Crude Oil Edge: October 10, 2023

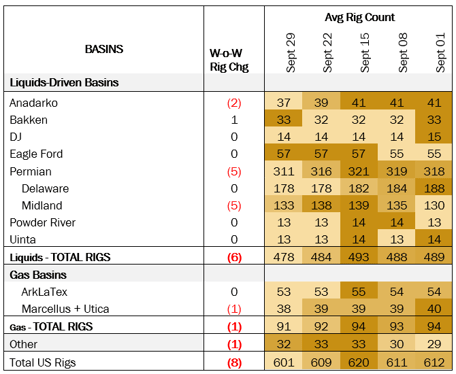

Rigs: The US rig count decreased by 8 W-o-W to bring the total count to 601. Liquids basins lost 6 rigs overall, including 2 rigs in the Anadarko, 1 in the Bakken, and 5 rigs in the Permian. Among the Permian sub-basins, the Delaware held steady and the Midland lost 5 rigs. The DJ, Eagle Ford, Powder River and Uinta basins saw no change.

Pioneer Natural Resources (PXD) and ExxonMobil (XOM) are reportedly in talks to merge, continuing a consolidation trend in the Permian Basin. There may be some acreage overlap between the companies that leads to rig reductions, as we have seen in other upstream mergers and acquisitions this year.

East Daley’s rig allocations in Energy Data Studio show PXD and XOM both have rigs in Midland County, TX on Targa’s West Texas system, at 6 and 1 rigs, respectively. There may also be some overlap on West Texas Gas’ North Midland system in Martin County, where Pioneer has 2 rigs and Exxon is running 3 rigs. At the end of September, the two producers operated 38 rigs combined in the Permian, according to Energy Data Studio.

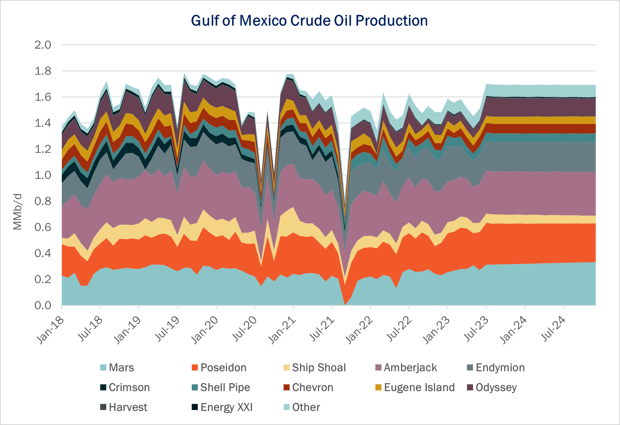

Infrastructure: The US Gulf of Mexico (GOM) accounts for 15% of total US crude oil production. Offshore production has not returned to pre-pandemic levels but has been steadily increasing since 2022.

GOM production averaged 1,929 Mb/d in July 2023, an increase of 250 Mb/d from January 2022 output of 1,680 Mb/d, according to East Daley’s Crude Hub Model. Poseidon Pipeline has seen the biggest increase in flows and is now at ~92% utilization.

Several deepwater projects have started operations this year and contributed to higher production. Woodside recently started the Shenzi North project in September. Located in the Green Canyon area 120 miles offshore Louisiana, Shenzi North will feed into the Shenzi platform, which is sized to produce up to 100 Mb/d. In April 2023, BP brought its deepwater Mad Dog Phase 2 project online in the Central GOM. Mad Dog is owned by BP (60.5%), Chevron (15.6%) and Woodside (23.9%). BP estimates the new project can produce up to 120 Mboe/d.

Privately owned LLOG Exploration is the lead operator for the two largest GOM projects coming online over the next two years. The Shenandoah field is expected to hit first oil in late 2024 with maximum production of ~100 Mb/d. The Salamanca field has a total capacity of 60 Mb/d and should produce first oil in early 2025. According to East Daley’s Crude Hub Model, both projects will be transported to shore by Genesis Energy’s (GEL) CHOPS.

