

As of April 25, there was ~375 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude input into refineries to increase, coming in at 16.15 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast stayed flat W-o-W. There were 25 vessels loaded for the week ending April 25 and 25 the prior week. EDA expects US exports to be 4.2 MMb/d.

The SPR awarded contracts for 6.0 MMbbl to be delivered To Choctaw February –May 2025 and 2.4 MMbbl to be delivered to Bryan Mound April – May 2025. The SPR has 397 MMbbl in storage as of April 18, 2025.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

Express Pipeline LLC. Initial committed rates were established through an open season process for the Express Canada pipeline, which had contracted capacity that became available when the underlying contracts for the capacity expired. FERC No 167.29.0 IS25-261 (filed February 25, 2025) Effective April 1, 2025.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)