Exec Summary:

Market Movers: EOG Resources (EOG) will acquire Encino Acquisition Partners for $5.6B, reflecting growing interest in Marcellus and Utica assets.

Rigs: Shifts in the Permian have led to stronger rig activity across WES systems but lower rig counts on EPD systems.

Flows: DTM is seeing lower volumes across its gathering systems, but the macro outlook calls for Haynesville growth in the back half of 2025, which should support a rebound.

Calendar: EDA will be in NYC July 29-31. Please reach out if you would like to schedule a market update while we are in town.

Market Movers:

On May 30, EOG Resources (EOG) announced a $5.6B deal to acquire Encino Acquisition Partners, adding momentum to a recent surge in transactions targeting the Northeast. The Encino deal follows activity surrounding Gulfport Energy (GPOR), Ascent Resources, and Infinity Natural Resources (INR).

GPOR, one of the Utica’s largest producers, has signaled interest in M&A. CEO John Reinhart recently stated that GPOR is evaluating acquisition opportunities with the goal of building resource depth and capturing long-term value. INR completed an IPO in January, and Ascent signaled to public debt holders in March that it too is considering an IPO. This flurry of activity suggests a shifting dynamic in the Northeast energy landscape.

One factor attracting interest is rising hopes for new regional infrastructure. Projects such as Constitution Pipeline, Northeast Supply Enhancement, and open seasons for Millennium PRO and Texas Gas Transmission’s Borealis project could create new growth opportunities for producers later in the decade.

Sharply increasing demand projections for data centers are also a driving force. In the Data Center Demand Monitor, East Daley currently tracks ~35 GW of data center projects under development on the regional PJM transmission grid. These projects will support more gas demand for power generation.

With infrastructure projects gaining traction and regional demand set to ramp, producers are positioning to capture expanding market share. Through the Encino acquisition, EOG not only secures liquids-rich acreage in the Utica but also adds 330,000 acres in the dry gas window — an asset that could gain value as gas demand and egress capacity grow.

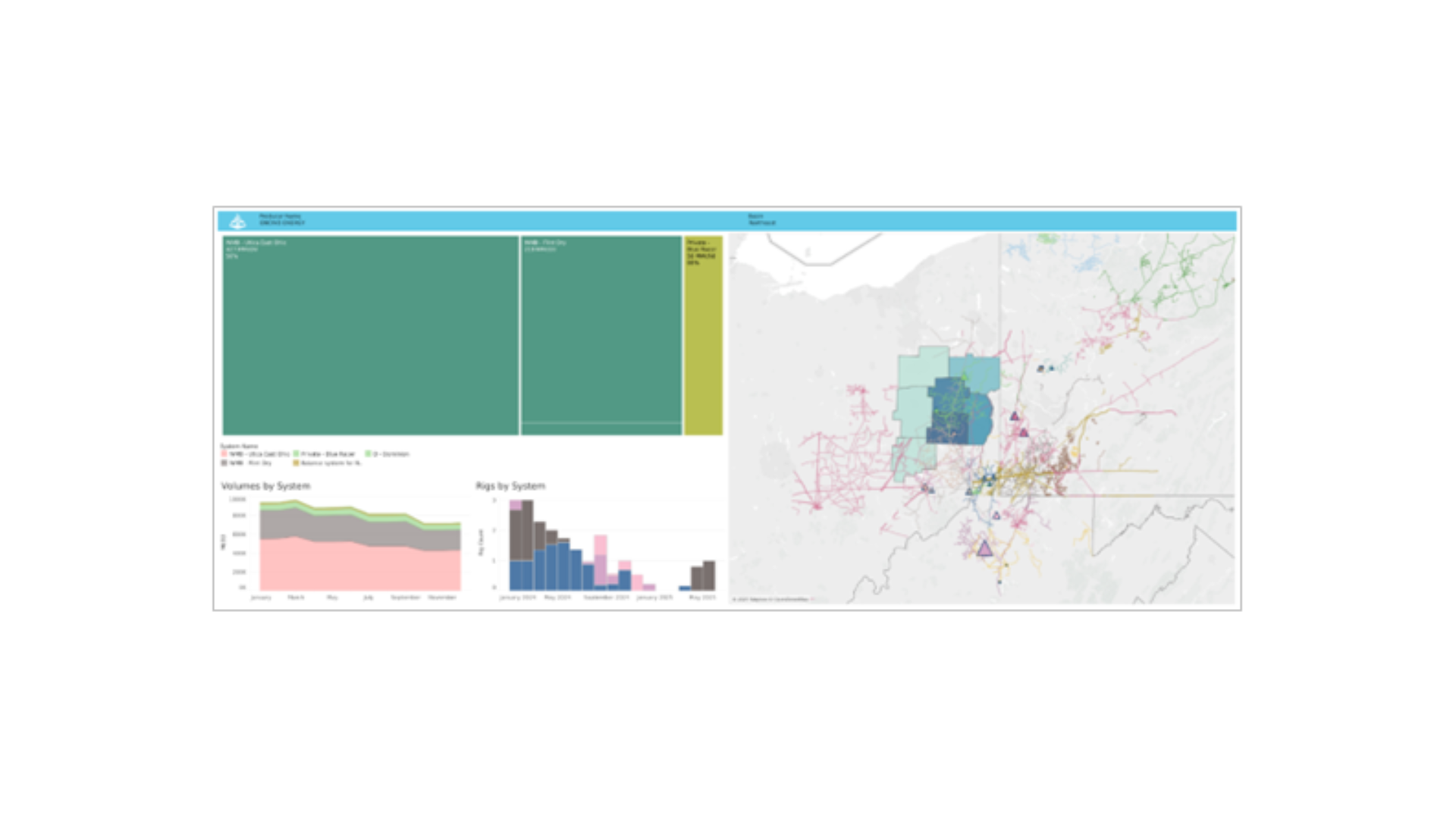

The figure from East Daley’s Energy Data Studio profiles rigs, volumes and G&P counterparty data for Encino. Williams (WMB) operates the Utica East Ohio, Flint Gathering, and Blue Racer gathering systems, which currently receive volumes from the producer. Given the operational efficiencies highlighted in EOG’s transaction materials, WMB could benefit from increased volumes through its Utica systems.

Rigs:

- The EPD rig count is down 24% vs 1Q25. Diamondback and Permian Resources have maintained relatively steady activity on EPD systems, but Mewbourne (-4.5) and EOG (-2) have dropped rigs since the beginning of the year.

- The WES rig count has increased 10% vs 1Q25. EOG Resources is the main driver of the increase, climbing from 2 rigs in January to ~6 rigs in June. Given current activity, EDA predicts continued strong operating results for 2Q and 3Q volumes.

Flows:

- WES volumes are up 5% vs the prior quarter and 10% relative to 2Q24. The flow sample for WES systems tracks closely with state-reported plant volumes but trail the total production outlook. The flow sample typically covers 55-60% of total WES production.

- The DTM sample has continued to trend downward. East Daley sees current DTM performance as a low-water mark, with strong macro events set to deliver increased production in the Haynesville. The current flow sample is about 25% lower than the historic high of ~3 Bcf/d set in 1Q24.

Calendar: