Executive Summary: Rigs: The total US rig count decreased by 12 during the week of May 11 to 531. Infrastructure: The Permian Basin continues to show growth potential, but the market is entering a more measured phase. Storage: East Daley expects a 3.9 MMbbl injection from commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 23.

Rigs:

The total US rig count decreased by 12 during the week of May 11 to 531. Liquids-driven basins decreased by 14 W-o-W from 439 to 425.

- Permian-Midland (-7): Diamondback Energy, Oxy, Blackbeard Operating LLC, Highpeak Energy, SOGC LLC, Continental Resources, Texland Petroleum

- Permian-Delaware (-1): Oxy

- Anadarko (-2): Sanguine Gas Exploration, Packard Energy

- Bakken (-4): Continental Resources, Chord Energy, Koda Resources, ConocoPhillips

Infrastructure:

The Permian Basin continues to show growth potential, but the market is entering a more measured phase. In our base case scenario, East Daley expects slower growth than in past years, but still with upside — especially for gas production.

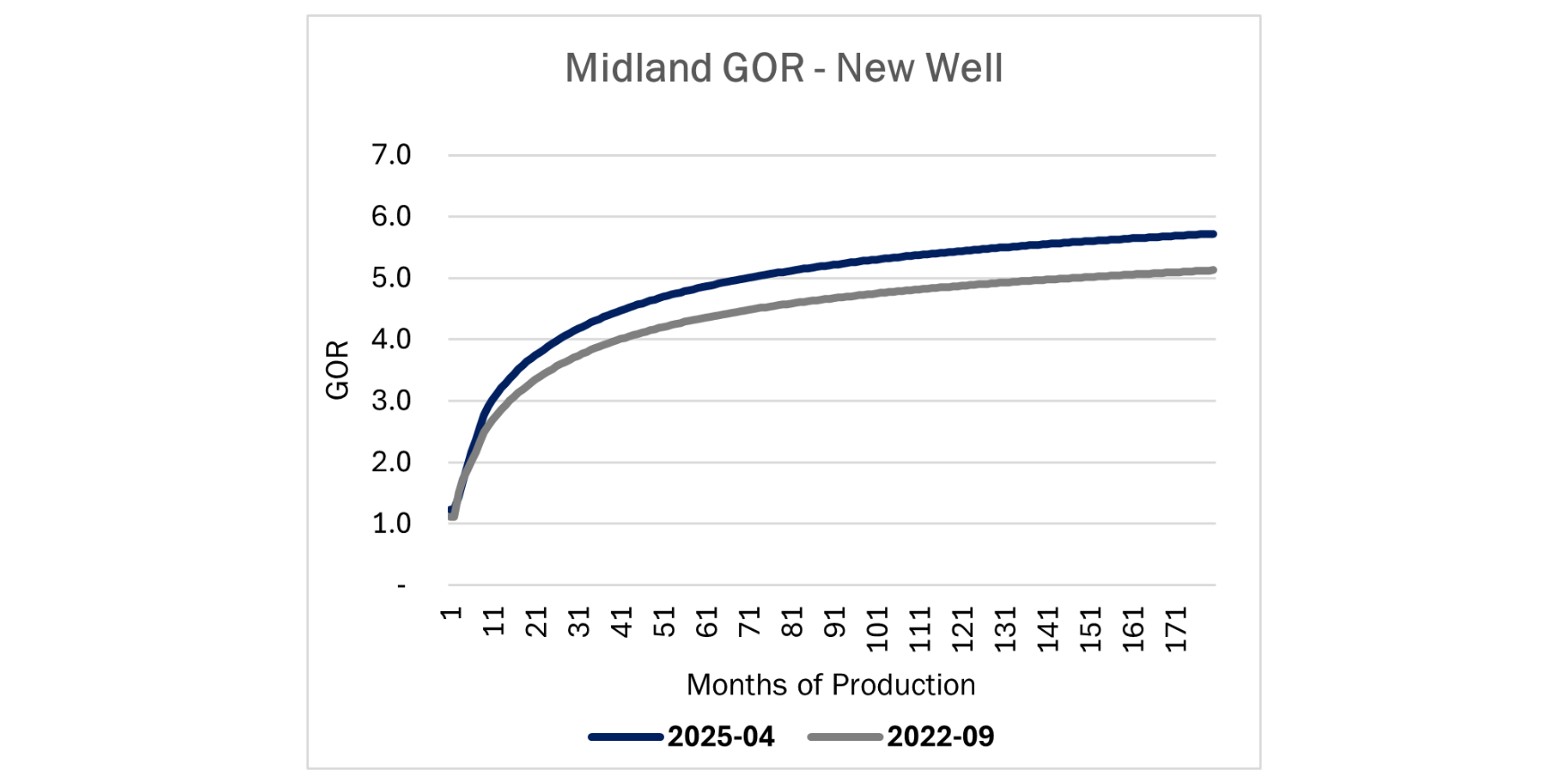

Gas-to-oil ratios (GOR) in the Permian have been climbing steadily over the last several years, supporting our optimism on gas supply. As wells age and operators shift their development strategies, more gas is coming out with the oil, particularly in the Midland Basin.

That said, midstream companies are still feeling optimistic. Most of the big names, like Targa (TRGP) and Enterprise (EPD), have kept their guidance intact. Their confidence is tied to new processing plants coming online and a backlog of wells expected to be turned in line in 2H25. Regarding price signals, there’s a general view that WTI in the $50/bbl range keeps the Permian in “maintenance mode.” If prices drop closer to the low $50s, we’d likely see production fall off, especially from smaller operators running 2 or fewer rigs. Those companies tend to be more sensitive to price swings and could start cutting back quickly. Rising GORs will still support gas production, but overall we’d likely see a pullback.

The second half of 2025 will be key. Drilled but uncompleted wells provide a lot of potential, but we’ll need to see how many are brought online. Our Permian Production Scenario Tool is built to adjust with the market and plug in your own assumptions — whether rig counts, pricing or well connection timing — to see how production might evolve in real time. With so much in flux, it’s a practical way to stay ahead of the curve and test how different outcomes could impact the basin’s trajectory.

Storage:

