Executive Summary: Rigs: The total US rig count decreased by 6 rigs for the May 12 week, down to 562 from 568. Infrastructure: ConocoPhillips (COP) will acquire Marathon Oil (MRO) in an all-stock deal worth $17.1B, the companies announced Wednesday (May 29). Storage: East Daley expects a withdrawal of 672 Mbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 24.

Rigs:

The total US rig count decreased by 6 rigs for the May 12 week, down to 562 from 568. Liquids-driven basins again drove the decline, down 8 rigs W-o-W to a total of 458. The Permian Basin lost 3 rigs, as the Delaware lost 1 rig and Midland lost 2. The Bakken decreased by 4 rigs, down to 33 from 37, and the Eagle Ford rig count decreased by 2.

In the Permian, Delaware operator Battalion Oil dropped 1 rig. Midland operators Ring Energy and Buck Wheat Resources both removed 1 rig from the basin. In the Bakken, 4 total rigs were lost, as Chord Energy removed 2 rigs, Petro-Hunt removed 1, and Iron Oil removed 1 for a total of 33 rigs. In the Eagle Ford, EOG Resources dropped 2 rigs, decreasing the total rig count to 53 from 55.

Infrastructure:

ConocoPhillips (COP) will acquire Marathon Oil (MRO) in an all-stock deal worth $17.1B, the companies announced Wednesday (May 29). With an enterprise value of $22.5B (including $5.4B in debt), the merger creates new risk to rig counts in the Bakken.

In an investor update, COP said it aims to create synergies from Marathon’s assets in the Bakken, Delaware and Eagle Ford basins. MRO adds a total of ~2,000 new drilling locations and >1,000 refrac opportunities, making it possible to increase production by streamlining its asset portfolio. COP said it also saw an opportunity to lower rig counts and rig crews in the Bakken. The companies expect to close the deal in 4Q24.

Five operators predominantly drive Bakken activity, producing >50% of the basin’s light, sweet crude: Chord Energy/Enerplus, Continental Resources, Hess (now Chevron (CVX)), MRO and ExxonMobil (XOM). Other than Continental, which took itself private, these are all large, publicly traded operators. Chevron’s recent merger with Hess will change producer dynamics as well, as we expect to see rig counts come in line with CVX guidance.

According to East Daley’s Production Scenario Tools, the transaction will make COP the third-largest producer in the Bakken behind Chord Energy/Enerplus and Continental. Based on the location of assets, East Daley believes production from COP/MRO likely feeds egress pipelines such as Enbridge North Dakota and Dakota Access Pipeline (DAPL).

Storage:

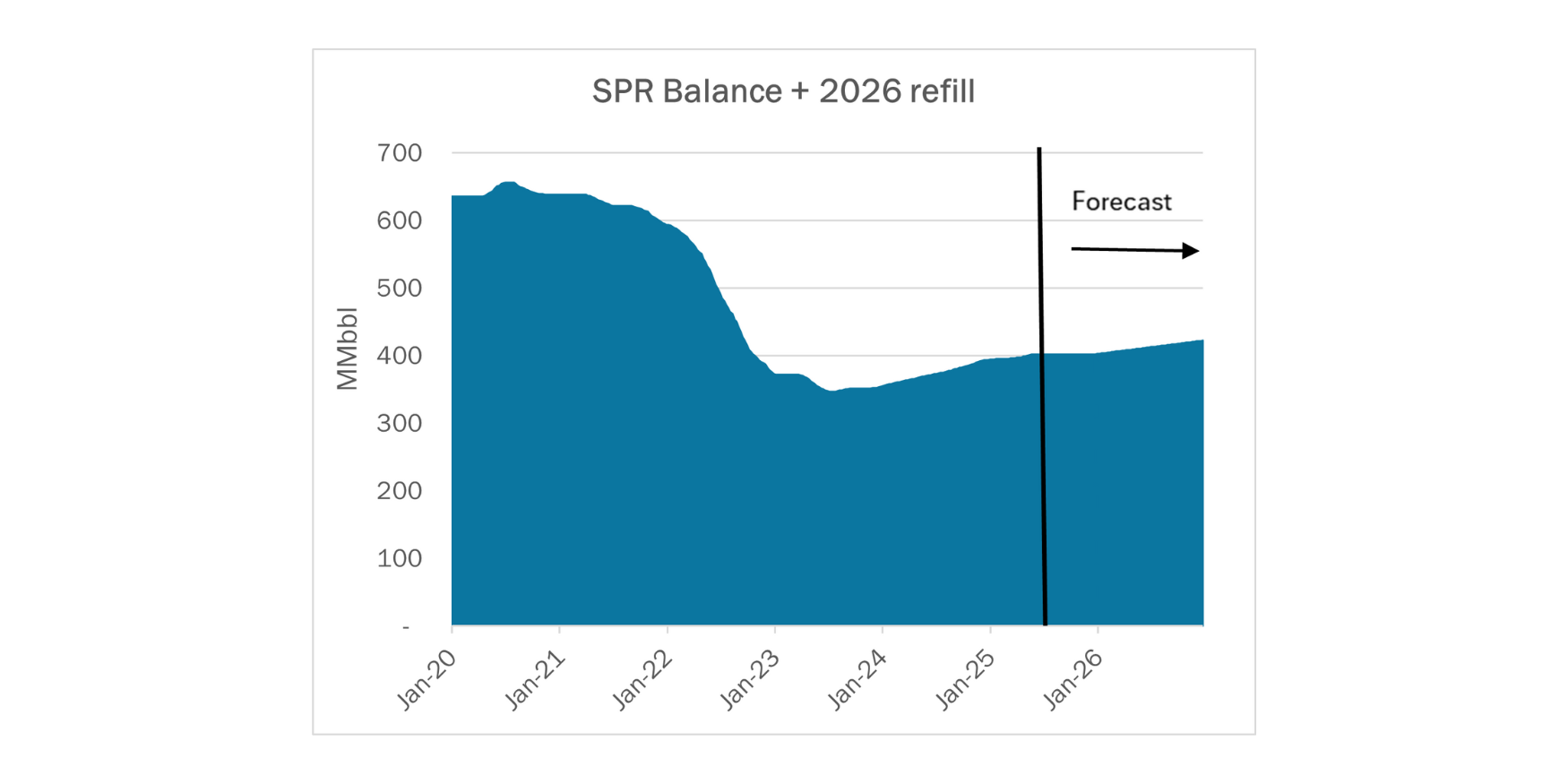

East Daley expects a withdrawal of 672 Mbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 24. We expect total US stocks, including the SPR, will close at 823 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, fell ~3.1% W-o-W across all liquids-focused basins. Samples decreased 13.52% in the Eagle Ford and 8.13% in the Gulf of Mexico. The declines were offset by a 1.43% increase in the Anadarko and 0.86% in the Bakken. The Williston Basin has a very high correlation between gas volumes and crude oil volumes, whereas the Eagle Ford’s correlation is less than 30%. We expect US crude production to remain flat at 13.1 MMb/d.

According to US bill of lading data, US crude imports decreased by 81 Mb/d W-o-W to 6.6 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico and Argentina.

As of May 17, there was ~409 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by ~246 Mb/d W-o-W, coming in at 16.7 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 22 vessels loaded for the week ending May 24 and 23 the prior week. EDA expects US exports to be 4.5 MMb/d.

The SPR awarded contracts for 3.1 MMbbl to be delivered in May 2024. The SPR has 369 MMbbl in storage as of May 24, 2024.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

Seaway Crude Pipeline The temporary incentive discount rates were extended through June 30, 2024.(FERC No 2.85.0 IS24- 269, filed May 08, 2024)

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)