Quick Summary

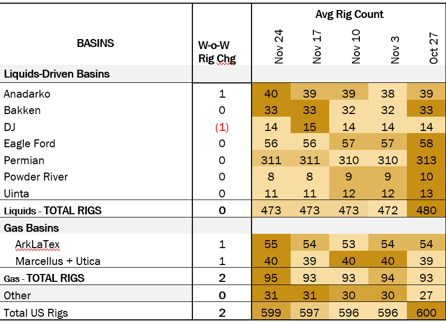

Rigs: The US rig count increased by 2 W-o-W with total rigs settling at 599.

Infrastructure: US crude oil production has reached a record high at 13.24 MMb/d, according to data released by the Energy Information Administration (EIA) last Wednesday (November 29).

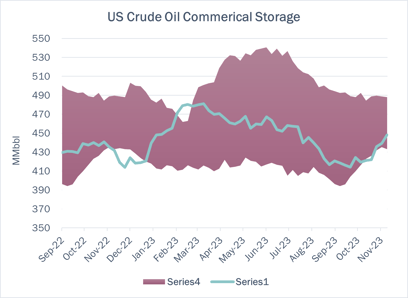

Storage: East Daley expects a withdrawal of 11.9 MMbbl in commercial inventories for the week ending December 1.

Rigs:

The US rig count increased by 2 W-o-W with total rigs settling at 599. Liquids basins held steady at 473 rigs. The Anadarko gained 1 rig and the DJ Basin lost 1 rig. Within the Permian, the Midland gained 1 rig and the Delaware remained flat.

Occidental (OXY) dropped 1 rig in the DJ Basin. In the Anadarko, Continental Resources and Murfin Drilling Company each lost 1 rig and Darrah Oil Company added 1 rig.

Infrastructure:

US crude oil production has reached a record high at 13.24 MMb/d, according to data released by the Energy Information Administration (EIA) last Wednesday (November 29). The record supply in the US coincides with the announcement of new voluntary production cuts by the OPEC+ supplier group of ~2 MMb/d. The voluntary cuts bring the total pledged cuts by OPEC+ to ~5.86 MMb/d, or 5.7% of daily world demand for 1Q24.

As OPEC+ tries to ensure stable markets and defend higher oil prices, US producers continue to grow output. As a group, US producers are focused on capital discipline, regardless where the market is or what the forward curve is indicating.

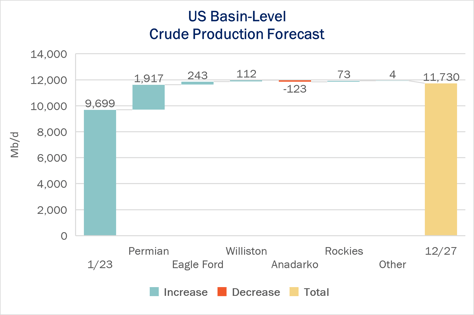

As shown in East Daley Analytics’ Production Scenario Tools (PSTs), we are forecasting basin-level production to grow 23% exit-2022 to exit-2027. Oil production by YE27 reaches 11.7 MMb/d in the PSTs, or total US crude oil production of ~15.3 MMb/d.

EDA’s basin-level forecast is ~30% below total production volumes shown by EIA, as the PSTs and the Crude Hub Model do not track Alaska, the Gulf of Mexico, and other areas outside of the major crude oil hubs and basins depicted in the Crude Hub Model.

The workhorse of US growth remains the Permian Basin. In the Crude Hub Model , EDA forecasts Permian oil production grows 34% from exit-2022 to exit-2027, reaching 7.6 MMb/d by YE27. The Eagle Ford, Williston, and Rockies basins also contribute to growth.

Storage:

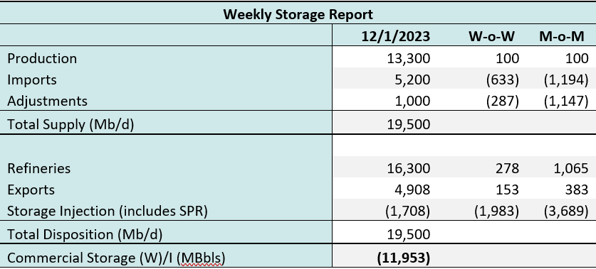

East Daley expects a withdrawal of 11.9 MMbbl in commercial inventories for the week ending December 1. We expect total US stocks, including the SPR, will close at 779.456 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, decreased by 0.5% in liquids-focused basins. The Eagle Ford saw a significant change, gaining 3.2% W-o-W, whereas the Williston Basin saw a 0.9% reduction W-o-W. The Williston has high pipeline sample coverage, whereas East Daley expects the Eagle Ford pipeline sample to be less than 30%. We expect US crude production to increase to 13.3 MMb/d.

According to US bill of lading data, US crude imports decreased by ~633 Mb/d W-o-W to 5.2 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Argentina and Brazil.

