The Daley Note: September 22, 2022

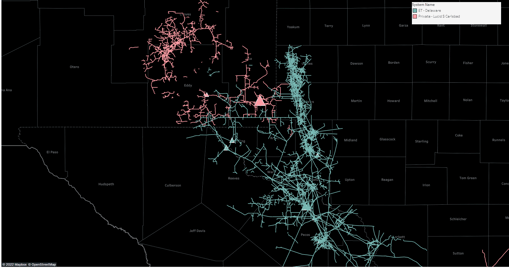

Energy Transfer’s (ET) Permian systems lost 5 rigs for the week of Sept. 4, the largest W-o-W drop by all public and private midstream systems we track on our weekly Midstream Activity Tracker. The declining activity may indicate increased competition in the basin, especially given G&P consolidation in the past six months.

The company’s Midland system lost 2 rigs and is now at only 8 active rigs, the lowest level since February 2022. ExxonMobil (XOM) is the largest counterparty on ET’s Midland system, but recently reduced its count from 5 rigs in July to only 2 rigs currently. XOM moved some rigs to rival Targa’s (TRGP) West Texas system. Given XOM’s historical presence on ET-Midland, it is likely the rig reduction is just a short-term blip rather than a long-term risk to ET.

In the Delaware, ET’s system lost 3 rigs but still stands at a healthy 18 rigs. EOG Resources (EOG) primarily drove the shift, moving its 3 rigs from ET to Lucid’s South Carlsbad system, which TRGP is currently acquiring. EOG has significantly ramped drilling on the Lucid/TRGP system, increasing counts from 3 rigs in May to 13 rigs as of Sept. 4.

With ET’s largest rivals, Enterprise (EPD) and TRGP, acquiring major Permian G&P systems this year, we feared the company would lose market share in the Permian. While absolute rig counts on ET’s Permian systems have remained stable at ~30 rigs since March, its peers have been capturing more of the rig additions. EPD (including Navitas) has increased its share by adding 10 rigs since March and is now at ~40 rigs. TRGP, including Lucid, has also increased rigs by ~10 and currently has ~100 rigs across its Permian systems.

East Daley does not expect ET to face volume or EBITDA declines on its Permian systems. An average of 30 rigs is more than enough to drive volume growth and support the company’s two new Permian processing plant expansions, as well as its downstream NGL assets. However, in relative terms, its growth may be lower than that of its peers. EPD has already announced a 275 Mb/d expansion to its Shin Oak pipeline, and the company will likely leverage growth from its Navitas assets to help fill it. TRGP has also stated it will shift any overflow volumes on Lucid’s system to its own Permian G&P systems and incremental NGL volumes to its Grand Prix pipeline (see our June 22 Midstream Navigator, “Targa Acquiring Lucid Energy for $3.55 Billion”).

While ET may have relinquished some market share in the basin by not partaking in the G&P consolidation, the overall Permian pie is still growing, its systems should remain competitive, and the company has an already large slate of projects to manage such as Lake Charles LNG, the Warrior pipeline, and a potential ethane cracker. — Ajay Bakshani, CFA Tickers: EOG, EPD, ET, TRGP, XOM.

Upcoming Event

HART Energy – America’s Natural Gas Conference 9 a.m. – Tuesday, Sept. 27 in Houston, TX

Click here to set up a meeting with Zack on Weds., Sept. 28 in Houston the day following EDA’s presentation.

The Daley Note

Subscribe to The Daley Note (TDN), “midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.