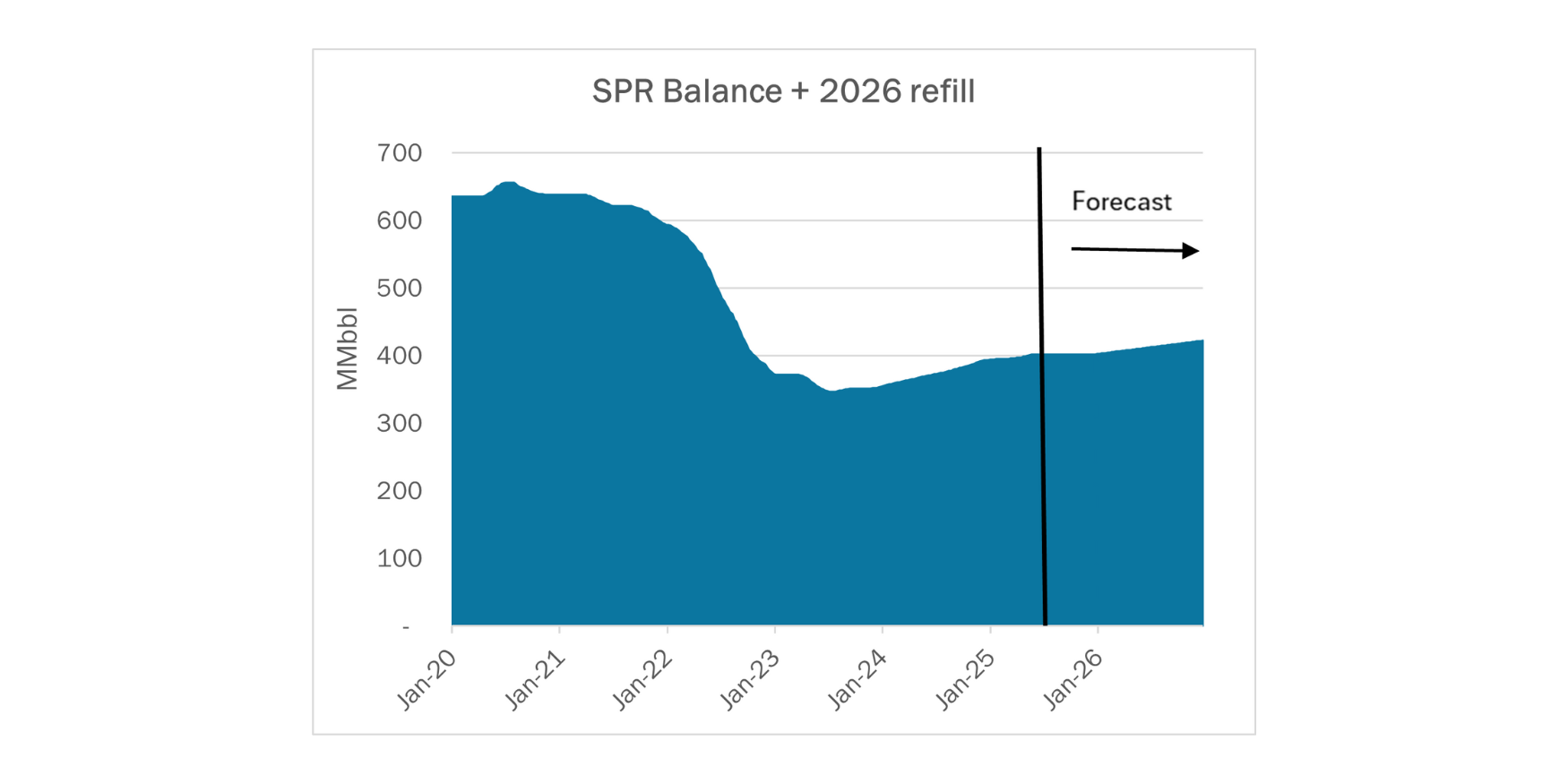

East Daley expects a 3.9 MMbbl injection from commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 23. We expect total US stocks, including the SPR, will close at 848 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, decreased .61% W-o-W across all liquids-focused basins. Samples increased 5% in the Eagle Ford and 1.75% in the Rockies and decreased 2.8% in the Williston Basin and 1.85% in the Permian Basin. The Rockies and the Gulf of Mexico have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

However, lower WTI prices near $60/bbl are starting to influence operator behavior. For example, Matador Resources (MTDR) said it would drop a rig and trim $100MM from its 2025 drilling budget. East Daley expects similar announcements ahead as producers start walking back their 2025 guidance. We don’t expect a collapse by any means, but a more cautious outlook where operators adjust rig counts and capital plans at the margin.

We expect US crude production to be 13.9 MMb/d. According to US bill of lading data, US crude imports increased to 6.8 MMb/d. More than 60% of the supply originated from Canadian pipelines and vessels into the US, with the remainder largely coming from vessels carrying crude from Mexico and Brazil.

As of May 23, there was ~818 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude input into refineries to decrease, coming in at 16.1 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast increased W-o-W. There were 27 vessels loaded for the week ending May 23 and 22 the prior week. EDA expects US exports to be 4.3 MMb/d.

The SPR awarded contracts for 6.0 MMbbl to be delivered to Choctaw February–May 2025 and 2.4 MMbbl to be delivered to Bryan Mound April–May 2025. The SPR has 400 MMbbl in storage as of May 16, 2025.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

Platte Pipe Line Company, LLC Terminaling services were added at Casper, WY for delivery to Frontier Aspen, LLC to accommodate shippers’ request. The rate was agreed to by at least one non-affiliated shipper. FERC No 4.6.0 IS25-312 Effective June 15, 2025.

Cheyenne Pipeline LLC The contract rates were canceled as they are no longer effective. FERC No 2.16.0 IS25-302 Effective June 10, 2025.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)