As of December 1, ~142 Mb/d of oil refining capacity was offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by 1.6% W-o-W, coming in at ~15.49 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast saw no change W-o-W. There were 25 vessels loaded for the week ending December 2 and the prior week. EDA expects US exports to be 4.9 MMb/d.

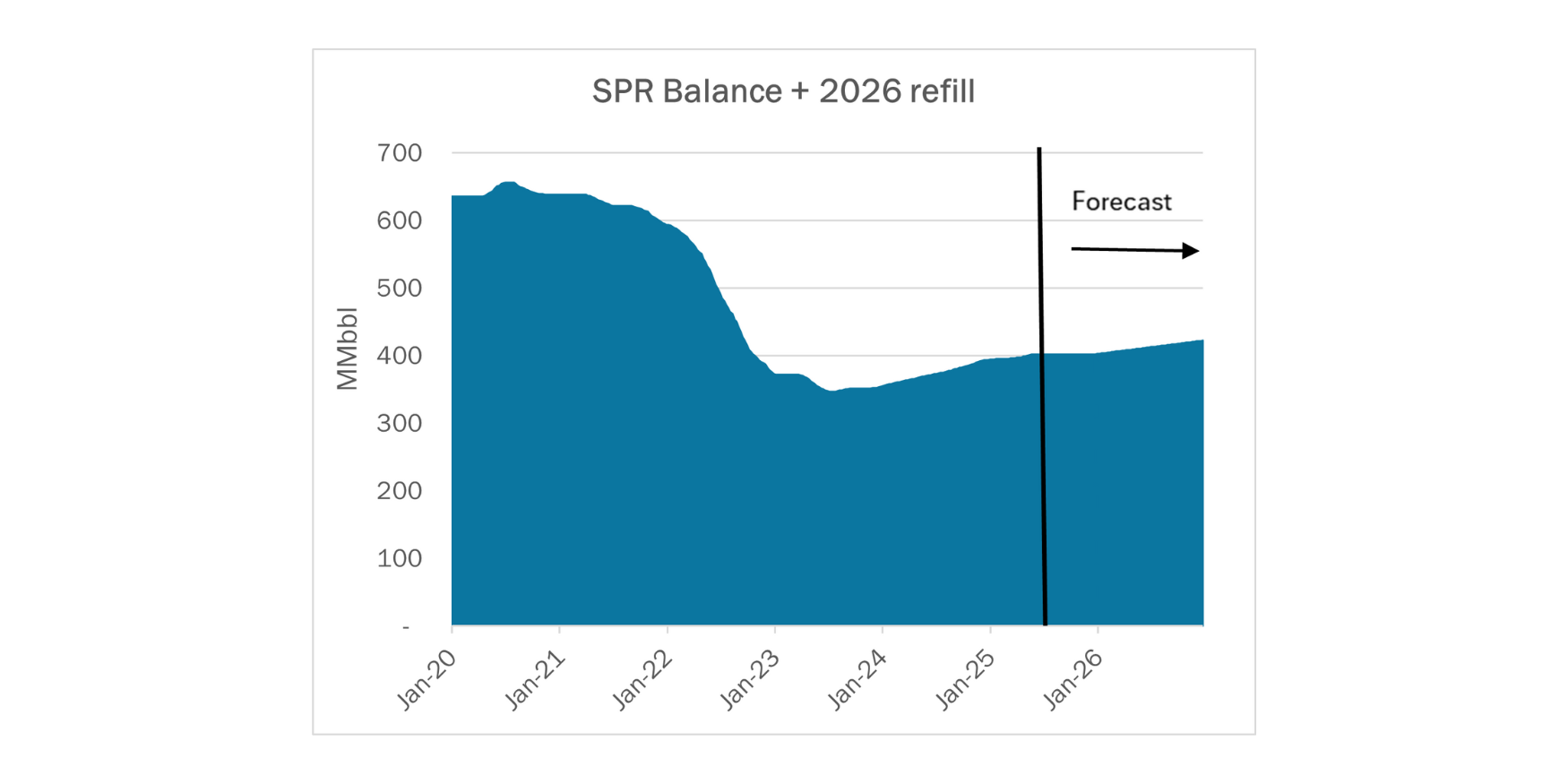

The Strategic Petroleum Reserve (SPR) awarded contracts for 2.73 MMbbl to be delivered to the Big Hill SPR site in January 2024. The SPR also saw a 313 MMbbl storage injection the week ending Nov 24 which East Daley believes to be part of a 1.2 MMbbl restock delivered through December 2023.

Regulatory and Tariffs

Presented by ARBO

Tariffs:

Bridger Pipeline LLC has removed the gravity bank for the Wyoming General Sour stream on shipments from Converse, Niobrara and Campbell Counties to the Bridger Guernsey Hub, effective December 31, 2023. Bridger stated sour movements on Bridger Pipeline have significantly declined over the past several years, without any realistic prospect of rising in the future, and that the gravity bank is on longer needed. Bridger will continue to batch a Wyoming General Sour stream, however Bridger Pipeline stated the dollar value of the gravity bank adjustments are too small and immaterial to continue. (IS24- 19, filed October 31, 2023

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)