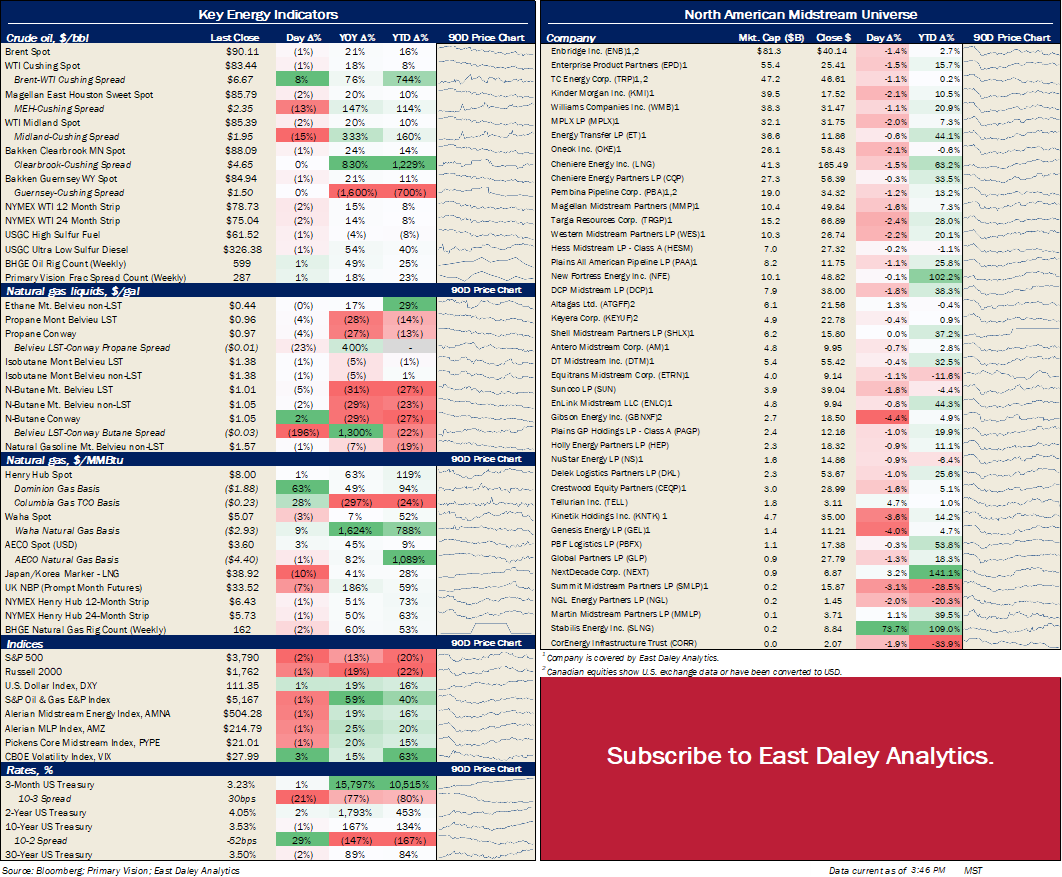

North American Energy Indicators and Equity Prices

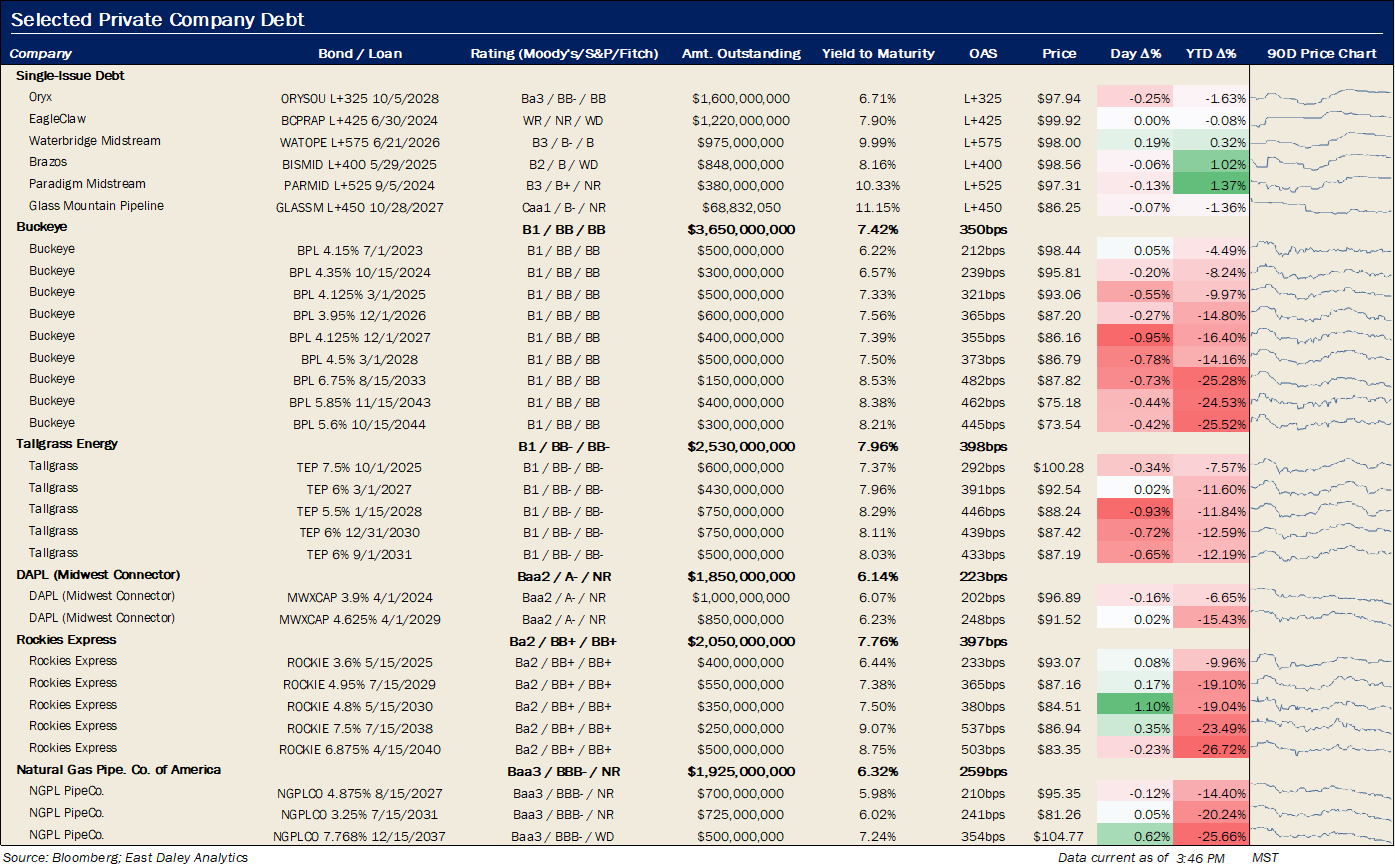

Key Private Debt Metrics

