Executive Summary:

Infrastructure: Canada’s Trans Mountain Pipeline is weighing more expansions to boost crude exports from the Pacific coast.

Rigs: The total US rig count decreased during the week of May 25 to 532.

Storage: East Daley expects a 298 Mbbl injection into storage for the week ending June 7.

Rigs:

The total US rig count decreased during the week of May 25 to 532. Liquids-driven basins decreased by 5 W-o-W from 431 to 424.

- Permian (-3):

-

- Delaware (-2): Vital Energy, BP

-

- Midland (-1): Vital Energy

- Anadarko (-1): Downing-Nelson Oil

- Bakken (-1): Zarvona Energy

Infrastructure:

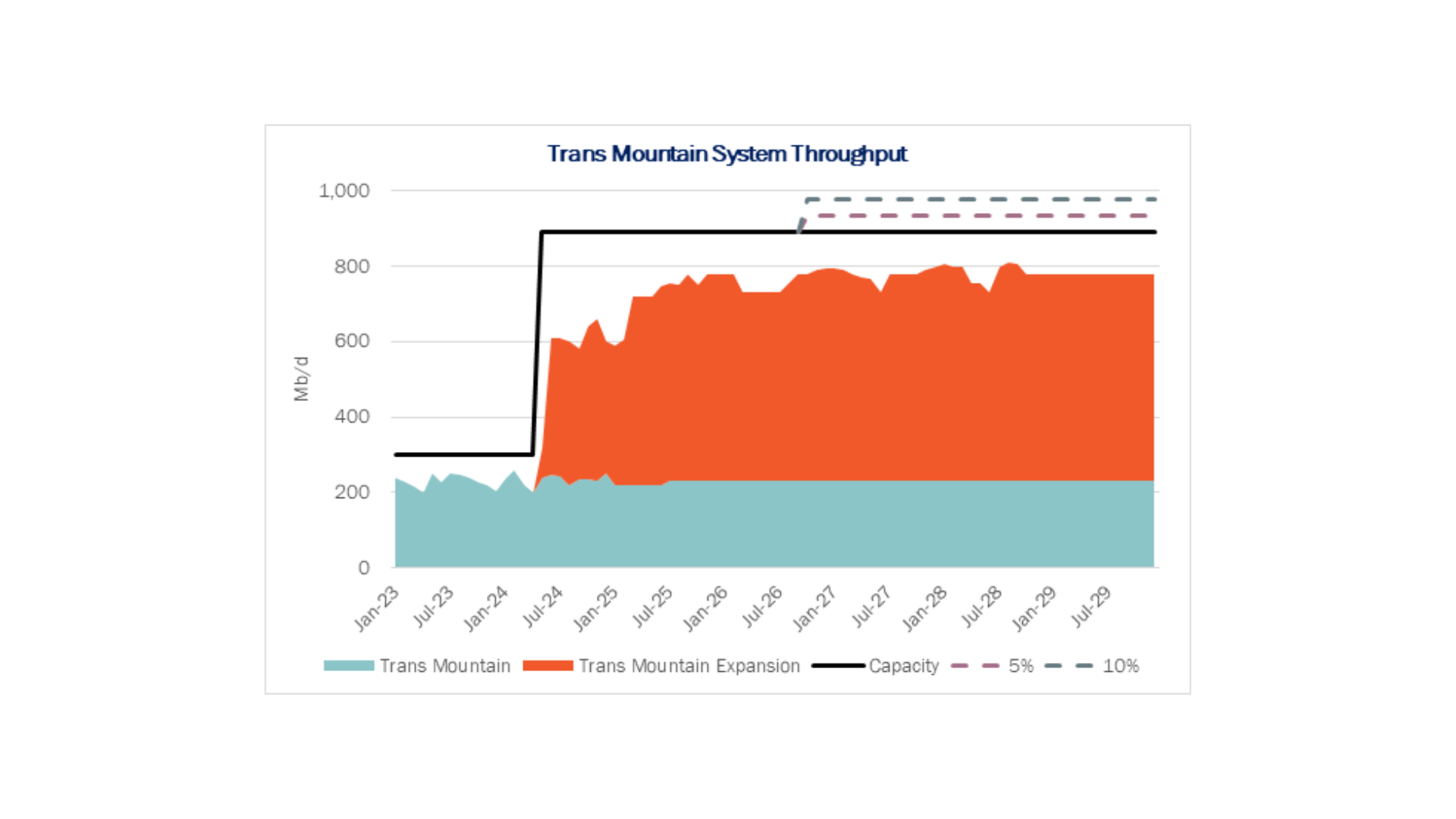

One year out from its widely anticipated looping, Trans Mountain Pipeline is weighing more expansions to boost crude exports from the Pacific coast.

Canada’s only dedicated oil export pipeline is exploring both short- and long-term projects to increase capacity by 200-300 Mb/d, Trans Mountain Corp. reported in its 1Q25 results. The pipeline is considering several options, from using drag-reducing agents (DRAs) to adding more pump stations to increase throughput.

The Trans Mountain looping expansion (TMX) began commercial operations in May ’24, adding 590 Mb/d of capacity from Alberta to the Westport Terminal in Burnaby, British Columbia. The project has helped diversify markets for Canada’s crude oil while spurring upstream expansions in the Western Canadian Sedimentary Basin (WCSB).

