Natural Gas Weekly: March 30, 2023

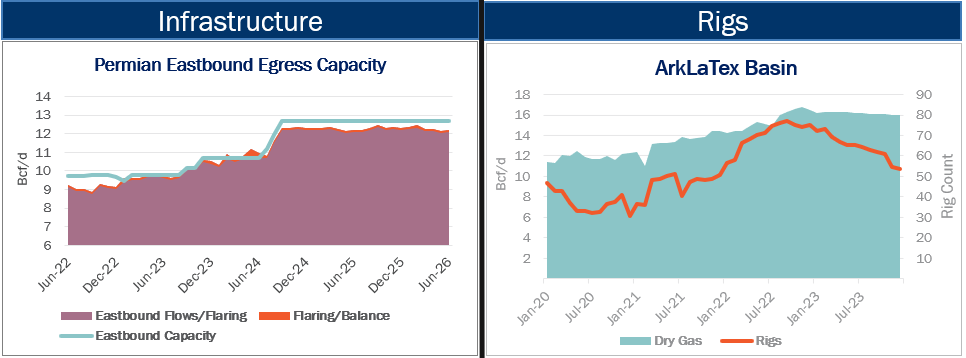

Infrastructure - Permian natural gas prices are likely to remain volatile in April as several Gulf Coast-bound pipeline systems conduct seasonal maintenance.

In a recent notice to shippers, Permian Highway Pipeline (PHP) said it plans to reduce available capacity to 1.6 Bcf/d from April 1-11 to replace a valve connecting to Kinder Morgan’s (KMI) Tejas Pipeline. The maintenance on PHP will temporarily remove ~0.5 Bcf/d of takeaway to South Texas.

Gulf Coast Express (GCX) announced earlier in March it plans to reduce system capacity to 1.2 Bcf/d from April 11-12, and to 1.6 Bcf/d from April 13-14, to perform work on the system. GCX can normally transport 2.0 Bcf/d from the Permian to the Agua Dulce hub.

With Permian pipeline egress already constrained, these service disruptions will no doubt result in downward pressure on Waha prices. In our Permian Supply and Demand Forecast, East Daley forecasts pipelines out of the basin to run at over 100% utilization during these maintenance events. Capacity looks tight regardless; we forecast Permian egress pipelines would run at 97% of effective capacity in April with all systems functioning normally.

Rigs - With the 2022-23 winter mostly in the rear view, the natural gas market will be contending with a large storage overhang through 2023 that we expect to eventually force producers to slow growth.

In the Balanced scenario of East Daley’s Macro Supply and Demand Forecast, we guide for relatively flat supply during 2023. We forecast US gas production to exit 2023 with a gain of less than 1 Bcf/d (+1.3%) over YE22. For the April-October 2023 storage injection season, we model supply growth of less than 0.2 Bcf/d.

US storage inventories as of March 24 are 321 Bcf above the five-year average, according to the latest EIA storage report. Higher demand this year could eat into the storage surplus, but the market will face formidable comparisons to the blistering-hot summer of 2022 that saw record consumption for power generation. Absent demand growth, supply will have to slow at some point to avoid a storage overfill. The physical limitations of storage, coupled with rapid supply growth entering the year, are key pillars of our sub-$2 gas call in 2023.

To achieve a balanced market, we anticipate lower production from the ArkLaTex (-0.24 Bcf/d) and the Northeast (-0.22 Bcf/d) later this year. Rigs in the ArkLaTex Basin decrease by 6 and average 64 rigs in 2023 in our Balanced scenario.

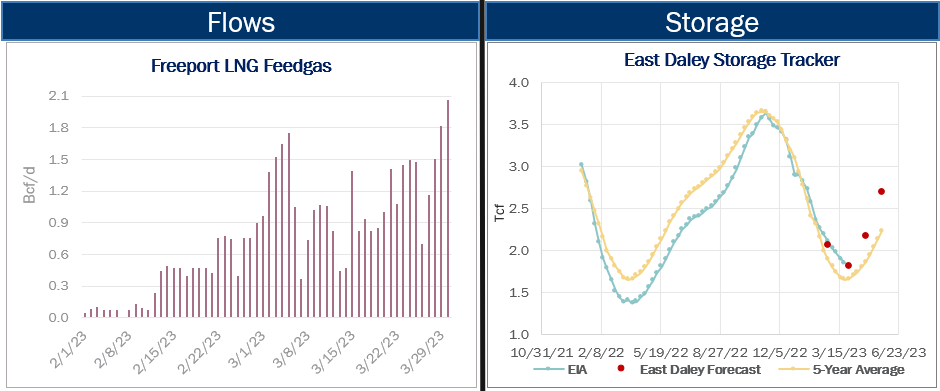

Flows - Feedgas to Freeport LNG hit a new high this week as the LNG facility continues to restart from an 8-month outage. Pipeline deliveries to Freeport rose to 2.06 Bcf/d on Thursday (March 30), moving the Texas LNG plant closer to its maximum intake of ~2.2 Bcf/d. Pipeline deliveries to Freeport averaged 1.46 Bcf/d for the latest 7 days. The higher sustained intake likely indicates that all three LNG trains at Freeport are operational.

Storage - EIA reported a 47 Bcf storage withdrawal for the March 24 week, putting working gas inventories at 1,853 Bcf. In our updated Macro Supply and Demand Forecast, we estimate storage inventories end March at 1,815 Bcf. US storage is 351 Bcf above the 5-year average after the latest EIA report.

Natural Gas Weekly

East Daley Analytics' Natural Gas Weekly provides a weekly update to our monthly Macro Supply and Demand Forecast. The update covers rigs, flows, production, prices and capacity constraints that materially change our view on supply and demand. This update highlights what investors and traders need to monitor in natural gas to ensure they are on the right side of the market. Subscribe to the Natural Gas Weekly.

-1.png)