The Daley Note: September 23, 2022

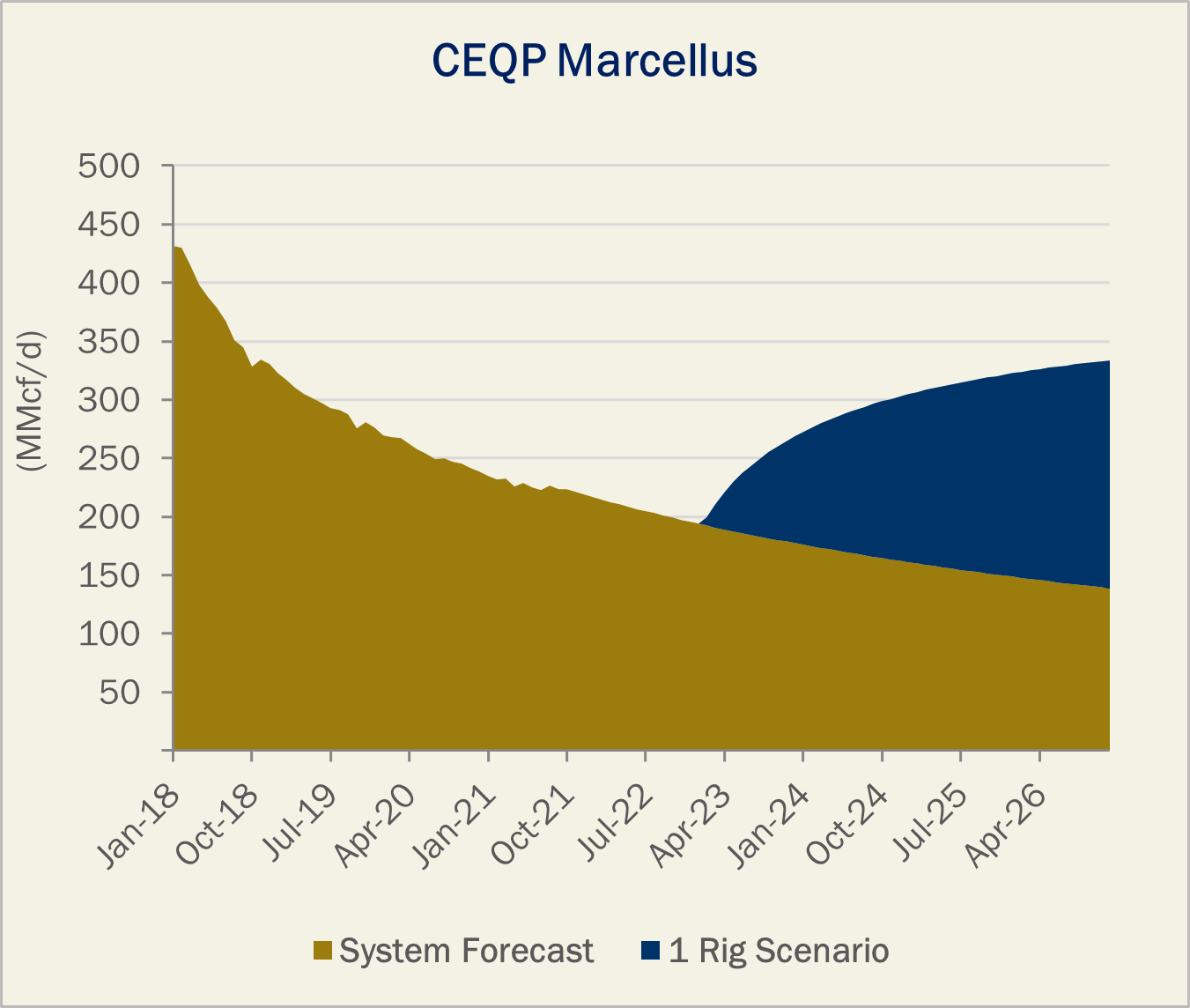

Crestwood Equity Partners (CEQP) sold its southwest Marcellus gathering and compression assets to Antero Midstream (AM) for $205 million last week. With natural gas prices above $9, we see an opportunity for AM to turn around the flagging system.

The deal represents a 7x 2023 EBITDA multiple, according to a Sept. 12 CEQP release. The system in Harrison County, WV is located in a dry area of the Marcellus with a gathering capacity of 875 MMcf/d. Volumes averaged 227 MMcf/d in 2021 under a fixed-fee contract with AM parent Antero Resources (AR), with 10 years remaining.