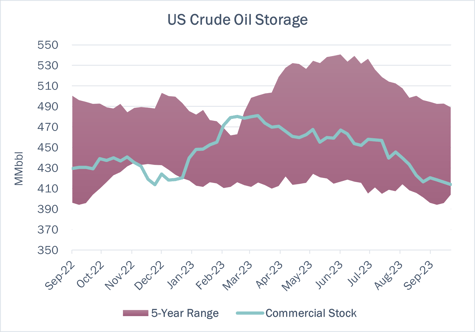

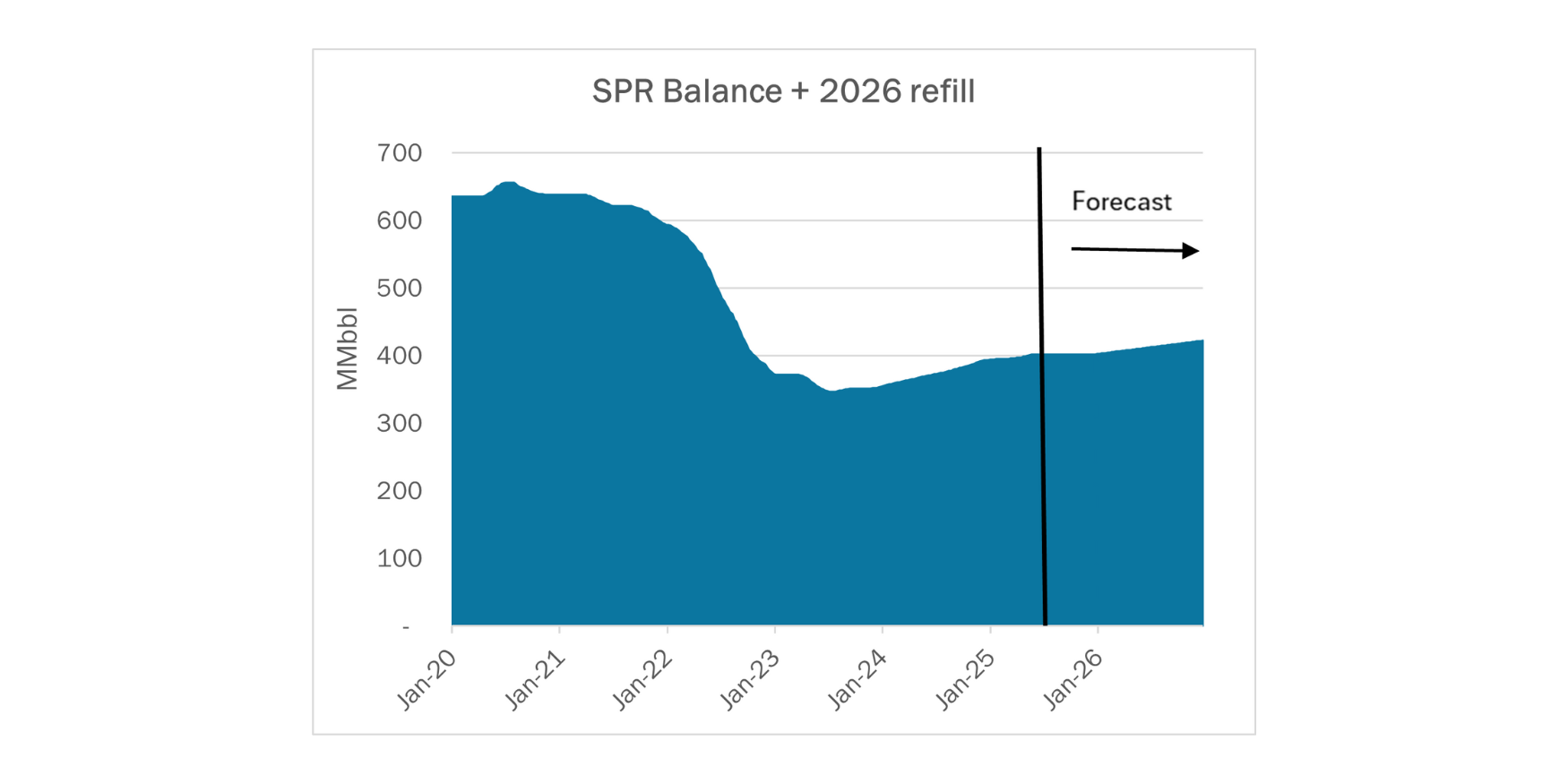

Storage: Crude oil commercial stocks are down 2.2 MMbbl for the week ending September 29 at 414.1 MMbbl. Strategic Petroleum Reserve (SPR) stocks are up 280 Mbbl, ending at 351.3 MMbbl.

SPR stocks should stay at a consistent level going forward as the last SPR repurchase concluded at the end of September and 140 MMbbl in Congressionally mandated sales have been canceled through 2027. According to DOE, the agency is committed to restocking the SPR when prices are in the $70-73/bbl range.

For the week ending October 6, East Daley expects a modest build in commercial inventories of 3 MMbbl. We expect total US stocks of crude oil to increase by 4.5 MMbbl, which includes the final deliveries for the remaining SPR repurchases.

The US pipeline sample, a proxy for change in production, declined by -1.5% in liquids-focused basins. Texas saw the largest drop at -5%, but only ~35% of total production is visible through this data. We expect US crude production will remain flat at 12.9 MMb/d.

-1.png?width=600&height=313&name=Image%20(1)-1.png)

According to US bill of lading data, US crude imports rose by 485 Mb/d W-o-W to 6.7 MMb/d. On the demand side of the equation, EDA expects refinery utilization to fall by 2% W-o-W, coming in at ~15.2 MMb/d. Refinery outage and turnaround data indicated there was another 370 Mb/d of capacity offline, as the US heads toward the peak of maintenance season.

Vessel traffic monitored by EDA along the Gulf Coast rebounded W-o-W. There were 24 vessels loaded for the October 6 week vs 18 vessels the prior week. EDA expects US exports to be 4.3 MMb/d, down ~600 Mb/d W-o-W.

-1.png)