In an interview with The Calgary Herald, Trans Mountain CEO Mark Maki said DRA testing is already underway. Blending DRAs in the crude stream could increase the system’s capacity by 5-10% at a low capital expense. The pipeline is also working on early engineering plans to increase the number of pump stations, Maki said. The additional compressors could increase capacity to nearly 1.14 MMb/d by the end of the decade, though at a significantly higher cost.

Trans Mountain reported 1Q25 throughput of 757 Mb/d, or 85% utilization of its current 890 Mb/d capacity. According to East Daley’s Crude Hub Model, the Trans Mountain system operated at 68% utilization in December ‘24 (based on the most recent CER data), compared to 97% for Enbridge’s (ENB) Mainline and 100% for South Bow’s (SOBO) Keystone pipelines during the same period.

Trans Mountain’s announcement comes months after ENB announced plans for additional WCSB egress via a 30 Mb/d expansion on the Express-Platte system and Mainline’s Phase 1 expansion of 150 Mb/d.

Given WCSB oil production estimates, the three pipeline expansions are essential to prevent bottlenecks and preserve discount economics for heavy crude, according to the Crude Hub Model. The Trans Mountain system serves West Coast refiners and export terminals, with ~50% of exports bound for the US West Coast and the other 50% destined for Asia. ENB’s Canadian egress routes supply refiners in PADDs 2, 3 and 4, and connect to Gulf Coast export terminals for shipments to Europe.

Storage:

