The Daley Note: September 8, 2022

The Energy Administration (EIA) recently announced it expects ethane production to grow by 9% in 2H22, from 2.4 MMb/d to 2.6 MMb/d, slightly below our forecast for 10% production growth. This growth and related ethane recovery should be a boon for natural gas processors including MPLX (MPLX) and Williams (WMB).

While our forecast is in line with EIA’s, we can use our Purity Product Forecast tool to go deeper than the PADD level that the EIA typically reports. East Daley can point to where this growth is coming from.

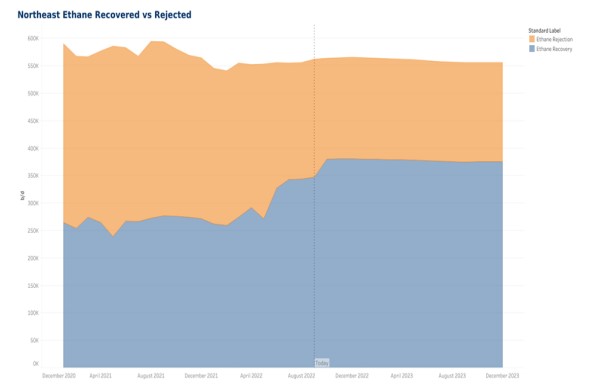

From FY21 to FY22, most of the ethane growth is unsurprisingly from the Permian. We expect the basin to grow by 167 Mb/d to 1.1 MMb/d exit-to-exit. The Northeast is the next-largest source of ethane growth, adding 109 Mb/d exit-to-exit. Most of the growth has been weighted to the first half of the year, growing 214 Mb/d vs only 164 Mb/d for 2H22.

The ramp in the first half of the year reflects high frac spreads in the Permian and the start-up of the Baystar cracker. For the second half of 2022, ethane production growth will be more weighted toward the Northeast. We expect an additional 50 Mb/d of ethane production in the Northeast in 2H22, almost entirely driven by higher ethane recovery rather than true production growth.

We believe this growth is reflective of Shell’s Monaca cracker that is expected to come online soon and will be ramping up through the end of the year. Higher ethane recovery in the Northeast will be a tailwind for natural gas processors in those basins, such as MPLX (MPLX) and Williams (WMB). For the Permian, we expect processors in the region like Enterprise (EPD) and Targa (TRGP) to see higher rejection compared to the first half of the year.

Our rejection estimates may increase however, given fractionation constraints at Mont Belvieu and Conway. East Daley has written extensively about the tight NGL fractionation market, and we noted increased rejection could help alleviate those constraints. We published a Midstream Navigator, “Medford Outage Shakes Up NGL Markets,” on August 18; please click here to access.

However, there is a limit to increased rejection as Permian gas egress also tightens in 2023. Producers may turn to flaring until new fractionators and natural gas egress expansions come online, which adds downside risk to our current forecast.

Welcome to East Daley Analytics

East Daley is excited to announce our transition to East Daley Analytics – reinforcing our commitment to driving transparency and connecting value chain analysis for energy markets.

We’ve updated our website to reflect our focus as a data and analytics company, and the new client portal will provide easy access to your subscription products.

Subscribe to The Daley Note (TDN), “midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.

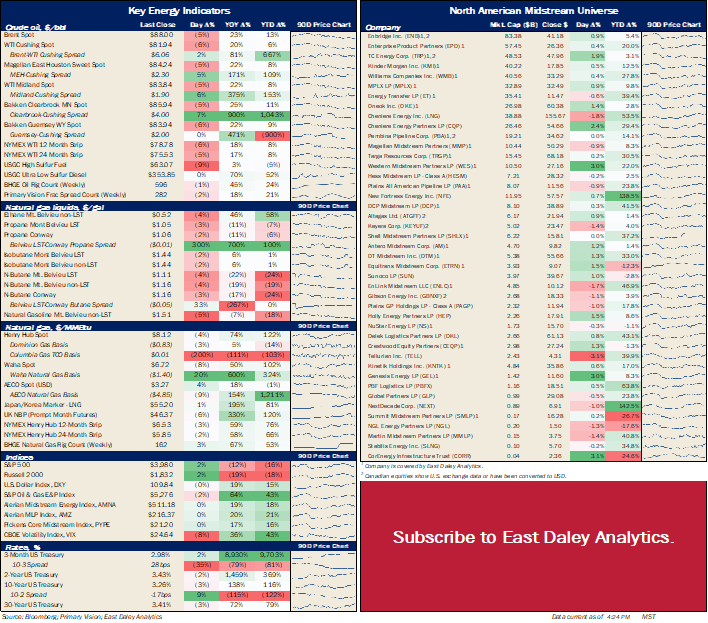

North American Energy Indicators and Equity Prices

Key Private Debt Metrics

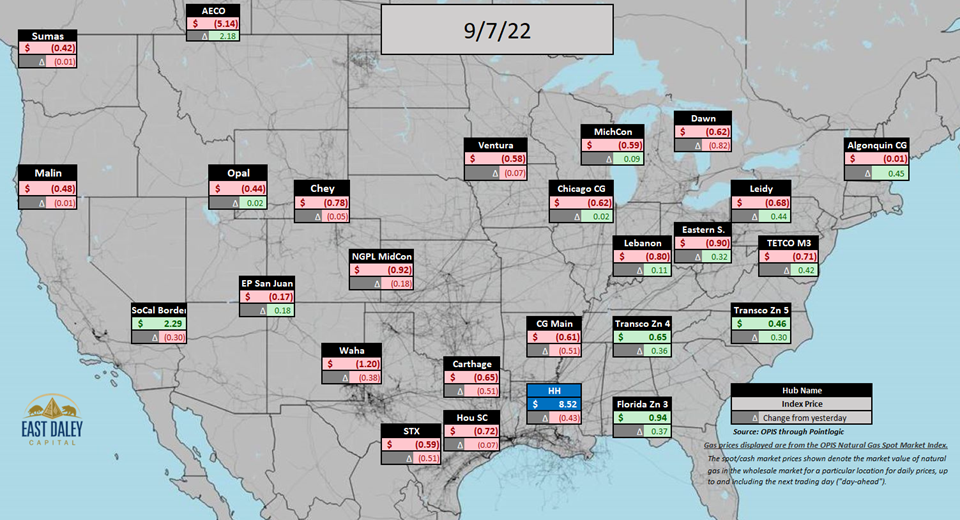

North American Natural Gas Prices

North American Crude Oil Prices

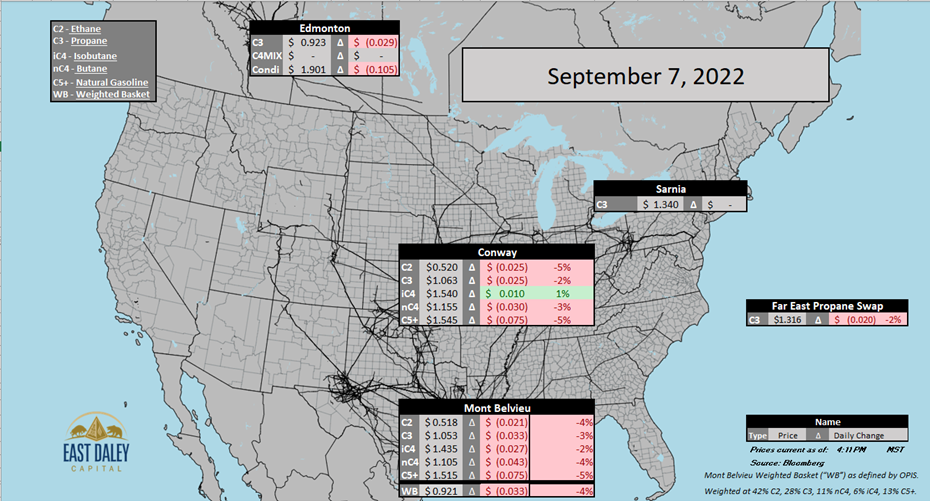

North American Natural Gas Liquids Prices

Subscribe to The Daley Note (TDN), “midstream insights delivered daily,” covers news, commodity prices, security prices, and EDA research likely to affect markets in the short term.