Crude Oil Edge: October 24, 2023

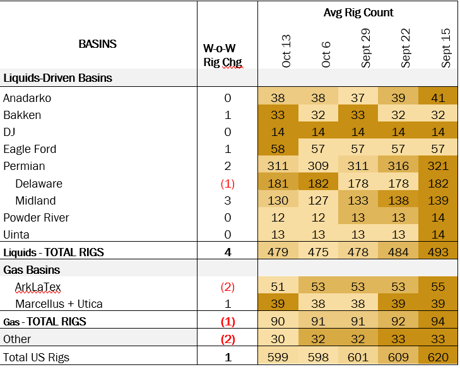

Rigs: The US rig count increased 1 W-o-W to bring the total count to 599. Liquids basins overall gained 4 rigs, including 2 rigs in the Permian, 1 rig in the Bakken and 1 rig in the Eagle Ford. Within the Permian Basin, the Delaware lost 1 rig and the Midland gained 3. The Anadarko, DJ, Powder River and Uinta basins saw no change.

Chevron (CVX) will buy Hess Corp. for $53B in stock, continuing a consolidation trend in the upstream. Chevron has been a big contributor with its recent acquisitions of Noble Energy and PDC Energy, two producers with primarily DJ Basin operations and some Permian wells. Now CVX will acquire Hess and its portfolio of Bakken and overseas Guyana assets. Hess will also provide complimentary Gulf of Mexico assets to Chevron’s own offshore portfolio. Including PDC Energy and Hess, a rolled-up CVX would have 22 rigs active currently, including; 12 rigs in the Permian, 5 in the DJ (3 PDC Energy), 2 in the Bakken (Hess), 1 in the Eagle Ford, 1 in the Uinta and 1 in Alberta.

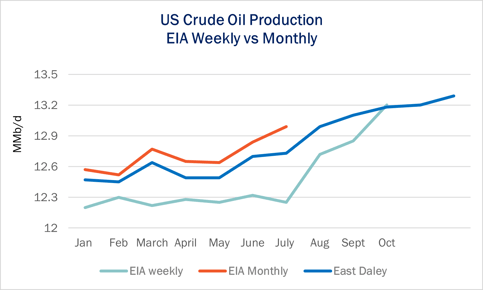

Infrastructure: US oil production could be at an all-time high of 13.2 MMb/d, if you believe one set of numbers published by the Energy Information Administration (EIA).

Oil production reached 13.2 MMb/d for two consecutive weeks, according to EIA’s latest Weekly Petroleum Status report. That would be a significant achievement, especially as rig counts have declined through much of 2023, and would imply production growth of 950 Mb/d since early July 2023 in the weekly report. But is the increase for real?

EIA publishes two reports detailing US crude oil production trends: the Weekly Petroleum Status report, and the Petroleum & Other Liquids report published monthly. The weekly EIA crude production numbers are based on a sample of producers, whereas the monthly data is based on mandatory state-reported numbers. The monthly data is typically viewed as more reliable since the numbers are used for tax purposes.

It appears that the weekly crude oil production numbers are catching up to the monthly numbers and forecasting the production increase through October. When looking at the July monthly production of 12.25 MMb/d and the ending weekly production of 13.2 MMb/d, a 209 Mb/d increase from July through October would be impressive and much more realistic.

Storage:

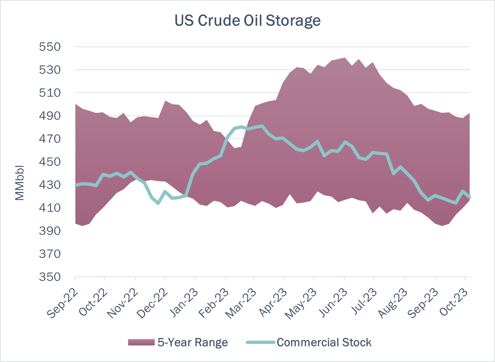

Crude oil commercial stocks saw a draw of 4.761 MMbbl over the week ending October 13 to 419.478 MMbbl. Strategic Petroleum Reserves (SPR) stocks are flat at 351.27 MMbbl.

Last week the Department of Energy (DOE) announced it will post monthly solicitations through May 2024 to purchase crude oil and replenish the SPR. However, the bids are below current WTI prices, which puts success of the auction in doubt.

Presently, the DOE has two bids out for up to 3 MMbbl of US-produced sour crude oil for delivery in December 2024 and January 2025. Both bids are for Big Hill SPR site deliveries. DOE said it will only purchase crude oil at $79/bbl or below. December and January WTI currently sells for ~$85/bbl, so filling these bids seems unlikely.

East Daley expects a draw of 1.8 MMbbl in commercial inventories for the week ending October 20. We expect total US stocks, including the SPR, will close at 769.2 MMbbl.

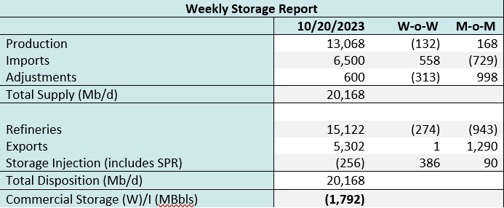

The US natural gas pipeline sample, a proxy for change in production, decreased by 1.0% in liquids-focused basins. The Gulf of Mexico saw the largest change, falling by -10% W-o-W. We expect US crude production will decline slightly to 13.1 MMb/d.

According to US bill of lading data, US crude imports increased by ~560 Mb/d W-o-W to 6.5 MMb/d. More than 60% of the supply originated on Canadian pipelines into the US, with the remainder largely coming from ships carrying Mexican and Brazilian crude.

As of October 20, there was ~2.0 MMb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to fall by 1.8% W-o-W, coming in at ~15.1 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast was flat W-o-W. There were 30 vessels loaded for the October 20 week vs 29 vessels the prior week. EDA expects US exports to be 5.3 MMb/d.

Regulatory and Tariffs

Presented by ARBO

Tariffs:

TransCanada’s (TRP) Keystone and Marketlink pipelines both extended the terms of their temporary volume incentives through November 30, 2023. On Keystone, the temporary discount only applies to uncommitted shipments originating at the international boundary and delivering to Cushing, OK. Depending on the quality of the barrel, the rate ranges from $7.60/bbl to $8.12/bbl. To get the rest of the way to the US Gulf Coast, Seaway has a current rate of $1.15/bbl. Only volumes above 50 Mb/d qualify. (IS23- 698, filed September 25, 2023) (IS23-704, filed September 28, 2023)

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)