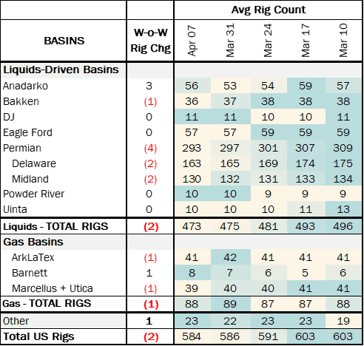

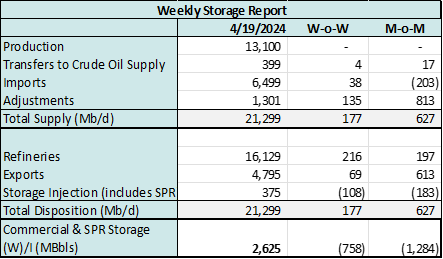

Executive Summary: Rigs: The total US rig count decreased by 2 rigs W-o-W, down to 584 from 586. Infrastructure: East Daley expects effective pipeline egress out of the Bakken to fill to 90% utilization by 2026 as crude oil production steadily grows, creating tight operating conditions on several systems. Storage: East Daley expects an injection of 2.625 MMbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending April 19.

Rigs:

The total US rig count decreased by 2 rigs W-o-W, down to 584 from 586. In liquids-driven basins, the Anadarko and Permian basins made the largest impact on overall rig count. The Anadarko gained 3 rigs W-o-W, while the Permian lost 4 rigs W-o-W. The Delaware and Midland each lost 2 rigs.

ConocoPhillips and Occidental each removed 1 rig W-o-W from their Permian – Delaware systems, while Pioneer Natural Resources subtracted 2 rigs from its system in the Midland. Anadarko operators Aztec Oil Operating, Mewbourne Oil, and Valpoint Operating each added 1 rig W-o-W, bringing the basin total to 56 rigs.

Infrastructure:

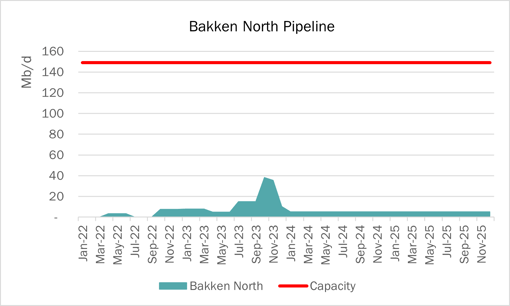

East Daley expects effective pipeline egress out of the Bakken to fill to 90% utilization by 2026 as crude oil production steadily grows, creating tight operating conditions on several systems.

We have highlighted that takeaway out of the Williston Basin is tighter than many realize. In 2026, Dakota Access Pipeline (DAPL) reaches 90% utilization, North Dakota Pipeline is at capacity, and shippers on Bridger and Double H Pipelines run into bottlenecks from Guernsey to the Denver-Julesburg Basin, according to the Crude Hub Model. However, shippers do have a last resort – Bakken North Pipeline.

Enbridge’s (ENB) Bakken North Pipeline has a capacity of 149 Mb/d, originating in North Dakota and delivering to the Enbridge Mainline via a connection at Cromer, Manitoba. From the Mainline, crude flows south into the Midwest (PADD 2) to Clearbrook. Over the last year, Bakken North has gone from running empty, to a recent 3Q23 volume surge to 26% utlization (39 Mb/d) before moving back to 7% ultization in 4Q23.

Using Bakken North carries a steep fee to move barrels to market, making for an ugly netback. Transporting crude oil north into Canada, then south again to Clearbrook is a roundabout way to reach market. The cost to ship on Bakken North is ~230% more than moving a barrel to Clearbrook via North Dakota Pipeline (~$6/bbl vs $2.56), and 190% more to Patoka via DAPL ($11.3 vs $6).

However, Enbridge Bakken North does provide a few benefits: barrels can be delivered to refineries in the Sarnia, ON market in Canada, and there is plenty of space available as Bakken egress becomes constrained.

East Daley’s Crude Production Model forecasts Bakken oil production to grow 5% on average in 2024, and 3% annually thorugh 2026 before starting a mild decline in 2027. Bakken’s production peaks at 1.395 Mb/d in 2H26.

Storage:

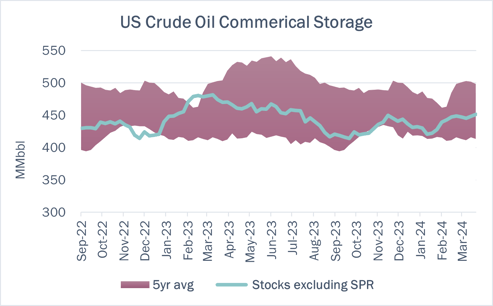

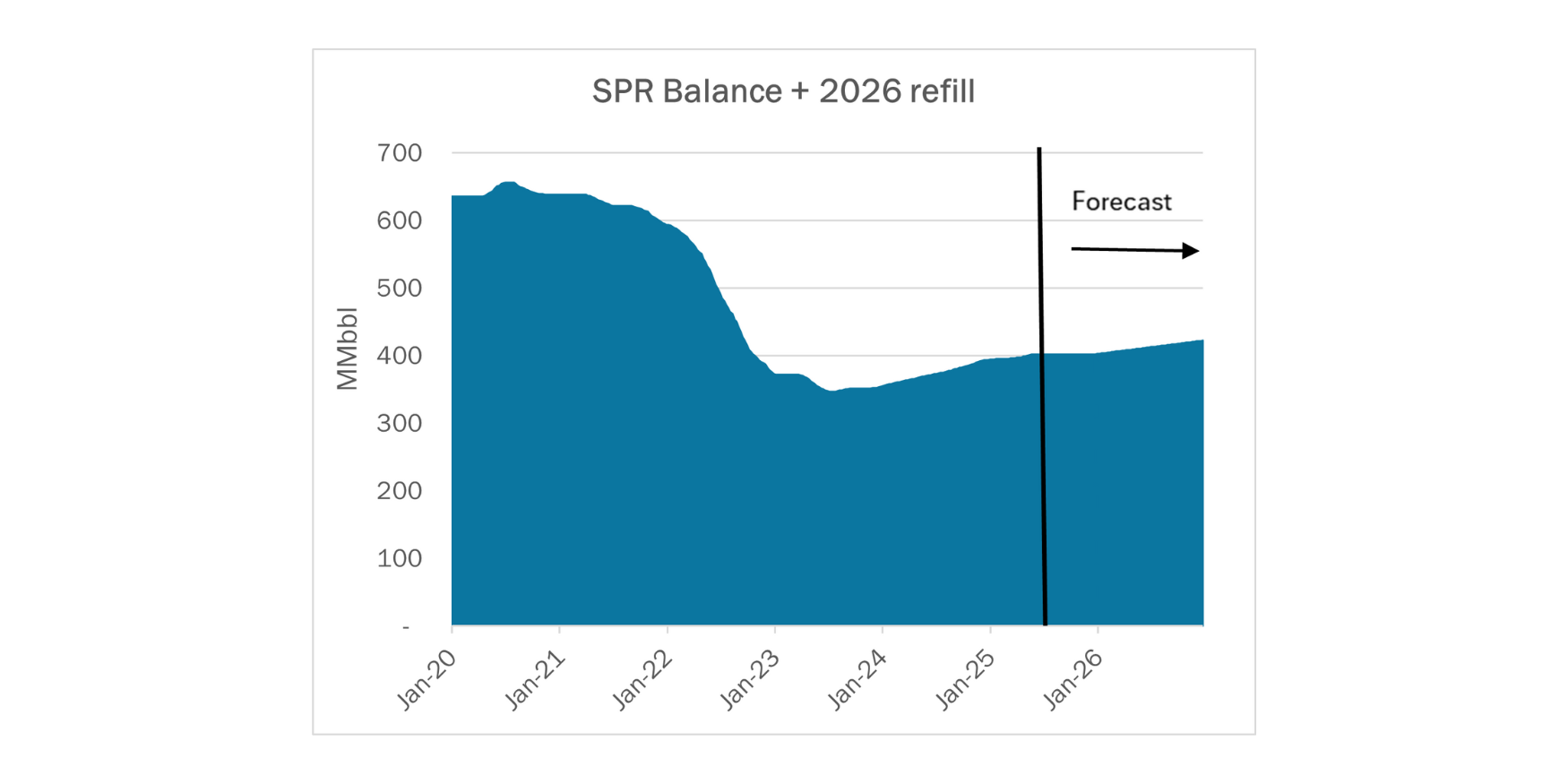

East Daley expects an injection of 2.625 MMbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending April 19. We expect total US stocks, including the SPR, will close at 827.502 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, fell ~0.88% W-o-W across all liquids-focused basins. Samples decreased 0.52% in the Williston Basin and 0.25% in the Permian. The declines were offset by a 1.18% increase in the Eagle Ford. We expect US crude production to remain flat at 13.1 MMb/d.

According to US bill of lading data, US crude imports increased by 38 Mb/d W-o-W to 6.5 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Brazil, and Argentina.

As of April 19, there was ~1,068 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by ~216 Mb/d W-o-W, coming in at 16.13 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast increased W-o-W. There were 31 vessels loaded for the week ending April 20 and 24 the prior week. EDA expects US exports to be 4.8 MMb/d.

The SPR awarded contracts for 3.2 MMbbl to be delivered in April 2024. The SPR has 365.6 MMbbl in storage as of April 19, 2024.

Regulatory and Tariffs

Presented by ARBO

Tariffs:

Bridger Pipeline LLC Expiring committed joint rates, based upon the 2012 T&Ds are canceled. New committed joint rates are established based upon the 2024 Open Season which includes incentive rates and extra barrel rates. A PLA of .4% is also established per the terms of the 2024 TSAs in addition to revised deficiency payment terms. (FERC No 123.25.0 IS24- 245, filed April 11, 2024)

Hiland Crude, LLC A new gathering origin area of Epping East located in Williams County, ND was established to all existing destinations with the agreement of at least one non-affiliated shipper. (FERC No. 5.37.0 IS24- 246, filed April 12, 2024

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)