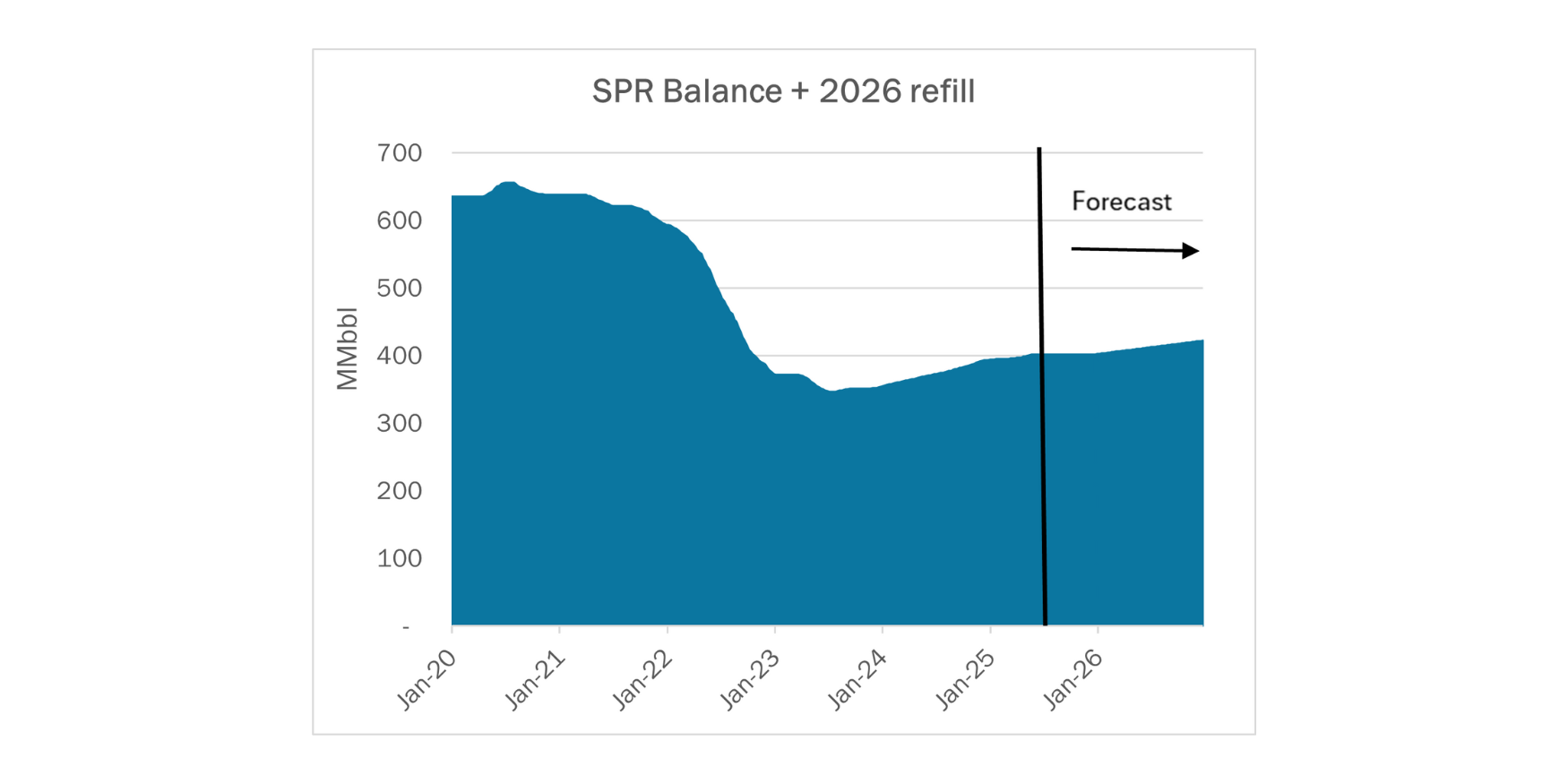

East Daley expects a 298 Mbbl injection into commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending June 7. We expect total US stocks, including the SPR, will close at 840 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, decreased 1.6% W-o-W across all liquids-focused basins. Samples decreased 4.7% in the Eagle Ford, 3.8% in the Rockies basins, 1.2% in the Permian, and 1.0% in the Gulf of Mexico. The Rockies and the Gulf of Mexico have a high correlation between gas volumes and crude oil volumes, whereas the Permian and Eagle Ford basins correlation is less than 45%.

We expect US crude production to be 13.45 MMb/d. According to US bill of lading data, US crude imports increased to 6.43 MMb/d. More than 60% of the supply originated from Canadian pipelines and vessels into the US, with the remainder largely coming from vessels carrying crude from Mexico and Nigeria.

As of June 7, there was ~371 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude input into refineries to increase, coming in at 16.1 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 21 vessels loaded for the week ending June 7 and 23 the prior week. EDA expects US exports to be 3.99 MMb/d.

The SPR awarded contracts for 6.0 MMbbl to be delivered to Choctaw February–May ‘25 and 2.4 MMbbl to be delivered to Bryan Mound April–May ‘25. The SPR has 402 MMbbl in storage as of June 7, 2025.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

Bridger Pipeline, LLC Rates were increased by the FERC index. Joint rates are less than or equal to the sum of the local rates. Effective July 1, 2025.

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)