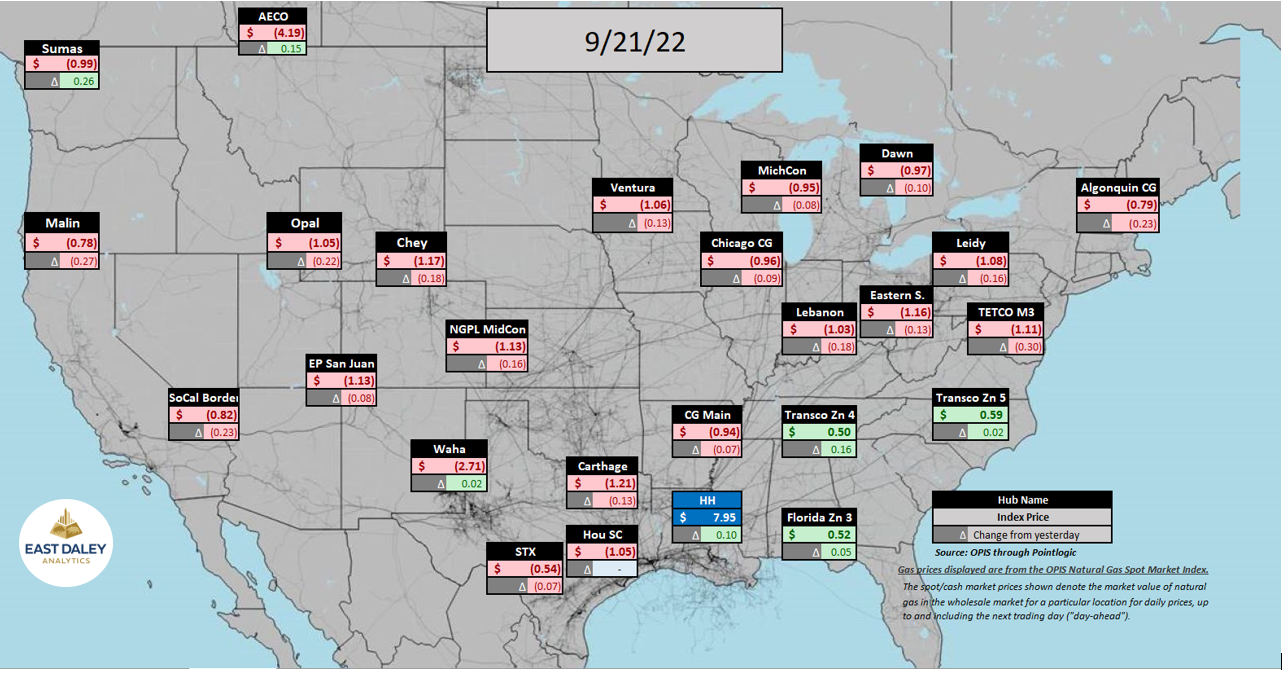

North American Natural Gas Prices

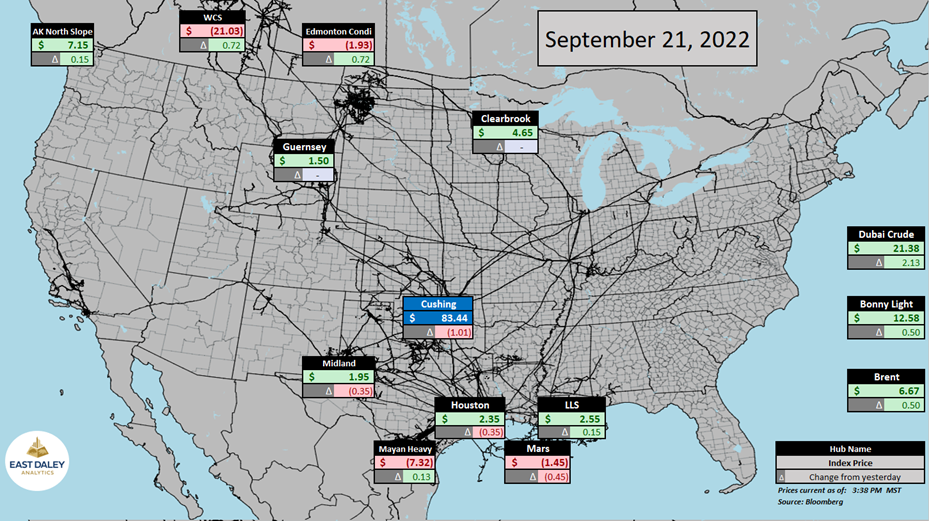

North American Crude Oil Prices

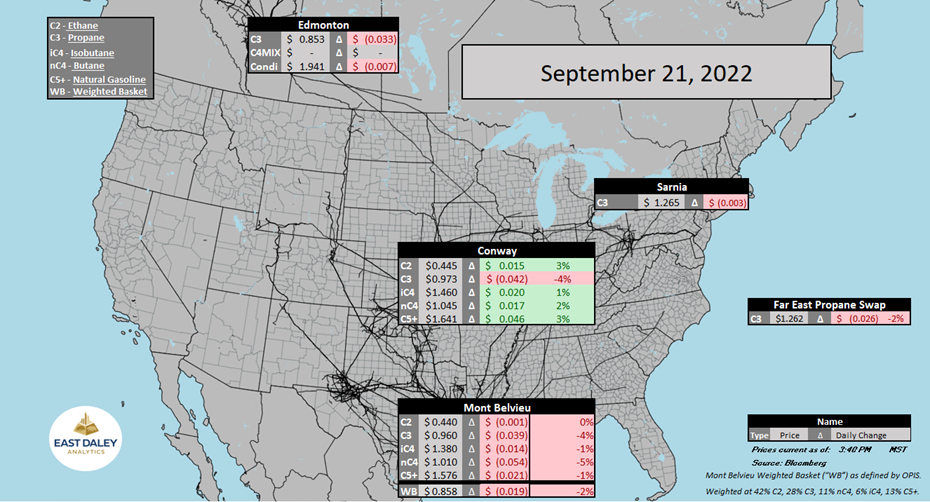

North American Natural Gas Liquids Prices

The Daley Note

Subscribe to The Daley Note (TDN), “midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.

-1.png)