Natural Gas Weekly: August 22, 2024

Infrastructure – East Daley expects Permian gas production to exit 2024 at 26 Bcf/d in the latest Permian Supply & Demand Forecast, for Y-o-Y growth of 1.7 Bcf/d. Output in 1H24 was handicapped by takeaway constraints, but we expect start-up of Matterhorn Express Pipeline to launch a new growth phase for the basin.

With Matterhorn expected online in 3Q24 and the new Blackcomb Pipeline to start later in 2H26, the Permian Basin will see 5 Bcf/d of additional egress capacity to incentivize supply growth. EDA’s forecast is backed by a considerable expansion ahead in gas processing capacity. From 2024–26, companies plan to add 3.7 Bcf/d of processing capacity in the Permian (2.4 Bcf/d in the Delaware and 1.3 Bcf/d in the Midland). Based on our current production forecast, we model Permian processing plant utilization to average 82% in 2024, rising to 88% by 2026.

Along with supply growth, Matterhorn and Blackcomb pipelines are likely to realign some gas flows out of the basin. We predict some northbound volumes that move to the Midcontinent will be rerouted to fill the new pipes. Moving more natural gas along the eastbound route (Waha to South Texas) will impact market dynamics at the Houston Ship Channel market and relieve pressure on Waha prices over the medium term. Our new hub pricing view should be reflected in the next updates to our Permian and Houston Ship Channel Supply and Demand reports.

Flows – East Daley’s ArkLaTex Basin sample is down over 1.8 Bcf/d on average YTD compared to 2023 volumes, though Haynesville producers have shown more activity recently.

The ArkLaTex sample is up 166 MMcf/d M-o-M in August, reaching a summer high of 10.55 Bcf/d. Most of the growth has come out of East Texas on Williams’ (WMB) Trace Midstream, the Enterprise (EPD) - East Texas, and Momentum Midstream gathering systems.

Gathering samples in the ArkLaTex troughed in June at around 10.1 Bcf/d as producers curtailed spring volumes in response to weak prices. Chesapeake has reported up to 1 Bcf/d in deferred TILs, and has warned of additional curtailments through the fall if prices don’t improve.

Storage – Traders and analysts expect the Energy Information Administration (EIA) to report a net injection of 27 Bcf into working gas for the week ending August 16. The surplus to the 5-year average would fall by 14 Bcf to 361 Bcf while the surplus to last year would increase by 4 Bcf to 213 Bcf.

In the latest monthly Macro Supply & Demand Forecast, East Daley projects the surplus to the 5-year average will fall to 172 Bcf by the end of October. This would imply that injections over the next 11 weeks (through October 31) would fall by 203 Bcf vs the 5-year average injection rate, or 18.5 Bcf per week. For the first 19 weeks of the 2024 injection season, the injection pace has trailed the 5-year average by 13.5 Bcf/week.