East Daley estimated the system gathering rate to be $0.40/Mcf. The last time East Daley allocated a rig to the CEQP system was in 2015; since then, volumes have been in natural decline. With liquids prices elevated, AR has not been operating in this area, instead focusing its drilling on more NGL-rich Marcellus/Utica targets via its current drilling agreement with QL Capital Partners.

We expect a continued hesitancy to drill in the area due to a healthy supply of drilling locations on existing AM infrastructure that fall under the growth incentive fee reduction incentives for AR, while the new CEQP footprint does not.

Additionally, AM has plans to continue expanding its legacy gathering capacity by relocating compressors. AM plans to continue moving compressors through 2024 to move capacity where AR needs it most.

AM estimates $50 million in discounted future capital avoidance with the deal and may potentially be able to leverage moving some underutilized compressors from the newly acquired acreage as well. After 2024, the compressor relocations should be complete along with the rate incentive fee, and then it may make more sense for AR to tap into the newly purchased system. Now that AM owns the system, Antero is more likely to bring back a rig which could significantly increase volumes on the system.

The system’s current throughput is ~200 MMcf/d, according to AM. New drilling should be economic in the future at higher natural gas prices; Antero’s wells have robust average initial production (IP) rates of 13 MMcf/d, according to East Daley’s allocation model.

One rig on this system would be enough to reverse the natural decline and grow system volumes. This divestiture makes sense for both parties as CEQP focuses instead on the Bakken and Permian while Antero sees better terms as the anchor producer on the AM system. – Alex Gafford & Zack Van Everen Tickers: AM, AR, CEQP.

Upcoming Event

HART Energy – America’s Natural Gas Conference 9 a.m. – Tuesday, Sept. 27 in Houston, TX

Click here to set up a meeting with Zack on Weds., Sept. 28 in Houston the day following EDA’s presentation.

The Daley Note

Subscribe to The Daley Note (TDN), “midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.

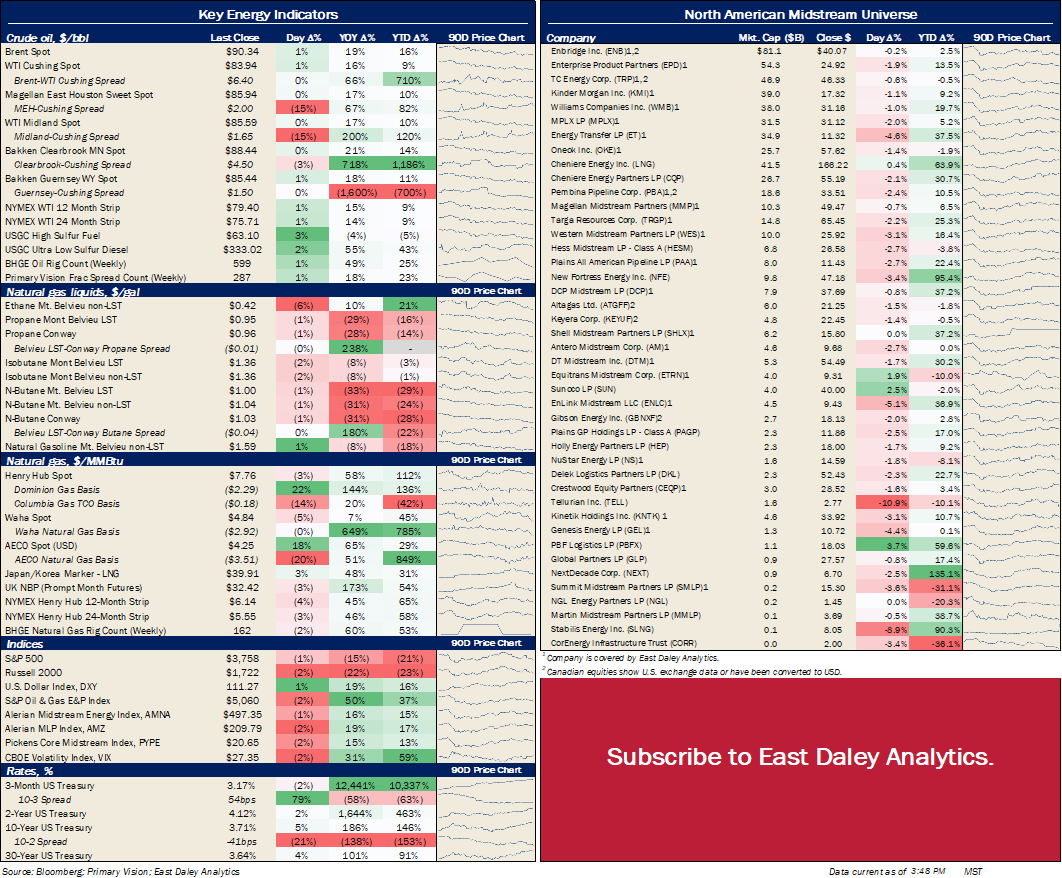

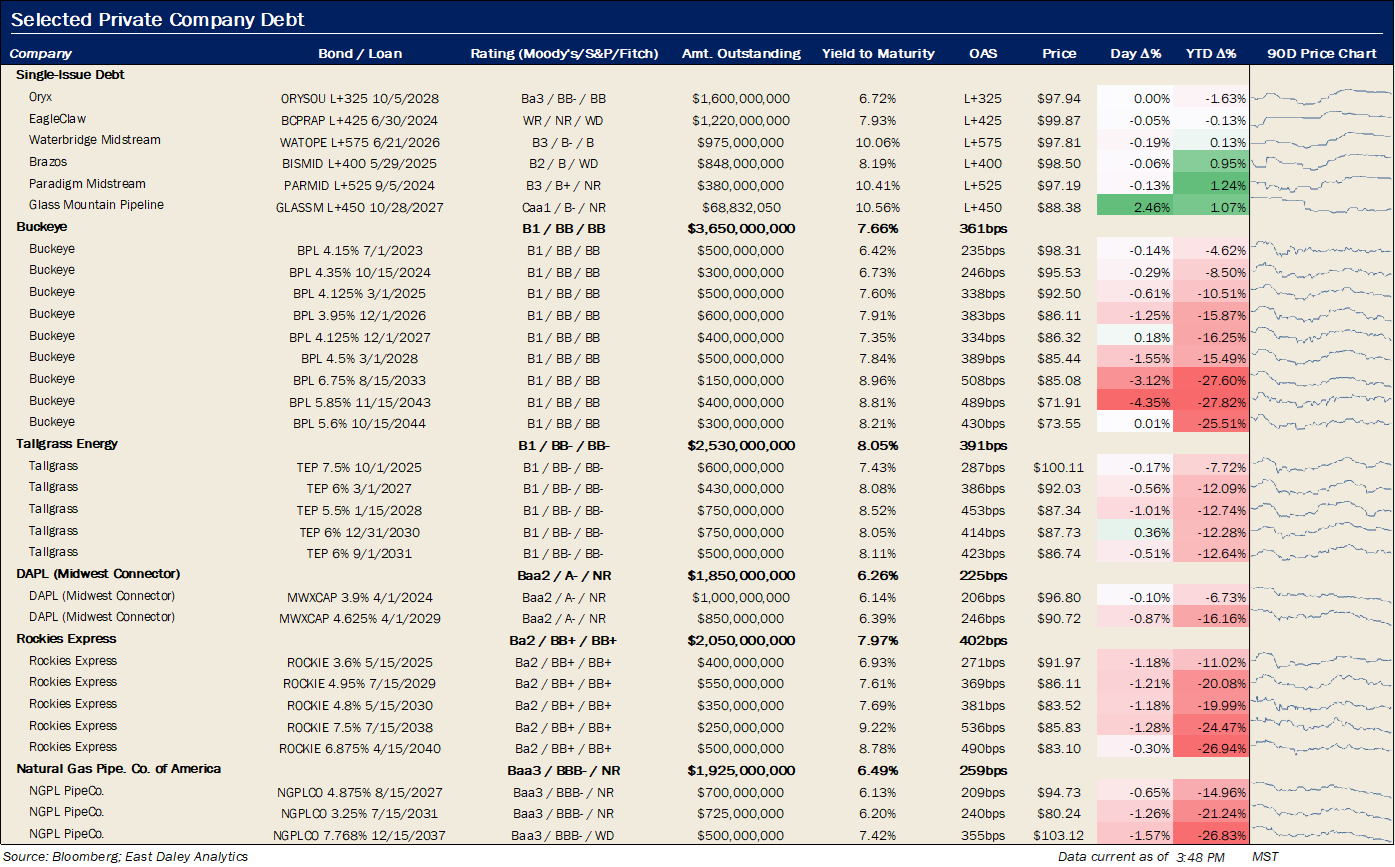

North American Energy Indicators and Equity Prices

North American Energy Indicators and Equity Prices

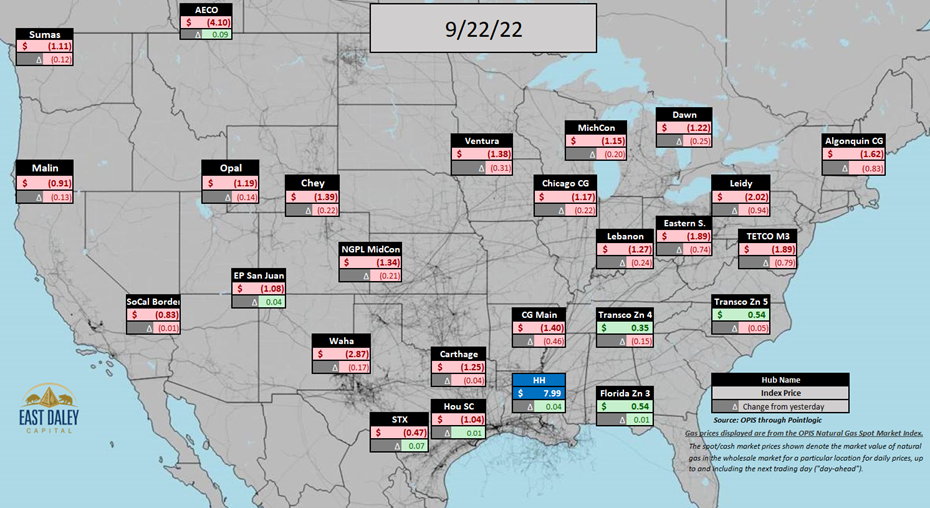

North American Natural Gas Prices