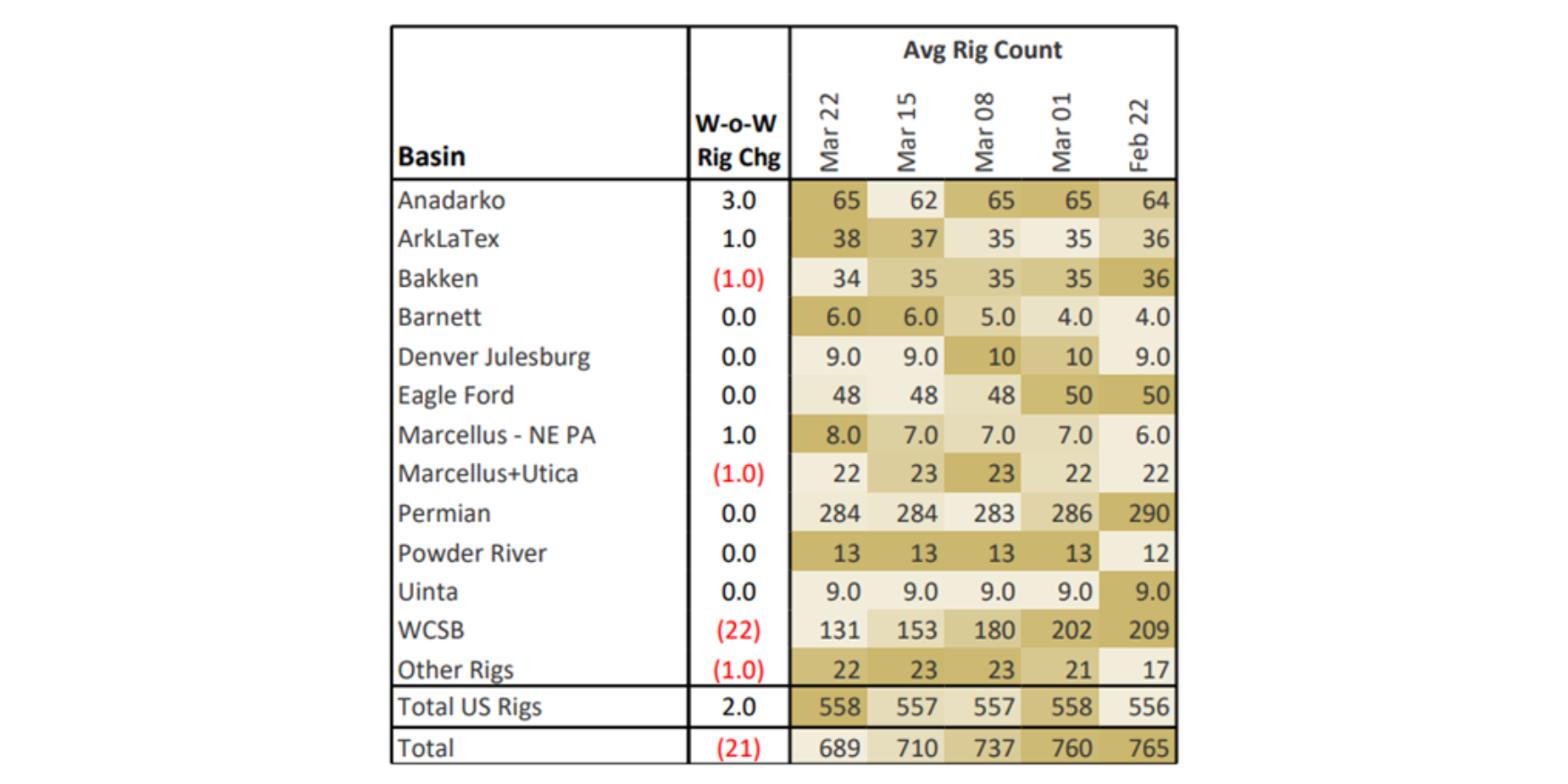

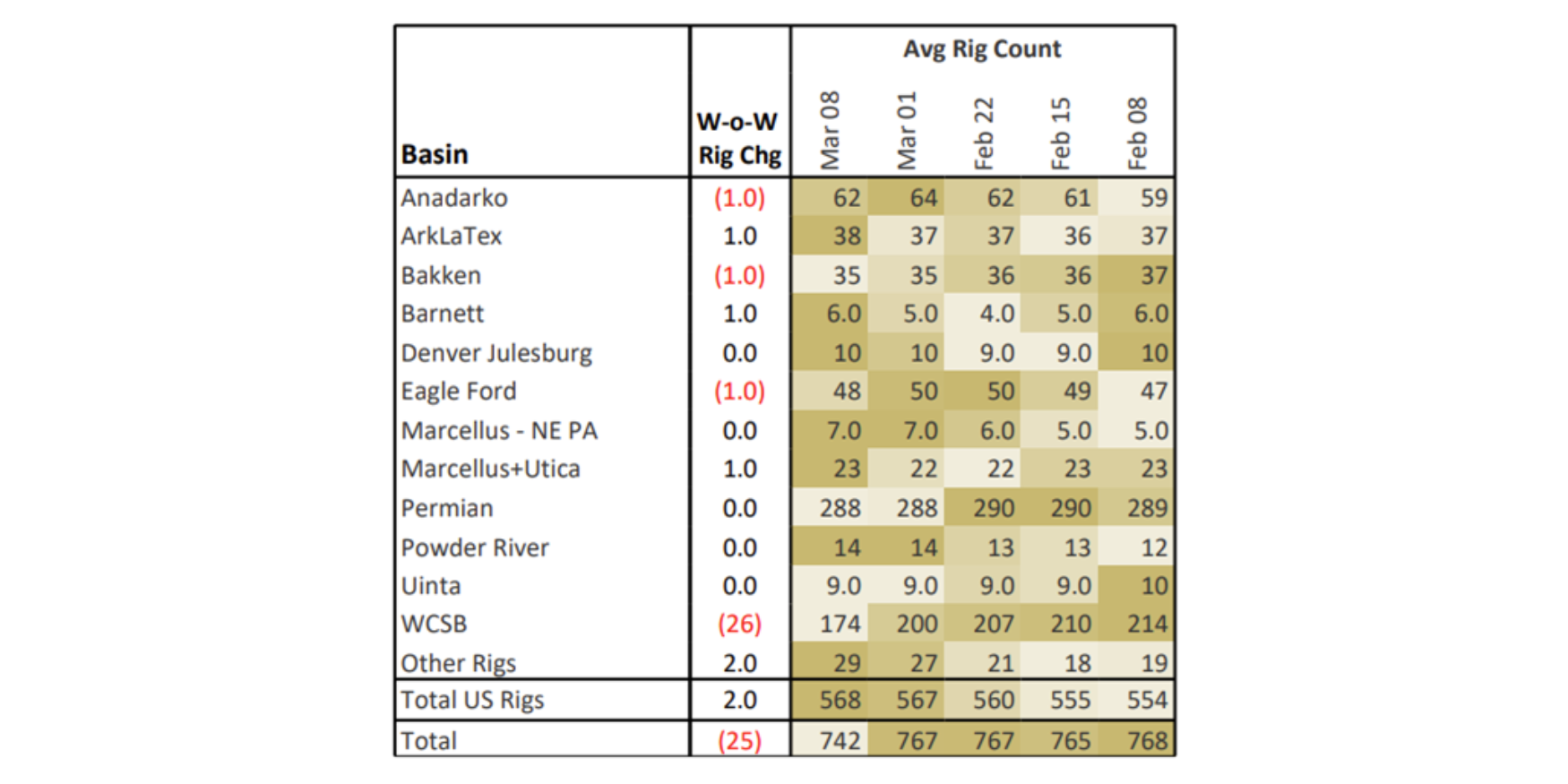

Rigs – US rigs decreased by 7 W-o-W to bring the total count to 559 for the August 10 week. Basins with rig reductions include the Bakken (-3), Marcellus-NE PA (-2), Permian (-2) and the Anadarko (-1). The Powder River Basin added 1 rig on the week.

On the midstream side, Targa Resources (TRGP) is down 4 rigs total with losses on its Permian and Bakken systems. Enterprise Products (EPD) gained 2 rigs in the San Juan and Piceance basins.

East Daley’s weekly Midstream Activity Tracker monitors rig activity by basin and by gathering and processing (G&P) system to better understand midstream impacts. We allocate rigs and monitor flows through 150+ public and privately owned G&P systems in every North American basin. Reach out for more information on the Midstream Activity Tracker.