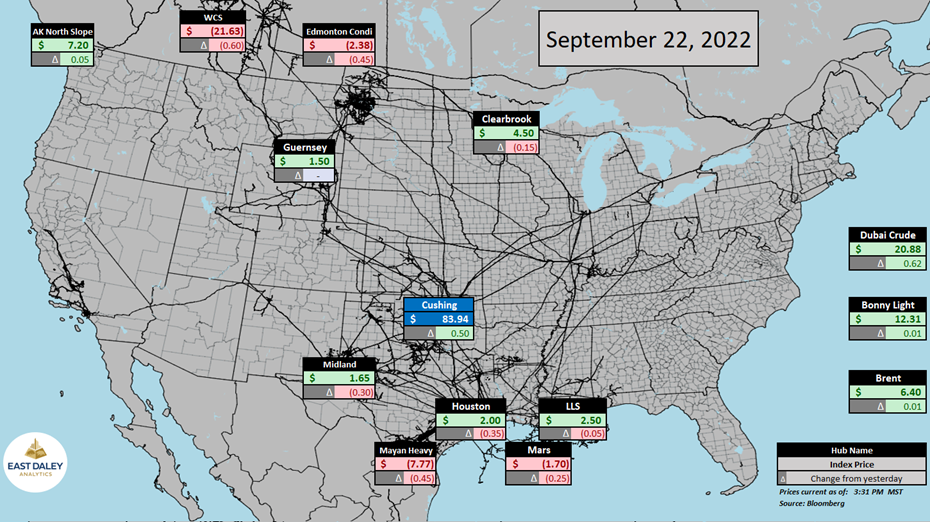

North American Crude Oil Prices

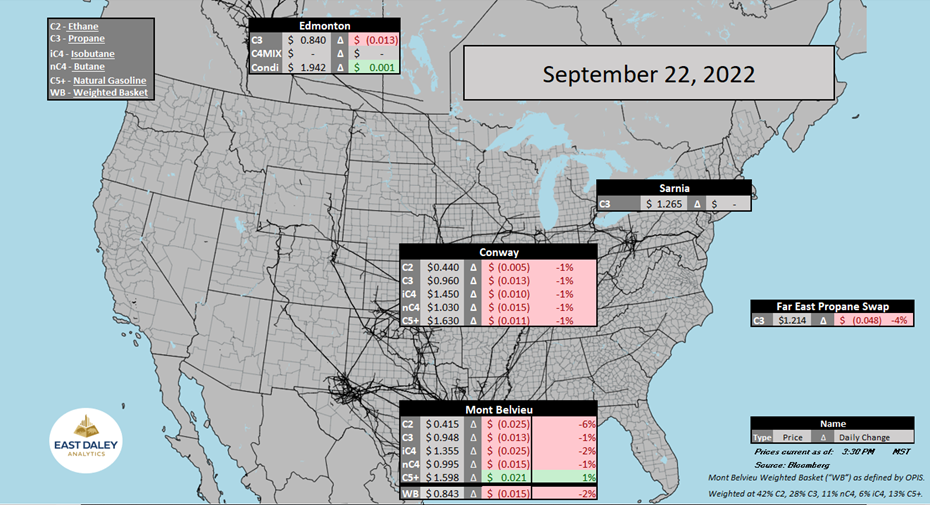

North American Natural Gas Liquids Prices

Subscribe to The Daley Note (TDN),“midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.

-1.png)